Pound Sterling starts the new week lower against a resurgent Euro which has benefitted from a calming of nerves over the prospect of Marine Le Pen winning the French Presidency.

Latest polls suggest independent Emmanuel Macron should walk away with the crucial second round vote in May. The Euro has been sensitive to the view that Le Pen could win the vote and take France out of the Eurozone and perhaps even the European Union.

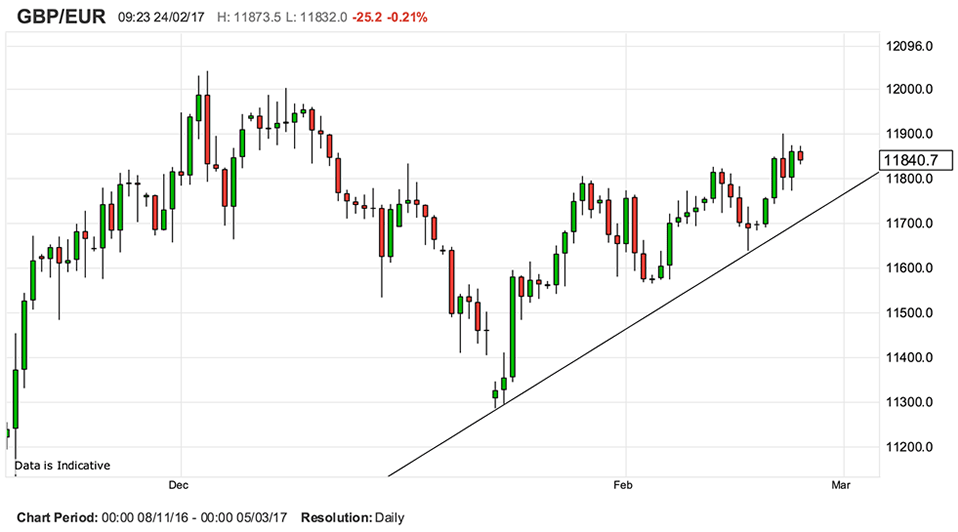

Technically speaking however, the losses in GBP/EUR are not yet great enough to undermine the mildly positive tone GBP/EUR maintains heading into month-end, and on balance we would expect this trend to extend a while yet.

As observed in our recent studies the currency pair has been in an uptrend since mid-January and only were the exchange rate to pierce below its trend-line would the bullish case be invalidated.

We see this area as lying ~1.1750 at present and a daily close below here would signal to us that perhaps the Pound is losing its advantage against the Euro.

So those are the technical levels anyone with an interest in this market should be watching. Clearly though, the uptrend is losing steam and the opening days of the new week will be key.

“Values here have pulled back into their previous range for now but not sufficiently to confirm an interim high in place as yet,” says analyst Lucy Lillicrap at AFEX, a foreign exchange brokerage based in London. “GBP prices can otherwise continue to ‘stair-case’ slowly upwards and any breach of 1.2000 would if seen improve intermediate readings as well, targeting 1.2250 if not 1.2400 thereafter.”

Trump is Euro's Big Risk this Week

However, for GBP/EUR, it is not actually Nicola Sturgeon and her nationalists that are likely to be this week's big driver.

On the event-calendar the progress of the Euro could well be determined on Tuesday February 28 when President Trump may disclose the details of his tax changes when addressing a joint session of US Congress.

"The immediate risk to the pound could come from President Trump’s address to Congress on Tuesday," says Kathleen Brooks at City Index. "Don’t put too much stock on Brexit headlines and Monday’s price action. Trump’s speech is a far more important risk even this week, and could determine whether we see further weakness."

At present there is only speculation on the details Turmp might announce, but because there is uncertainty around the event it is all the more potent for foreign exchange markets.

It is the surprise factor that shifts currency.

“As a German economist, I’m especially interested in a border adjustment tax. What would be the implications of penalising US imports for the rest of the world and export countries such as Germany?” asks Dr. Andreas Rees, Chief German Economist at UniCredit Bank in Frankfurt.

So far, financial investors have been quite sanguine to any potential negative effects of Trump’s protectionist trade agenda.

Rather, the so-called reflation trade has been dominating financial markets with a significant impact on equities, bonds and FX as markets price in higher Government spending in the US which should drive higher levels of inflation.

But Rees says a border adjustment tax would backfire on US growth and the global economy. In Europe, Germany might be most hurt, while the negative impact on France, Italy and the UK would be less pronounced.

Dangers of the Border Adjustment Tax

Rees says including a border tax would be a game changer.

“The effects on growth would not only turn negative for Europe but also backfire on the US. Curbing US imports and propelling exports obviously aims at triggering a turnaround in the US trade balance. And voilà, you are seemingly getting stronger US growth, even if proponents of a border adjustment tax do not say so explicitly. In my view, such an argument is a static, not to say, naïve view of a far more complex and dangerous adjustment process,” says Rees.

UniCredit have calculated exports to the US in percent of GDP to identify the biggest losers in Europe and Asia.

The higher this figure, the more a border tax will harm foreign economic activity.

1) Germany, US exports equal nearly 4% of national GDP.

2) Italy and the UK, 2% each

3) France, 1.5%.

4) In Asia South Korea is most exposed with 5%

5) China, 3.7%

6) Japan, 3%

Currency Implications

It appears that the Euro is at risk of any aggressive border tax but we warn reactions and patterns on foreign exchange markets are far more complex, since they are driven by (volatile) expectations and not by simple adjustments in the trade balance.

“In an immediate reaction, the US dollar will probably get stronger indeed,” says Rees.

This would likely hit the Euro exchange rate complex and ensure its recent trend lower extends.

The Pound to Euro exchange rate would be an obvious winner in this situation and we would look for it to press fresh highs into the 1.19-1.20 area.

Data to Watch this Week

In the Eurozone the highlight of the coming week will be Tuesday’s ‘flash’ HICP data for February, released at 10:00 GMT.

The headline inflation rate currently stands at 1.8%, more or less at the ECB’s target of ‘below, but close to 2%’.

A strong reading could well help the Euro as it would signal to the markets that the ECB will have to step back from its policy of low interest rates and generous quantitative easing - a policy that has kept the Euro artificially low for some years now.

But it’s important to note that much of the Eurozone’s recent inflation is largely to moves in energy and food prices, which could have a temporary effect.

That is why we are more interested in the Core CPI reading which is indicative of organic economic activity and wage rises - it is this type of inflation that the ECB will be interested in.

A strong rise here could certainly be Euro-positive, a disappointment will likely keep the single currency under pressure.

Remember to keep an eye on French politics.

“Investors will remain nervous over the run-up to the French Presidential elections. The news that centrist François Bayrou is supporting former Economy Minister Emmanuel Macron, rather than standing, reduces the risk that the centre and centre-right votes fragment in the first round,” says Ryan Djajasaputra at Investec Bank in London.

Djajasaputra argues such an outcome in turn cuts the chances of a ‘hard left’ v ‘Front National’ run-off, which might propel Marine Le Pen to the Elysée.

“But both French CDS prices and bond spreads remain at elevated levels. By contrast we note that Dutch bonds spreads are relatively contained, despite the generally good showing of the populist right wing PVV party in the polls. The election in the Netherlands takes place on 15 March,” says Djajasaputra.

The UK this Week: Article 50 and PMIs

In the UK, the Article 50 bill looks set to continue its journey through Parliament. It moves to the committee stage of the House of Lords on Monday.

Most analysts see no reason why the bill cannot gain Royal Assent early next month, allowing the PM to invoke Article 50 by the end of March at the very latest.

On the data side the various PMIs will help markets to gauge the tone of the manufacturing, construction and services sectors.

Manufacturing PMI is released on Wednesday 1 March at 09:30 AM GMT and markets are forecasting a reading of 55.5.

Construction PMI on Thursday is forecast at 52.4.

Services PMI on Friday is forecast at 54.2.

The services sector data is particularly important as it will give a good indication as to whether the trend of softer data seen in 2017 is extending.

If so then Sterling could struggle.