- GBP/EUR risks stalling near 2-month high ahead of BoE

- At risk of setback if BoE takes slower pace on Bank Rate

- Inflation forecasts & implications for rate outlook also key

- Supported near 1.15 but faces resistance above 1.1650

Image © Adobe Images

The Pound to Euro rate has extended its recovery from September's lows to reach two-month highs in recent trade but may be susceptible to profit-taking this week due to uncertainty about Thursday's Bank of England decision and risk of the BoE raising Bank Rate to a lesser extent than markets expect.

Sterling climbed throughout much of last week as risky currencies benefited from a softening of the U.S. Dollar and financial markets welcomed the selection of former Chancellor Rishi Sunak as Prime Minister.

However, market attention will turn quickly on Monday to the release of October inflation figures from the Eurozone and to Thursday's interest rate decision in which economists and financial markets expect the BoE to lift Bank Rate by three quarters of a percentage point to 3%.

This would be the BoE's largest interest rate rise to date if delivered, although it may not be quite the done deal or sure thing that many assume.

"Markets and most economists are expecting a 75 basis-point rate hike from the Bank of England on 3 November. But we think a 50bp increase is narrowly more likely. More importantly, we think the Bank Rate is unlikely to go above 4% next year," says James Smith, a developed markets economist at ING.

Above: Pound to Euro rate shown at 4-hour intervals with Fibonacci retracements of late September rebound indicating possible areas of technical support for Sterling.

Above: Pound to Euro rate shown at 4-hour intervals with Fibonacci retracements of late September rebound indicating possible areas of technical support for Sterling.

"It’s becoming increasingly clear that the Bank of England is uncomfortable with the amount of tightening markets are pricing. Investors still expect Bank Rate to peak around 5% next year. In a recent speech, BoE deputy governor Ben Broadbent suggested that GDP would take a near-5% hit over coming years if the Bank were to deliver that sort of tightening," Smith said on Friday.

Economists and markets have raised forecasts and expectations for Bank Rate aggressively in recent weeks after the government of former Prime Minister Liz Truss attempted to implement a large stimulatory package of tax cuts and UK inflation returned to the double-digits in September.

But since then GDP data for August has suggested the economy may be slowing faster than the BoE anticipated while the government of Prime Minister Sunak intends to cut back public spending notably in the year ahead, which somewhat undermines the case for aggressive increases in interest rates.

"The risk is that the BoE maintains the current pace of tightening and delivers a 50bp hike," says Carol Kong, an economist and currency strategist at Commonwealth Bank of Australia, who sees the Pound at risk of fresh losses against the Dollar this week.

Whether Thursday's change in Bank Rate is enough to satisfy the market will be important in determining if the Pound can sustain its recovery against the Euro into next weekend, although the BoE's latest inflation forecasts will also be scrutinised closely too for clues about the outlook for interest rates.

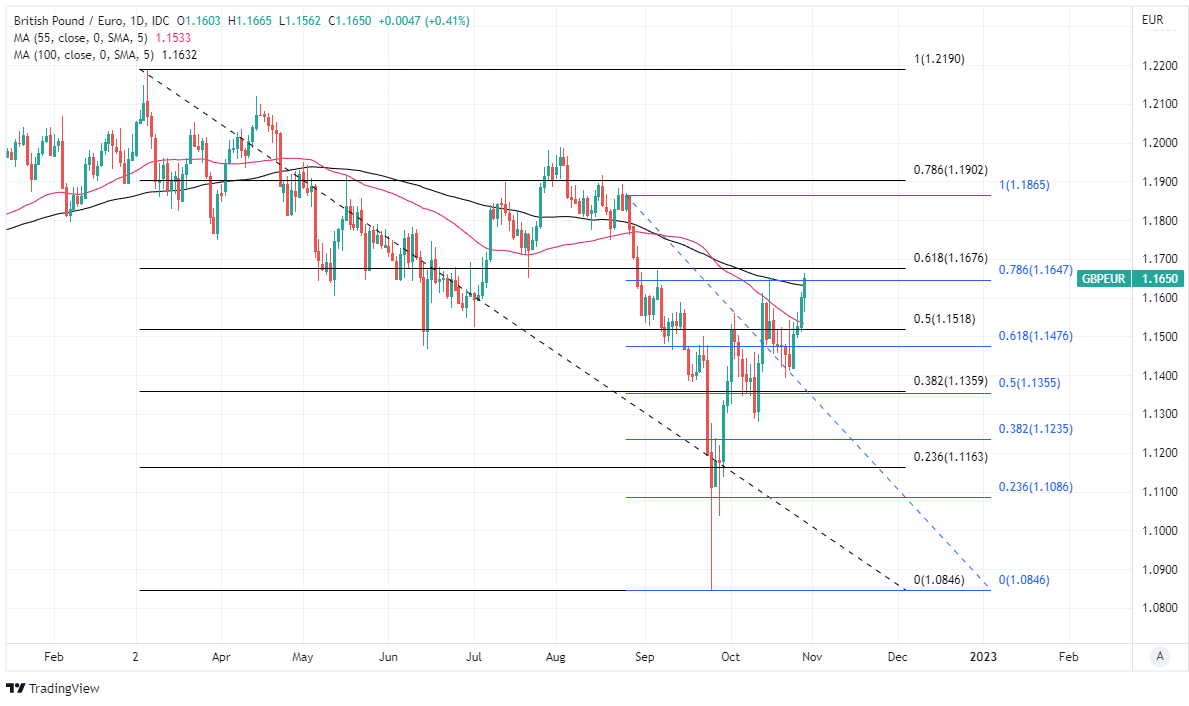

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of August and 2022 downtrends indicating possible areas of technical resistance.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of August and 2022 downtrends indicating possible areas of technical resistance.

The extent to which the BoE's inflation forecasts sit below the 2% target at the other end of the multi-year forecast horizon will be revealing of the degree to which the BoE wants to discourage market pricing from the current assumption that Bank Rate will rise above 5% early next year.

"The MPC’s forecasts likely will show CPI inflation hovering near the 2% target in two-to-three years’ time, despite the big upward shift in markets’ expectations," says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

"The MPC won’t overtly lean against markets’ expectations, as neither the scale of the impending fiscal tightening, nor the persistence of inflation pressures, is clear at this stage. But Deputy Governor Broadbent’s speech last week showed growing unease at the BoE with market pricing," he adds.

Tombs is looking for the BoE to raise Bank Rate by 0.75% to 3% on Thursday and to emphasise that risks to its inflation forecasts are on the downside rather than to quibble over the market's assumptions and this is possibly the best case scenario outcome for Sterling this week.

But that won't necessarily be enough for the Pound to Euro rate to build further on its recovery while the risk is of a smaller than expected increase in Bank Rate on Thursday that would come as an upset for Sterling that leaves it vulnerable to further profit-taking ahead of next weekend.

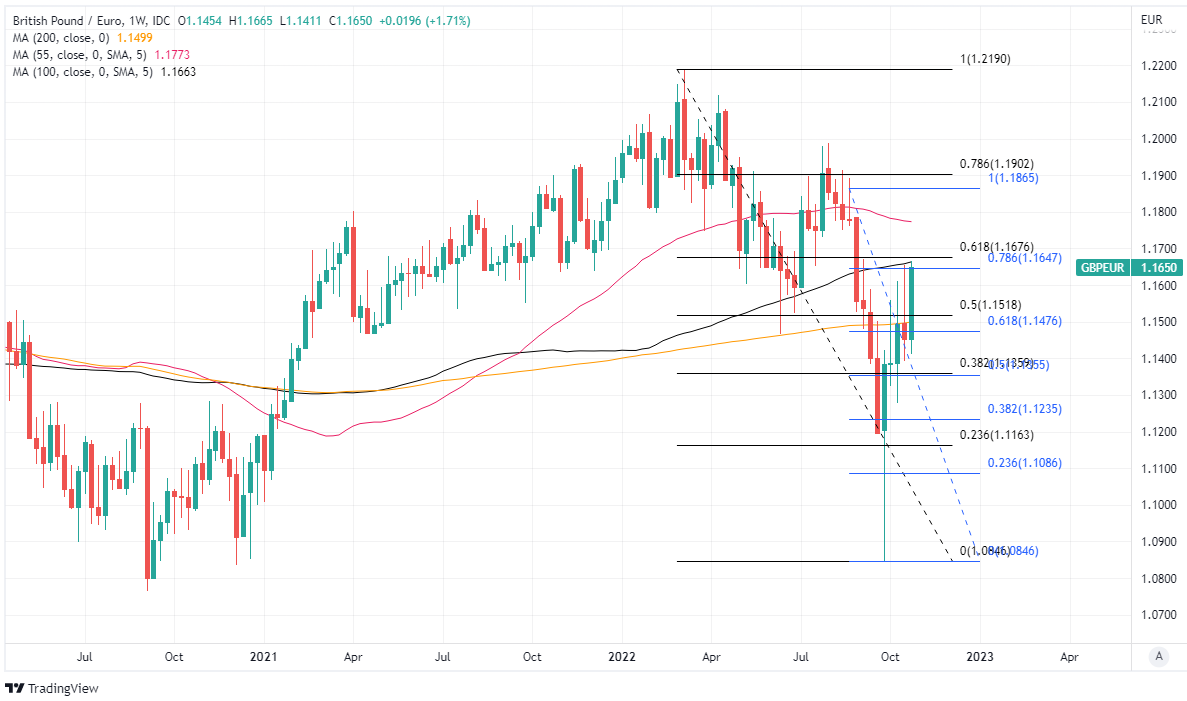

Above: Pound to Euro rate shown at weekly intervals with Fibonacci retracements of August and 2022 downtrends indicating possible areas of technical resistance and selected moving-averages.

Above: Pound to Euro rate shown at weekly intervals with Fibonacci retracements of August and 2022 downtrends indicating possible areas of technical resistance and selected moving-averages.