- GBP/EUR supported around 1.18, 1.1750 on charts

- But needs 'hawkish' BoE surprise to recover further

- Bank Rate seen rising to 1% & new post-2008 high

- But economic forecasts may stifle appetite for GBP

Image © Adobe Stock

The Pound to Euro rate climbed from near April lows last week and may attempt to extend its recovery over the coming days but it would likely take a significant 'hawkish' surprise from the Bank of England for it to avoid succumbing to the implications of any gloomier set of BoE economic forecasts this Thursday.

Sterling rebounded from close to the round number of 1.18 against the Euro last Monday to enter the new week trading above 1.19 although the recovery reflected more the misfortune of the Euro than it did any kind of market enthusiasm for the Pound.

Renewed market concerns about the security of continent's gas supply and economic risks stemming from the spread of coronavirus containment measures in China each weighed heavily again on the European single currency last week, helping to stem an earlier slide in the Pound-to-Euro rate along the way. (Set your FX rate alert here).

But the danger is now that any further recovery becomes stifled by Thursday’s updated economic outlook and inflation forecasts from the BoE, which are likely to further contradict market expectations for Bank Rate to rise from 0.75% to more than 2% before the curtain closes on 2022.

“The large upward shift in markets' expectations for Bank Rate since the MPC's last set of forecasts in February also will compel the MPC to revise down its main projection for GDP growth,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

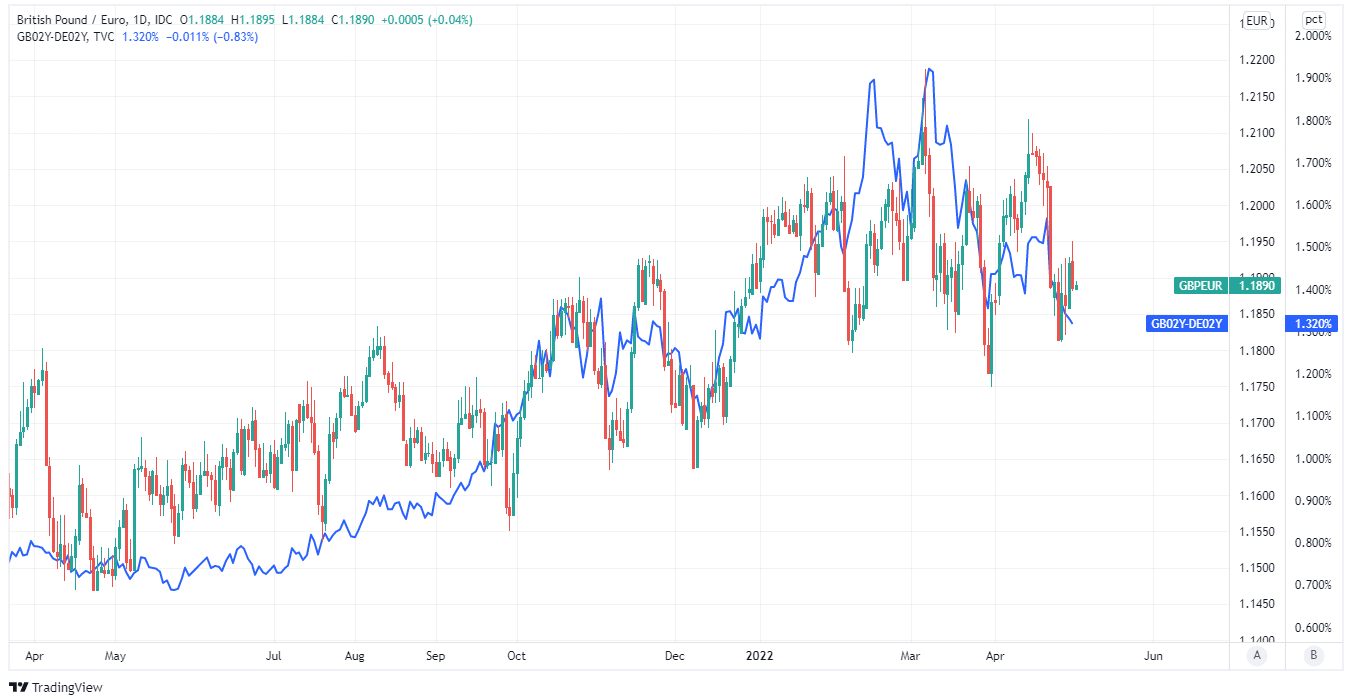

Above: Pound to Euro rate shown at daily intervals alongside spread - or gap - between 02-year UK and German government bond yields. Click image for closer inspection.

“We think it is extremely unlikely that the MPC will validate the current path for Bank Rate envisaged by markets at this meeting, either with its new forecasts, or its comments in the minutes,” Tombs added in a research note last week.

The BoE is widely expected to lift Bank Rate to a post-financial crisis high of 1% on Thursday but has said repeatedly of late that the squeeze on household incomes will reduce inflation sharply over the coming years, implying that interest rates may not need to rise as far as markets expect later in 2022.

Meanwhile, Governor Andrew Bailey said twice in April that the bank will have to walk a tightrope when judging how much further UK interest rates might need to be raised in order to bring down an inflation rate that reached 7% in March.

“We are now walking a very fine line between tackling inflation and the output effects of the real income shock and the risk that that could create a recession,” Governor Bailey told the Peterson Institute for International Economics while in Washington late last month.

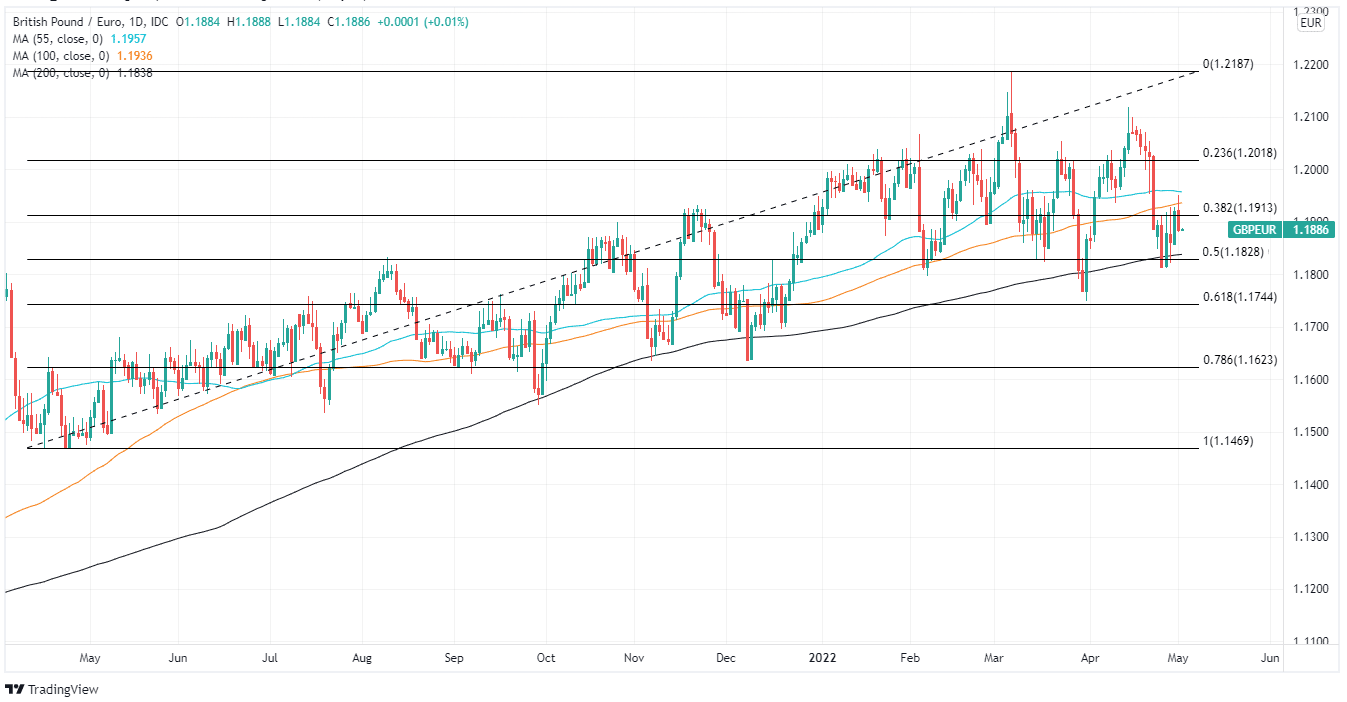

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of April 2021 uptrend and selected moving-averages indicating possible medium term areas of technical support for Sterling. Click image for closer inspection.

Since then some UK economic figures including the March retail sales report have suggested that the squeeze on incomes may now be cannibalising spending that would otherwise flow to other parts of the economy, which is almost exactly what the BoE has warned of.

All of this could lead the squeeze on incomes to be viewed as a substitute for some of the interest rate rises that have all but been taken to the bank by the market in the months ahead, with possible adverse consequences for Sterling.

But UK inflation rose to 7% in March and more than three times the level of the BoE's 2% target while even after excluding increases in energy and food costs, the annual pace of price growth still leapt from 5.2% to 5.7% in what was still likely a significant development for the bank's Monetary Policy Committee.

“A dovish BoE hike, coupled with the lingering global uncertainty, won't do GBP any favours next week. That said, we wouldn't chase the move lower either,” says Mark McCormick, global head of FX strategy at TD Securities.

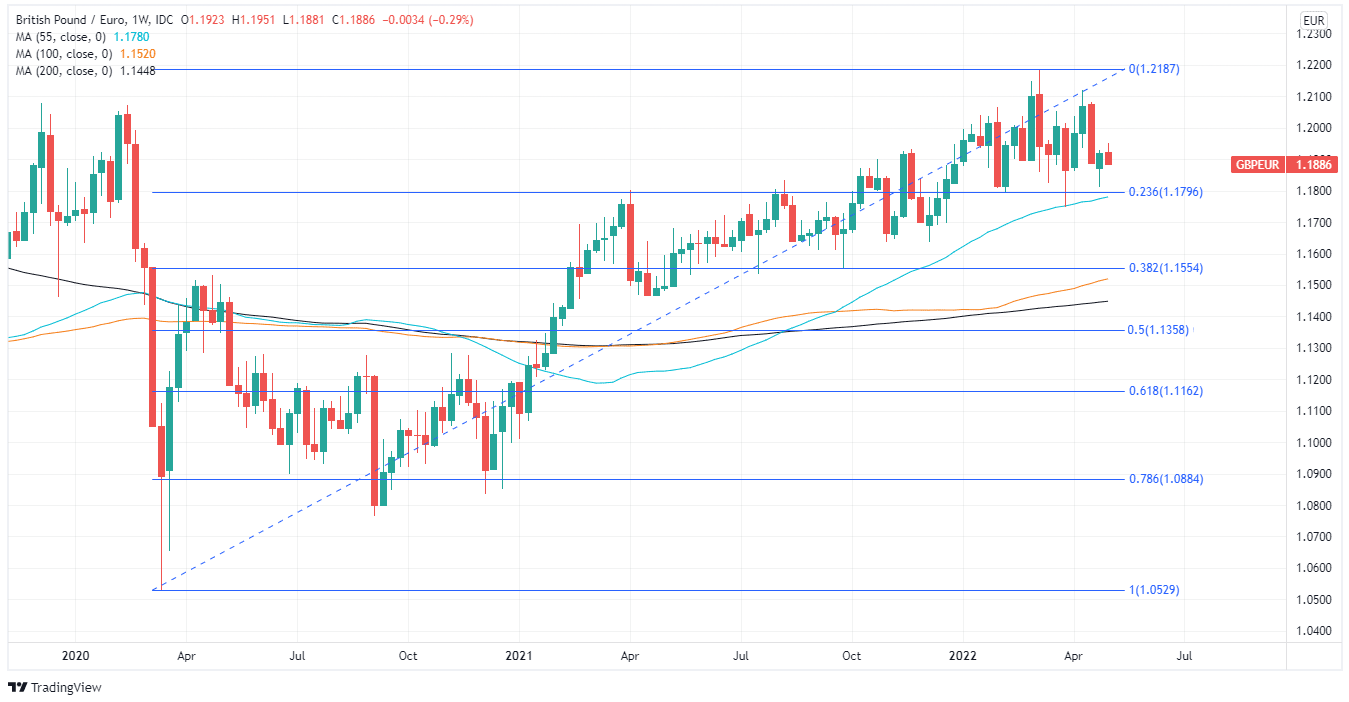

Above: Pound to Euro rate shown at weekly intervals with Fibonacci retracements of March 2020 recovery trend and selected moving-averages indicating possible medium term areas of technical support for Sterling. Click image for closer inspection.

Above: Pound to Euro rate shown at weekly intervals with Fibonacci retracements of March 2020 recovery trend and selected moving-averages indicating possible medium term areas of technical support for Sterling. Click image for closer inspection.

“We think fading the highs in EURGBP might be a better way to trade the recent price action, reflecting the extreme GBP discount priced into markets currently. We like fading the EURGBP range extremes between 0.83 and 0.85 [GBP/EUR 1.2048 and 1.1764],” McCormick also said on Friday.

Much depends for the Pound to Euro rate on the BoE's actual decision about interest rates this week, on the possible implications of its latest economic forecasts and the language contained in the statement as well as the accompanying quarterly Monetary Policy Report.

“We do not think that hiking into a cyclical slowdown is negative for the currency—nor is it a problem that is unique to the UK. However, for now, the BoE’s more nuanced approach to balancing the growth and inflation path has negative implications,” says Michael Cahill, a G10 FX strategist at Goldman Sachs.

Cahill and Goldman Sachs colleagues suggested on Friday that clients of the bank consider selling Sterling after downgrading their forecasts for the Pound-Euro rate, which is now expected to slip back toward 1.1627 over the coming three months after previously being tipped to trade around 1.2048.

This is partly due to an expectation that the BoE will continue to push back against market expectations for Bank Rate later this year, which is a risk for Sterling this week.