- Markets in the red due to coronavirus fears

- EUR remains a top performer in this environment

- GBP finds support from shift in Bank of England rate cut expectations

Image © Adobe Images

- GBP/EUR spot: 1.1484 -0.46%

- Bank transfer rates (indicative): 1.1182-1.1261

- FX specialist transfer rates (indicative): 1.1300-1.1380 >> More information

The Euro charged ahead of its major rivals in the final trading day of the week as a global stock market slump gathered pace, confirming the single currency to be one of the main beneficiaries of the market's fear of the economic impacts of the coronavirus.

A look at global equity markets shows a bloodbath ahead of the weekend: the FTSE 100 is 3.33% down, the German DAX is 3.6% down, the Dow Jones is forecast to open 2.15% down and the S&P 500 is forecast to open 2.41% down.

The Euro exchange rate complex is meanwhile sharply higher, confirming the single currency's strong relationship to trends in investor sentiment: the Euro-to-Dollar exchange rate is an eye-watering 0.90% higher at 1.1325 while the Euro-to-Pound exchange rate is 0.43% higher at 0.8703. This gives a Pound-to-Euro exchange rate of 1.1489 and takes the week's loss for Sterling against its cross-channel neighbour to 1.0%.

"What was largely a Chinese issue just a month ago, has turned into a global crisis that threatens to throw the world economy into recession. The growth of the virus may have seemed relatively gradual outside of China, yet the growth in cases outside the country has actually been an incredible 6600% over that timeframe. We are at a tipping point, where a similar month of growth for the virus will likely spark a global panic and bring severe economic consequences that have yet to be realised," says Joshua Mahony, Senior Market Analyst at IG.

The Euro remains an outperformer in the current climate; not so much because the market believes the Eurozone is better placed than others to withstand the coronavirus outbreak, but rather because investors continue to liquidate stock holdings and repatriate Euros.

The Euro's gains are therefore something of a technical phenomenon: because Eurozone interest rates are some of the lowest in the world (the ECB's base rate is -0.50%), investors borrow in euros to fund stock market investments.

When it comes time to sell, that drawdown of euros is replenished. Consider that this is one of the longest bull markets in history and you might get a sense of how vast the repatriation demand for euros might become if the sell-off continues.

"The tank has already run dry despite a week of stimulus across central banks, governments and the IMF. On a week that has seen extraordinary action taken to stem the flow of pessimism, we are yet again heading towards the weekend surrounded by a sea of red. Despite brief moments of stimulus-fuelled optimism, traders always return to the gradually increasing threat of the coronavirus," says Mahony.

The Euro is meanwhile looking set to end the week nearly 2.0% higher against the U.S. Dollar and 1.0% higher against the Pound and has advanced against all the major currencies apart from the 'ultra' safe havens the Japanese Yen and Swiss Franc.

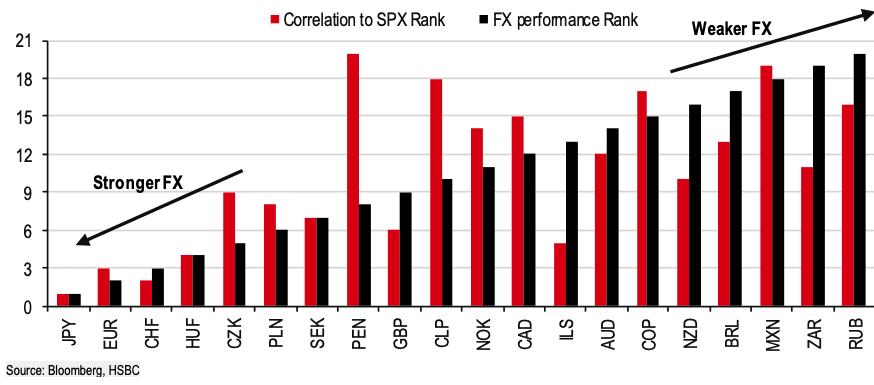

Research by HSBC shows that the Japanese Yen is the most likely to benefit from when markets are experiencing a risk-off episode, closely followed by the Euro and then the Swiss franc. "We believe that while one story or theme dominates financial markets, FX will remain beholden to the forces of Risk On – Risk Off," says Dominic Bunning, Senior FX Strategist at HSBC Plc.

"Despite the spreading of the coronavirus across Europe, the Euro has strengthened significantly against most major currency peers over the past week or two. Investors aren’t attracted to the Euro – slow Eurozone growth, high unemployment and low interest rates – it is rather the relentless unwinding of carry trades causing the spike in the common currency’s value," says George Vessey, Currency Strategist at Western Union.

"Typically, carry trades are put on in stress-free market conditions, when investors are confident in global growth and higher yielding assets appreciating. Investors sell lower-yielding currencies (like the Euro) to buy higher-yielding currencies (like the USD). The rapid reversal of this trade effectively means traders are buying back Euros, causing the currency to rally," adds Vessey.

The analyst says of late the Pound-to-Euro exchange rate has suffered as a result, "melting to around €1.14-€.1.15 having traded near €1.20 only last week."

And, if the global stock market sell-off continues Vessey says there is a realistic chance the Pound-to-Euro rate could fall towards 1.12; "if the big unwind of carry trade continues, we might expect EUR/USD to inch towards $1.14, which could drag GBP/EUR towards €1.12."

Bank of England Provides Sterling with Some Support

Above: Andrew Bailey testifies to the Treasury Select Committee on March 04. Image (C) Pound Sterling Live. Source: Parliament TV

While the Euro is benefitting in the current market environment, we note Sterling has shown a greater resistance to the Euro's onslaught of late and the Pound-to-Euro exchange rate is down only marginally in the past 24 hours. It is meanwhile gone higher against the Dollar and a host of commodity currencies such as the Australian and New Zealand Dollars.

The reason the Pound has not succumbed to fresh selling pressures is because markets have had to rapidly reverse their expectations that the Bank of England will follow the lead of the U.S. Federal Reserve and cut interest rates at the end of March.

There was a growing assumption that the market meltdown would force the Bank into slashing rates from 0.75% and in doing so deprive Sterling of a key pillar of support. Yet, the incoming Governor of the Bank of England, Andrew Bailey, on Wednesday told lawmakers in Parliament that a cut is by no means yet a guarantee.

"The catalyst appears to have been comments from incoming Bank of England governor, Andrew Bailey," says Erik Bregar, Head of FX Strategy at Exchange Bank of Canada, on the Sterling's recent relative resilience.

When asked about whether the Bank should cut interest rates before the next scheduled decision on March 26, Bailey said:

"The Monetary Policy Committee hasn't in its history tended to do that but there is nothing that in the constitution of the Monetary Policy Committee to stop that happening. I think what we need frankly is more evidence than we have at the moment, as to exactly how this is feeding through. We have got a building picture of evidence. The Bank of England is ... working extremely hard on it. I have been engaged on it this week, and I think then we can reach our judgment."

The Bank of England has good reason to think twice before cutting interest rates simply for the fact that it might not help an economy that has been impacted by coronavirus fears.

David Bloom, HSBC's senior foreign exchange analyst, hit the airwaves on Friday to explain why central bank interest rate cuts do not necessarily help when a crisis is an issue of a lack of supply:

"I'll use toilet paper as the example, only because there has been panic buying of toilet paper... if there is nothing available in the shop and someone gives me £100, I say 'OK I couldn't get it', and then I get given £1000, I say 'but it is not available!'" Bloom told CNBC.

The coronavirus is a shock to the supply side of the economy: the UN estimates that the supply chain to global manufacturers owing to the Chinese economic shutdown stands at £50BN.

"The problem is it's a supply side problem and throwing money at a supply side problem may not help" adds Bloom, "that's why people are sceptical of central banks cutting rates."

This crisis therefore differs notably to the 2008 crisis where the fundamental problem was a ceasing up in the supply of finance to a debt-laden global economy.

Bailey's unwillingness to send a signal that the Bank intends to cut interest rates could also be due to the looming March 11 budget announcement.

Bailey said that support for the economy during the coronavirus outbreak would likely need to be in the form of a combination of Government and Bank of England support: i.e. the Treasury and the Bank would need to coordinate. This is particularly relevant to providing trade finance to those companies with international supply chains, which are most at risk of the coronavirus outbreak.

The Bank could therefore still offer support, just not via an interest rate cut.

We would imagine that the Bank will have the benefit of observing the reaction to rate cuts from the United States, Australia, Canada and the European Central Bank by the time the March 26 Monetary Policy Committee meeting takes place.

Thus far, the response to the rate cuts by the real economy is inconclusive but what we can say with certainty is these cuts have not stabilised investor sentiment.

We would therefore imagine the Bank would only cut rates if they believed the financial system was starting to show stress.

For now markets see another 50/50 decision looming and with budget day only a week away foreign exchange markets could well adopt a wait and see approach to Sterling.