Image © Adobe Stock

Pound Sterling was swamped with widespread losses as currency and interest rate markets responded to a further increase in one of the UK's most important measures of inflation barely more than a day out from the latest Bank of England (BoE) policy decision, leading to a wave of forecast changes among analysts and economists.

Sterling rose against the Japanese Yen and Korean Won on Wednesday but fell against the remainder of its counterparts in the G20 bucket with the heaviest losses coming in relation to the Swedish Krona, Russian Rouble and Polish Zloty amid another large shift higher in market-implied expectations for the BoE Bank Rate.

The market-implied rate for year-end was said to be testing 6% on Wednesday having overcome the 5.75% threshold that triggered a mini meltdown in the U.S. banking sector following the March failure of Silicon Valley Bank, and soon after the Office for National Statistics announced inflation figures for May.

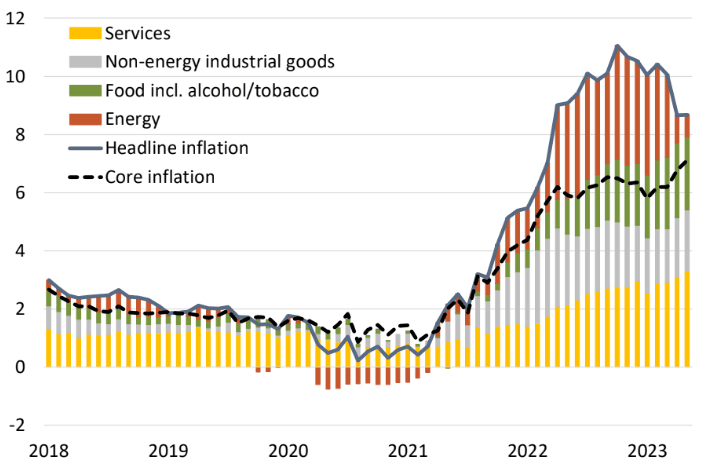

Overall inflation remained at 8.7% last month while the core inflation rate rose from 6.8% to 7.1% once reported declines in energy and food prices were set aside, leading to widespread suggestions of the UK having a bigger problem with inflation than in other comparable economies.

Above: UK inflation breakdown, image courtesy of Berenberg Bank.

The May inflation developments follow the beginning of a new financial year and another round of annual price adjustments among companies, as well as a near 10% uplift in the national minimum wage and similar but slightly smaller increases in pay for professions further up skills ladder.

Previously, both of the UK's inflation rates had fallen haphazardly since October last year and throughout a period in which the economy dodged a recession that was previously projected by the Bank of England, though the increase in market-implied interest rates has been very significant over the last month.

These market-implied rates are immediately passed through to borrowing costs for mortgages as well as some other forms of loans but many will nonetheless watch and listen closely on Thursday for any indication of whether the BoE intends to formalise the market levels by changing Bank Rate.

There is a wide variety of views among analysts and economists on the subject of far Bank Rate could move Thursday and after with similar being true of how analysts see the outlook for the Pound: Some of these views are encapsulated in whole or part below.

Stephen Gallo, global FX strategist, BMO Capital Markets

"My view is that the FX market has been focusing on the weaker USD — which has supported GBP — and the anticipation of more carry, which probably explains part of the decline in EURGBP. I think this dynamic is changing."

"There have been periods when GBP has depreciated or remained weak as sterling rates have moved higher. One period was during the run-up to the 1967 devaluation, and there were other instances in the 1970s and early-1980s. Britain's chaotic 1992 exit from the ERM is another example."

"The BoE has two options in my opinion. The first option is to deliver further cautious tightening and hope that inflation and a wage price spiral cause a slowdown on their own. The problem with this option is that high inflation is already embedded, and it will probably result in a weaker value for sterling as markets remove interest rate hikes from the curve."

"The second option is to move faster and more aggressively with tightening, by shifting to a series of 50 or even 75bps increments. With core inflation above 7.0% and the policy rate less than 5.0%, the Bank is arguably not restrictive enough. The Bank has been confounded by the strength of the labour market in 2023."

"The second option seems like the better route, and it favors 50bps from the BoE tomorrow. This is now BMO's base case."

Mark McCormick, global head of FX strategy, TD Securities

"May inflation surprised sharply to the upside again and further builds on April's surprise relative to the MPC's projections. As such, we no longer expect the MPC to push back against market pricing, though we still see 25bps as more likely than a 50bps hike."

"GBPUSD comes into the BoE sitting near HFFV (that rests at 1.2770). GBP needs a surprise factor, where continued pushing back on market pricing might help it nudge lower. We like EURGBP higher on the week, after holding 0.85."

Jordan Rochester, FX strategist, Nomura

"It’s a human decision by nine people whether they react to spot inflation prints (like the Fed does) or carry on with their usual reaction function of balancing that with warning signs from growth of lower inflation to come (GDP since Q2 2022 has been 0% essentially, housing market clearly flashing red, PPI down etc).

I tend to be on the more dovish side of the UK market it seems..BUT I have been wrong on how services CPI keeps rising despite the PMIs signal."

"As from an RV [relative value] perspective the UK has a faster monetary policy transmission via housing than Germany and France (with their lovely 10 to 30yr fixed mortgages)."

John Hardy, head of FX strategy, Saxo Bank

"We have to expect that the BoE does what it can to claw back as much credibility as it can, or else. Finger pointing and a small hike could prove devastating for sterling. In short: the market has already priced 90 basis points through the next three meeting."

"EURGBP rallying sharply today despite hot new UK inflation suggests that the Bank of England has a lot to deliver to support the bullish sterling case. There is plenty of room for this pair to consolidate higher without reversing the down-trend, but 0.8675 possible begins to stress it badly."

Bipan Rai, North American head of FX strategy, CIBC Capital Markets

"Although the market briefly discounted an almost 50% probability of a 50bps hike Sterling gains have unwound as the risk of terminal rates threatening 6% have amplified recession concerns into 2024."

"Despite the rise in core CPI, in part due to ongoing supply concerns, which cannot be fixed by higher rates alone, leaves us still looking towards a 25bps hike tomorrow. Renewed Gilt selling, boosting mortgage rates suggest recession concerns look set to continue to drag on near-term GBP performance."

Samuel Tombs, chief UK economist, Pantheon Macroeconomics

"All told, then, we think the headline rate of CPI inflation will fall to about 4.5% by the end of 2023, on course for a near-2% rate in the second half of 2024."

"The case for expecting CPI inflation to fall sharply in the second half of this year remains strong. For a start, we already know that Ofgem will reduce its energy price cap by 17% in July, and wholesale prices currently are consistent with a further 5% or so fall in the cap in October."

"It might seem implausible that our Q4 average forecast, 4.7%, still is below the 5.1% rate forecast by the BoE last month, but note that motor fuel prices recently have fallen sharply, and PPI data have been soft."

"The rate of increase in consumer prices remained far too rapid in May for the MPC to contemplate bringing its rate hiking cycle to an end soon."

"Accordingly, we continue to think that the MPC will raise Bank Rate by 25bp today and by a further 25bp in August, but that the Committee will have seen enough evidence of slowing price rises then to stand pat with Bank Rate at 5.0% in September."

Brad Bechtel, global head of FX, Jefferies

"The situation for the UK is not getting any better but economists are holding out hope that the inflation dynamic will change dramatically next month with base effects kicking in big time, especially in the energy sector. We will see."

"Let's see if the GBP is patient enough to wait for July inflation data. GBP/USD is -46bps lower with the pair back to 1.2700. I am flat the GBP here and would not go near it until this is resolved. EUR/GBP back to 0.8600. the 'shadow' MPC voted for a 50bps hike at this meeting, let's see if the BoE has the courage to follow suit."