Image © Adobe Stock

Some major investment banking names are predicting the Federal Reserve will opt to maintain interest rates at current levels on March 22 in response to recent financial market turmoil.

But others maintain expectations for another hike, although one even sees the prospect of a rate cut.

This makes the upcoming meeting of the Fed's FOMC the most unpredictable for years, which promises to inject some volatility into global equity, currency and fixed-income markets.

"We now expect the Fed to cut rates in 25bp increments in the March FOMC meeting in comparison to where we had previously expected a 50bp rate hike since 24 February," says Aichi Amemiya, North America Economist at Nomura.

However, the Nomura view is still a minority one with the majority of institutions looking for a hold or another hike.

"We now expect the FOMC to pause at its March 21-22 meeting because we think that Fed officials will worry that another interest rate hike could be counterproductive to efforts by US policymakers to shore up the financial system," says Jan Hatzius, Chief Economist and Head of Global Investment Research at Goldman Sachs.

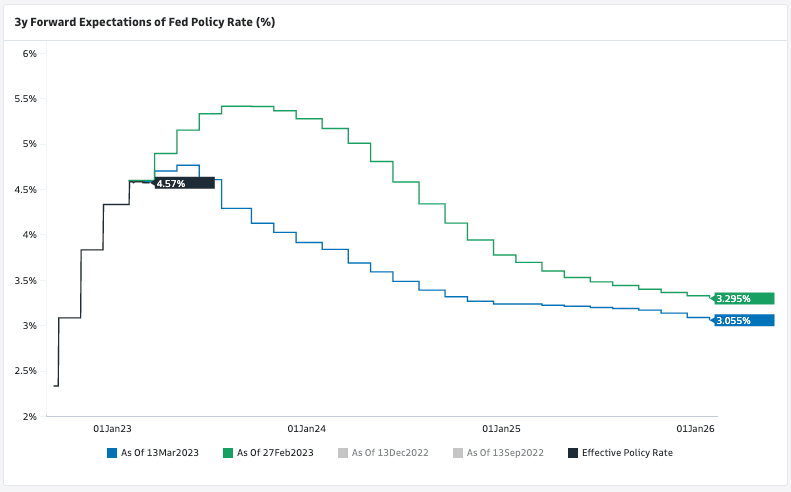

Above: Fed rate hike expectations have retreated sharply. Image courtesy of Goldman Sachs.

Financial markets have rapidly moved to 'price out' another interest rate hike at the March 22 meeting following the collapse of Silicon Valley Bank (SVB) and the smaller Signature Bank.

A 50bp hike had become an odds-on outcome in the wake of Fed Chair Powell's testimony to the U.S. Congress in which he said rates would need to rise to higher levels than previously expected.

SVB's downfall was, in the main, down to its overreliance on longer-term Treasury bonds in its primary portfolio, a class that has taken a hammering as the Fed has raced to raise interest rates to combat red-hot inflation.

The failure signalled that rapidly raising interest rates is not without consequences for the financial system.

Policymakers on the FOMC could therefore display greater caution in considering the pace at which further hikes come for fear further banks and institutions might come under pressure.

"Whether the Fed trusts the additional safeguards now in place to the extent that it will raise interest rates as early as next week (which was not only our firm expectation before the SVB crisis) is not certain. The developments in the financial markets over the next few days will probably determine this," says Bernd Weidensteiner, Senior Economist at Commerzbank.

Money markets show investors see a 70% chance of a 25bp hike in March, with 'no change' commanding 30% odds.

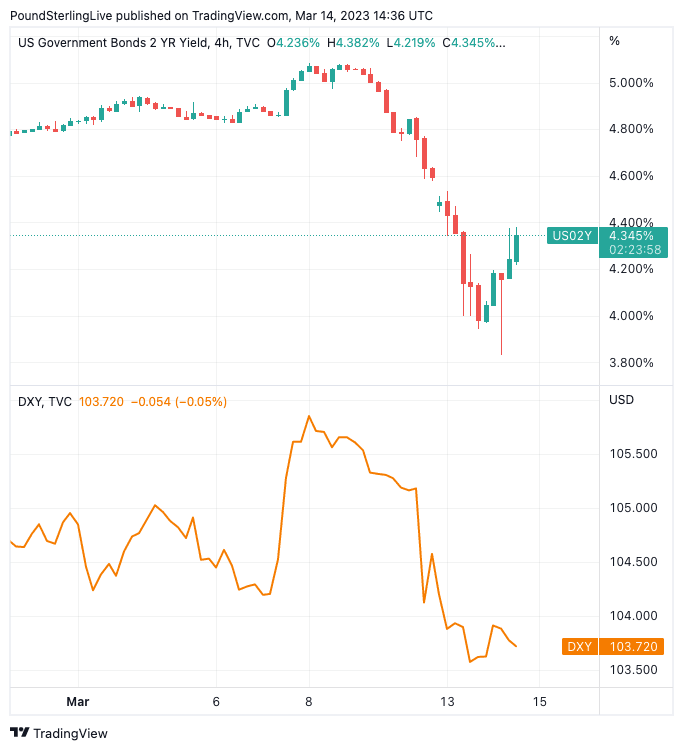

U.S. two-year bond yields have collapsed back to pre-February levels as investors adjust their expectations in a move that has weighed heavily on the Dollar.

Goldman Sachs and others say it is too soon to judge whether the measures put in place by the Fed and other authorities are enough to prevent further financial system deterioration.

"It will be hard to be completely confident in the near term that Sunday’s intervention will halt the pressure on smaller banks, who play a large macroeconomic role and could become considerably more conservative in their lending," says Hatzius.

"With financial stability concerns moving to the forefront, we adjust our call to assume no hike at the upcoming FOMC meeting," says Marc Giannoni, Chief U.S. Economist at Barclays.

Last week, Barclays, like many others, adjusted its Fed call to assume a 50bp hike by the FOMC at the upcoming March meeting, followed by 25bp hikes in May and June.

"Based on the financial market turbulence over the weekend, and signs of a sudden intensification of risk aversion, we now believe that a 50bp hike is off the table for next week and that the decision point will be between a 25bp hike or a pause," says Giannoni.

Above: U.S. two-year yields have stabilised, which could underpin the Dollar from here. (Lower panel: Dollar index).

The Fed will meanwhile be digesting Tuesday's inflation data release that showed inflation remains uncomfortably far off the 2% target, with core inflation coming in stronger than economists were expecting.

The data serves as a reminder that it is highly unlikely the Fed's rate hiking cycle is complete, even if it buys itself some time with a hold next week.

"The strength in core service prices increased the odds of a rate hike from the Fed next week, with just over 25bps being priced in, and that prevented a further depreciation in the USD," says Katherine Judge, an economist at CIBC Capital Markets.

"Consumer price inflation did not show many signs of cooling in the February CPI. Headline inflation rose 0.4%, with the core index up 0.5%. With more than a week to go until the next FOMC meeting, a 25 bps rate hike is still a distinct possibility if financial stresses ease," says Sarah House, Senior Economist at Wells Fargo.

Nevertheless, Wells Fargo joins peers at Goldman Sachs and Barclays in leaning towards a "pause" at the March meeting so that policymakers can digest the significant developments of the past week.

But Bank of America is sticking to a previous call for a 25bp hike on March 22.

"In our view, and in light of ongoing market volatility from concerns around some regional banks, we did not see February's employment report as robust enough to warrant a 50bp rate hike," says Michael Gapen, U.S. Economist at Bank of America.

JP Morgan's U.S. economist Mike Feroli is also sticking with his forecast of a 25bp rate hike while acknowledging rate expectations have clearly pulled back dramatically the last few days on the SVB news.