Image © Adobe Images

The UK still commands a sizeable current account deficit, although it did decline in the second quarter of 2022 and revisions show the first quarter's deficit was smaller than previously anticipated.

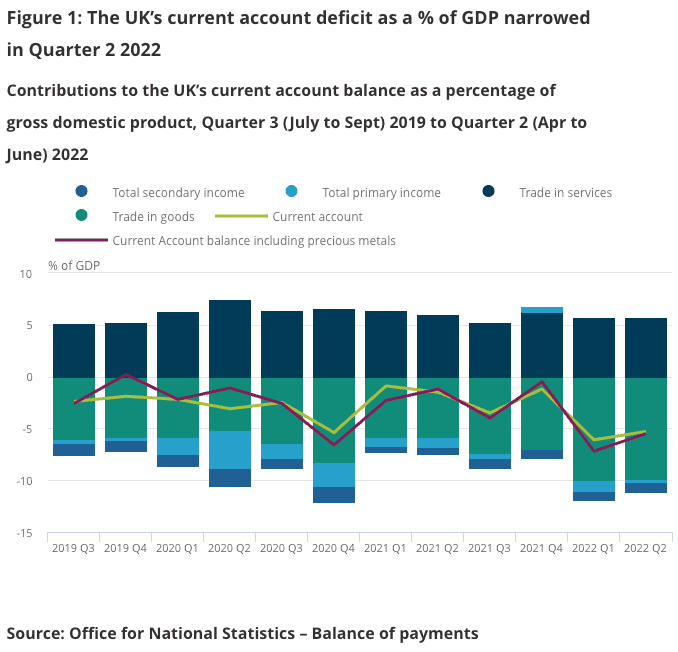

The current account deficit stood at -£33.8BN in the second quarter, still large, but below consensus expectations for a blowout to -£44BN.

In fact, the deficit has shrunk markedly on the first quarter, which stood at -£51.7BN.

The UK's current account balance is a measure of the country's balance of payments with the rest of the world in trade, primary income and secondary income.

Because the UK runs a deficit it must attract foreign investor capital if the value of then Pound is to remain stable, or increase.

Economists have said then Pound is vulnerable to even deeper declines because of the scale of the deficit. For instance, currency strategists at Nomura are forecasting the Pound-Dollar exchange rate to slip below parity largely on account of the deficit.

Therefore, news of its shrinking is, on balance, supportive of the Pound and serves as a reminder that while the Pound can adjust, so too can economic data.

When the erratic trade in precious metals is excluded the current account narrowed in Q2 to £32.5BN (5.3% of GDP) from a deficit of £37.0BN (6.1%) in the previous quarter.

Direct investment income from abroad was the main contributor to the narrowing in Q2.

The scale of the deficit in Q1 has been revised lower to a deficit of £37.0BN (6.1% of GDP), from an initial estimate of £44.2BN (7.1% of GDP).

Again, the revision is largely due to investment income earnings from abroad (credits) being higher than previously estimated.

Revisions to the deficit in Q1 means it now sits below the largest current account deficit on record, which was 7.1% of GDP in Quarter 4 2015.

But the deficit remains sizeable thanks to the increased cost of energy imports, particularly gas.

"The current account deficit remained extremely large in Q2, mainly due to the surge in the cost of energy imports," says Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics.

Tombs says it is likely to grow over the remainder of the year:

"Natural gas futures prices suggest that the overall trade deficit likely will increase to about £40B in Q4 and £45B in Q1 2023, from £26.2B in Q2. This will easily counter the shrinkage of the investment income deficit that likely will be caused by sterling’s recent depreciation; a weaker pound automatically boosts the sterling value of the income generated by the U.K.’s overseas assets."

Pantheon expects the current account deficit likely will increase to about 8% of GDP in Q4 and 9% in Q1 of 2023.

So while today's data provides a rare piece of positive news for the UK and the Pound, the outlook certainly remains challenging.

"It would be foolish to rule out sterling falling to parity against the U.S. dollar, especially given that the pound’s current value relies on expectations of an implausibly sharp increase in Bank Rate. But we expect the government to announce spending cuts when it publishes its Medium-Term Fiscal Plan in November, providing some reassurance to overseas investors that have fled U.K. markets in the last week. Accordingly, we see sterling at around the $1.05 mark at year end, with the further drop being driven by the MPC raising Bank Rate to 4%, rather than the 6% currently priced-in by investors," says Tombs.