- Nordea sees 25bp hike due in December

- Berenberg says March lift-off more likely

- Timing matters greatly for EUR exchange rates

Image © European Central Bank.

Expect a rapid move towards higher Eurozone interest rates says a major Nordic lender who now see a 25 basis point hike coming from the European Central Bank in December, however other economists see significant sequencing speed bumps built into the road ahead that means a March 2023 hike is the most likely lift-off date.

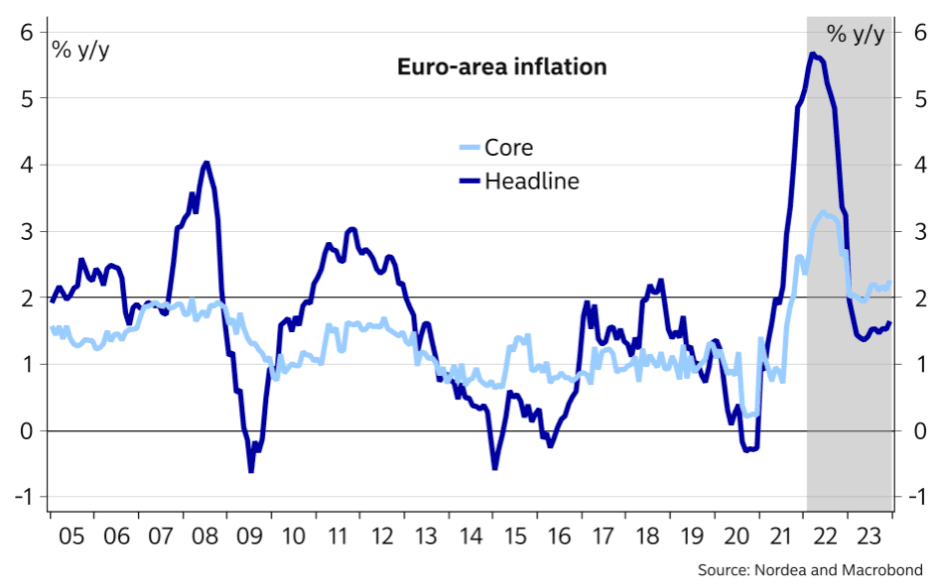

Economists at Nordea Markets say Eurozone inflation pressures are building and they now expect core inflation to stay above 2% in 2023.

"Against this backdrop, the ECB needs to act: we expect a decision to accelerate the taper in March and the first rate hike in December," says Jan von Gerich, Chief Analyst at Nordea Markets.

The timing of interest rate hikes matter for Eurozone fixed income markets and Euro exchange rates which have all risen in response to the ECB's surprise 'hawkish' pivot at its February policy update.

At it's February meeting ECB President Christine Lagarde said members of the Governing Council were now unanimous in their concern inflation was becoming elevated and some action would therefore be required on interest rates to ensure prices stabilised back at 2.0%.

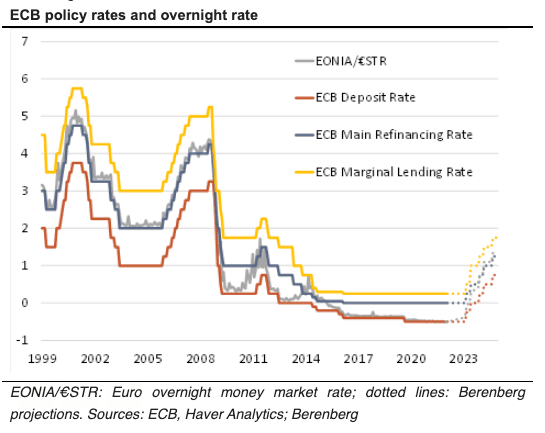

As a result the ECB dropped a previously-held overt commitment to not raising rates in 2022.

Money markets now show investors to be positioned for up to 50 basis points of hikes in 2022, which implies two 25 basis point hikes.

The question for foreign exchange and fixed income markets is whether this hawkish shift in expectations is warranted and can be sustained.

Any pushback against such expectations ultimately leaves the Euro prone to reversals.

"The hurdle for a late 2022 rate hike remains high, especially as an end to quantitative easing and to long-term liquidity injections at generous terms could lift Eurozone money market rates even before and/or by more than the increase in ECB policy rates," says Holger Schmieding, Chief Economist at Berenberg Bank.

Berenberg finds that an end to quantitative easing and reducing reserves will allow the market to bid up short-term rates will in itself tighten monetary policy, even before the main interest rate levers are pulled.

"Over time, the return of overnight rates to their normal position at or just above the refi rate will add some 50bps to the increase in policy rates," says Schmieding.

Given that the ECB cut rates in 10 basis point increments once the deposit rate went below zero, it could follow that the central bank opts to hike in 10 basis point increments.

Such an observation would therefore also imply expectations for up to 50 basis points to be delivered by year-end are unlikely.

ECB Governing Council Member Klass Knot did however say in a weekend interview that there was little reason to doubt a 25 basis point hike could be delivered in 2022, highlighting the impatience some corners of the Governing Council have with the ECB's ultra-easy monetary regime.

Nordea Markets says the 'hawks' have good reason to make a stand, given upward inflation surprises have continued and core inflation pressures are broadening and strengthening faster than they or the ECB had expected.

Nordea Markets anticipates the ECB will again revise its inflation forecasts higher at the March meeting and decide to accelerate the tapering of its bond purchases, so that net purchases will cease around the end of August.

This will allow for the commencement of rate hikes in December, kicking off with a 25bp move.

Further rate hikes are anticipated with another 25bp move coming in March, taking the deposit rate to zero.

Another hike in September 2023 is expected by Nordea, raising the deposit rate to 0.25%.

"Even many of the traditionally more dovish ECB members have started to talk about policy tightening. That many central banks around the world are starting to tighten policy and rate hikes are already being priced in by financial markets makes it easier for the ECB to start hiking rates as well," says von Gerich.

- Reference rates at publication:

GBP to EUR: 1.1864 - High street bank rates (indicative): 1.1550 - 1.1632

- Payment specialist rates (indicative: 1.1757 - 1.1805

- Find out more about specialist rates and service, here

- Set up an exchange rate alert, here

But in an appearance before EU lawmakers on February 07 Lagarde sought to quell some of the newfound haste adopted by investors in their approach to the ECB's policy outlook.

She said there was "no need to rush" on making conclusions as to the ECB's intentions to tighten monetary policy.

Lagarde said on Monday there was "a real chance inflation will stabilise" at the 2% target, which she said would lead to a "normalisation of our monetary policy".

"Taken at face value, the ECB’s February monetary policy statement still seemed to virtually rule out a December 2022 rate hike," says Schmieding. "The ECB repeated its December 2021 schedule for tapering its net asset purchases from c€70bn per month now to still €20bn from October onwards."

Berenberg finds the ECB’s practice to adjust its pace in quarterly steps points to quantitative easing continuing until at least the end of 2022.

"Coupled with the ECB’s vow to raise rates only “shortly after“ the end of its purchase programmes, March 2023 would then be the logical time for a first hike after stopping QE at the end of 2022," says Schmieding.

If Berenberg is right the market will have to calm its recent excitement and some giveback by the Euro becomes likely.