The South African Rand Remains On Road to Recovery, Analysts Say, after GDP Surprise

- Written by: James Skinner

© Lefteris Papaulakis, Adobe Images

Achieve up to 3-5% more currency for your money transfers. Beat your bank's rate by using a specialist FX provider: find out how.

The Rand was rebounding from earlier lows at the start of the new month as global risk appetite picked back up and after having gotten no help from better-than-expected GDP data, although Investec says the South African currency should remain on a recovery path into year-end, but a volatile one.

The Rand was rising and the Dollar retreating Wednesday, continuing a pattern that developed in the prior session when investors took cues from a small reduction in the number of new coronavirus infections in Florida rather than adverse economic or geopolitical developments.

Stocks were in the green and so too were the risk currencies like the Rand that follow them, despite multiple threats to investor appetite.

Investors were heartened when the coronavirus slowed in Florida Tuesday but wobbled overnight when U.S. case growth hit a new daily high and advisers warned of a possible 100k new daily infections up ahead. Markets were up in Europe Wednesday after German retail sales blew economist expectations out of the water, which saw Chinese Foreign Ministry threats against U.S. media outlets go overlooked, along with reports of arrests in Hong Kong due to the 'national security law' imposed there by China.

"SA will start the month with equity market movements most likely in line with global changes in sentiment, and the rand as well. There will be a steady release of manufacturing PMIs which, if they continue their V-shaped recoveries, should keep market activity positive. For the rest of us, we can hope the weather goes the same way," says Siobhan Redford at Rand Merchant Bank.

Above: USD/ZAR shown at hourly intervals alongside S&P 500 index futures (orange line).

Markets are prone to knee-jerk reactions to the ebb and flow of virus-related data, which is part of why South Africa's Rand is also tipped to remain volatile as it treads a zigagging path to recovery from punishing losses in the opening quarter. Investec forecasts the Rand will drag USD/ZAR down to 16 by year-end after reaching 16.50 by the end of the third quarter, if-not before.

"With QE globally set to be larger and longer than that experienced after the 2008-2009 financial crisis, it is no surprise that the rand has bounced back so quickly, from R19.35/USD in April to R16.33/USD by June, a rapid run which pushed it into overbought territory," says Annabel Bishop, chief economist at Investec. "After some necessary recent consolidation [the Rand] is likely to largely remain around current levels into Q3.20, and then strengthen somewhat further. The rand is however also likely to remain highly volatile."

A global rebound that lifts commodity prices would help the Rand and is a factor in Investec's outlook, combined with central bank policies that burnish the appeal of South African bond yields. SA yields are higher than developed world counterparts and give many emerging market rivals a run for their money.

Others see the appeal of South African bonds under threat and are concerned about the prospect of the public finances and pledged fiscal consolidation serving to hamstring the economic recovery.

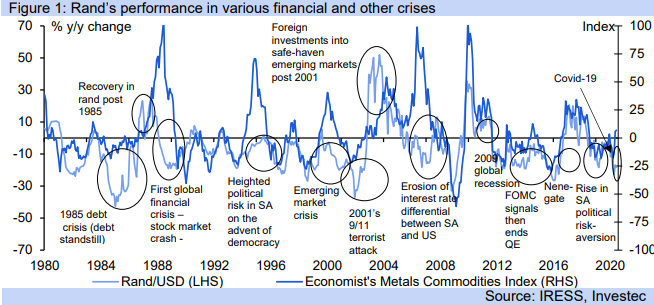

Above: Investec graph showing performance of ZAR/USD throughout various crises.

"Last week’s supplementary budget provided a list of policy initiatives whose implementation President Ramaphosa will struggle to secure political support for from his ideologically divided ANC coalition. Political infighting and half-way measures will likely result, thus eroding the hoped for economic recovery," says Larry Brainard, a senior economist at TS Lombard, an independent investment research provider. "Risks on the horizon for bond investors include the possibility that the Treasury might introduce a “prescribed asset” regime. Such a move is allowed under Regulation 28 of the Pension Funds Act, in which pension funds would be required to hold a specified portion of their assets in government paper. Such a regime of yield curve control could trigger an outflow of non-resident holdings."

South African bond markets were lifted last week when Finance Minister Tito Mboweni said in his supplementary budget update that the government will deliver a primary budget surplus by 2023/24.

Markets hadn't expected the budget to return to balance until some time after even before the country was burdened by the extortionate cost of the coronavirus containment, so last week's commitment was a meaningful offering.

"The deepening of the recession is set and thus priced into the ZAR exchange rate. However, markets are likely to be interested above all in how quickly the economy will come out of the trough - in particular in comparison to others. This is likely to be above all a question of time and (financial) resources," says Elisabeth Andreae, an analyst at Commerzbank.

Many are sceptical that a surplus will be delivered though, partly because of the government's poor track record but also because the R500bn coronavirus-related support of the economy will add significantly to the deficit, even though it's substantially funded by international organisations.

Above: USD/ZAR shown at daily intervals alongside Pound-to-Rand rate (orange line) and selected moving-averages.

"The IMF's decision on a USD 4.2 billion loan application to support the fight against the corona pandemic is still pending," says Andreae, who forecasts a USD/ZAR rate of 17.0 for year-end. "Although a credit commitment could give the rand a short-term boost, we believe the upside is rather limited given the risks. It is likely to remain vulnerable, especially if the risk appetite declines - for example in the wake of rising new infections."

The Rand got no help Tuesday when Statistics South Africa said the economy shrank -2% in the first-quarter, despite markets looking for a -3.8% fall.

This makes for a third-consecutive decline and a three-quarter recession that had been flagged as likely by Investec in late 2019. Most sectors shrank last quarter despite just a handful of days under 'lockdown,', although agriculture, foresty and fishing saw output increase while there were also gains in financial, real estate and business services, in addition to government services.

"South Africa’s economic lockdown came into effect on March 27, but the effects of the Covid shock began to be felt prior to this," says Andrew Matheny, an economist at Goldman Sachs. "We interpret the fact that the contraction was smaller than our modeling (and consensus expectations) envisaged as likely to have a bearing on the timing of the Covid shock rather than its magnitude. Thus, we shift more of the weakness in our forecast into Q2, where our modeling now suggests a 35% annualized contraction in GDP for the quarter, and we leave our full-year growth forecast of -7.5% unchanged."