New Zealand Dollar Leads the Pack Following Q1 Inflation Print

- Written by: Gary Howes

Image © Adobe Images

The New Zealand Dollar is the day's top-performing G10 currency after it was revealed New Zealand inflation remains far too high for the Reserve Bank of New Zealand (RBNZ) to cut interest rates.

The Pound to New Zealand Dollar exchange rate fell to a daily low at 2.1042 after Statistics New Zealand said inflation rose 0.6% quarter-on-quarter in the first quarter of the year, taking the annual rate of increase to 4.0%, double the RBNZ's target. This is also above the RBNZ's most recent forecast of 3.8%.

A measure of core inflation - non-tradeable inflation - fell from 5.9% to 5.8% y/y, defying consensus expectations for a greater decline.

"Non-tradeable CPI is a gauge that has been monitored closely by the RBNZ as they attempt to isolate underlying price pressures from commodity-driven swings in the headline rate," says Francesco Pesole, FX Strategist at ING Bank. "We think today’s data in New Zealand endorses the hawkish stance displayed by the RBNZ at the April meeting."

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

The New Zealand Dollar has risen by three-quarters of a per cent against the U.S. Dollar in the hours following the inflation print, with NZD/USD now quoting at 0.5913.

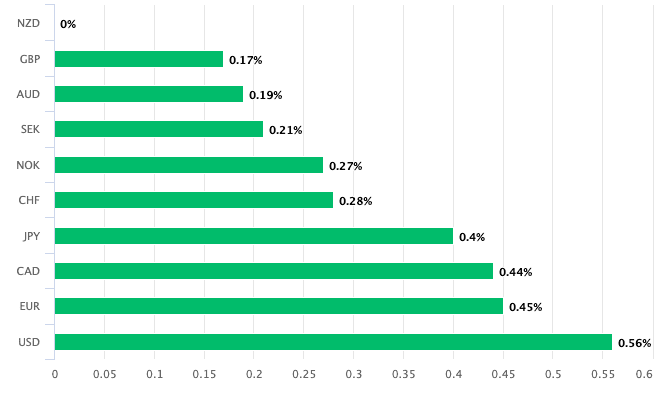

For the New Zealand Dollar, these inflation data re, on balance, a supportive development and is reflected in the currency's outperformance against all G10 peers on the day:

Above: NZD performance on April 17. Track NZD with your own custom rate alerts. Set Up Here

In short, a mid-year interest rate cut is unlikely and Kiwis will likely have to wait until towards the end of the year before the pressure is released.

"The details presented a much less convincing story of underlying disinflation than meets the eye," says Henry Russell, an economist at ANZ. "The suite of core measures moderated, but by less than we had anticipated."

Russell points out that at the 30% trim level, inflation eased from 5.0% y/y to 4.5% y/y. Weighted median inflation was unchanged at 4.4% y/y. CPI excluding food, fuel, and energy was also unchanged at 4.1%.

ING's analysis reckons the slow fall in non-tradeable inflation mirrors the ongoing pressure from the sharp rise in net immigration in New Zealand.

Markets are pricing in 35bp of cuts by year-end (just one cut, with 50/50 odds of a second). "Our call is for 50bp of easing in New Zealand this year, starting from October, although there are risks that an immobile Fed and sticky inflation in New Zealand force the RBNZ to deliver only 25bp or none at all," says Pesole.

The boost to the New Zealand Dollar is nevertheless likely to be limited as the global pulse remains firmly in control of this 'high beta' currency. If global markets continue to decline in light of the significant decline in expectations for Federal Reserve rate cuts, the NZD will likely come under pressure.

"The centrality of risk sentiment in NZD trading now makes domestic factors almost irrelevant. NZD/USD may extend its slide to the 0.5800 support in the near term," says Pesole.