Oil Production Cut Reflects OPEC Weakness say Economists

- Written by: Gary Howes

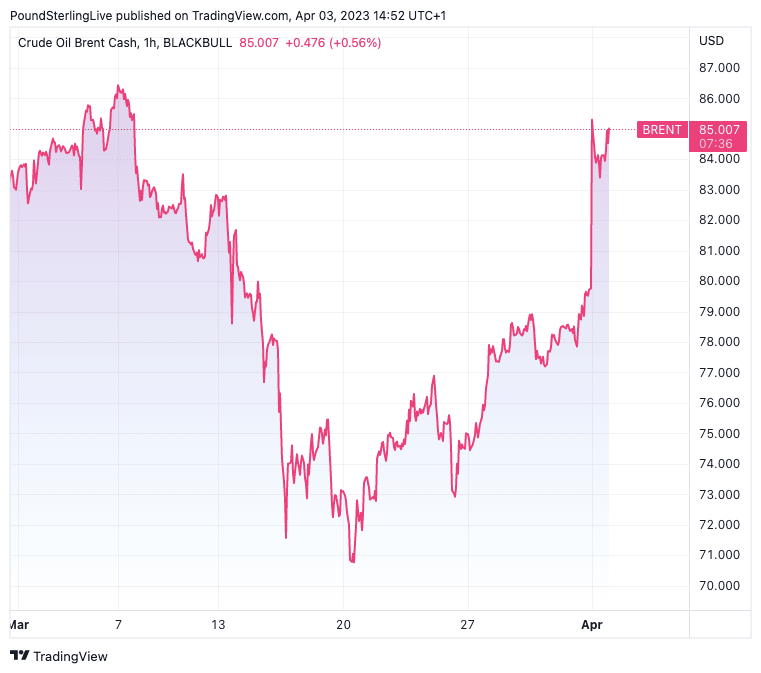

Above: Brent crude oil prices at one-hour intervals.

OPEC+ sent oil prices surging after announcing an unexpected cut to production, but some economists say the decision could in fact reflect the weakened position of OPEC in the face of slowing global demand.

The cartel announced it would cut output by a million barrels a day, a move that comes mere days after delegates had signalled it had no intentions of changing production limits.

The surprise caught the oil market off-guard and resulted in a sharp rally in the price of key oil benchmarks, a strategic move that looks designed to punish traders for betting heavily on further price declines.

The outcome meanwhile prompted analysts at Goldman Sachs to raise Brent oil price forecasts for the year by $5 a barrel to $95/barrel.

"OPEC+ has very significant pricing power relative to the past, and today’s surprise cut is consistent with their new doctrine to act pre-emptively because they can without significant losses in market share," says Daan Struyven, an economist at Goldman Sachs.

But other analysts don't read the developments as fundamentally bullish for oil price prospects, suggesting OPEC is in fact acting from a position of weakness as it is global demand that is the ultimate arbiter of sustainably elevated oil prices.

"All in all, the cut does not change our view on the oil market, as OPEC+ is acting from a position of weakness, not a position of strength," says Carsten Menke, Head of Next Generation Research at TS Lombard.

Menke says the decision will likely prop up oil prices in the (very) short term, but the cut confirms his medium- to longer-term expectation of a more than sufficiently supplied market.

"The fundamentals are hinting at oil prices in the 70s in the longer term, and we stick to our Neutral view for now," sasys Menke.

The most recent OPEC decision adda to the two million barrels per day reduction agreed by OPEC+ back in October, taking the total to around 3% of global supply.

"The cartel is trying to put a floor under crude prices against the backdrop of rising inventories and downside risks to demand as a US recession looms," says Konstantinos Venetis at TS Lombard.

Venetis says the move was in part supposed to send a message to speculators whose bearish skew in futures positioning had become particularly pronounced recently.

The TS Lombard analyst also acknowledges a political angle to the timing of this announcement as it follows news that U.S. officials had effectively ruled out new crude purchases to replenish the Strategic Petroleum Reserve in 2023.

"Near term, this will deter short sellers and help oil prices settle higher – much like what December’s surprise BoJ tweak to Yield Curve Control did for the yen," says Venetis.

But he adds:

"In our experience, however, as a rule the recipe for sustainable oil market turnarounds is positive demand surprises, not pre-emptive supply reductions. Just like the production cuts announced in autumn 2022, this essentially amounts to a defensive move in the hope that the world economy skirts a severe economic downturn in 2023."

TS Lombard says expectations for a U.S. recession and limited global spillovers from China’s reopening, our sense is that at this juncture sticky oil prices are more likely to weigh on growth than arrest the broad disinflation process already under way.

"For commodities overall, the glass still looks half empty: we continue to expect rangebound trading in 2023 Q2, albeit with metals’ outperformance over energy starting to erode as the Brent-to-copper ratio mean-reverts higher," says Venetis.