Above: File image of Jeremy Hunt by Simon Dawson / No 10 Downing Street.

The government could have up to £20BN in additional headroom to play with at the time of the March budget, according to an analysis that follows the latest set of UK borrowing figures.

The ONS reports the government borrowed significantly less than expected in December amidst rising tax take and reduced expenditure, offering Chancellor Jeremy Hunt the space to announce meaningful giveaways in the budget.

"December’s better-than-expected public finances figures brought some cheer for the Chancellor after the recent run of poor outturns and will give him a bit more wiggle room for a big pre-election splash in the Spring Budget on 6th March," says Ruth Gregory, Deputy Chief UK Economist at Capital Economics.

Capital Economics reckons Hunt will find additional "headroom" against his fiscal mandate of about £20BN in the Budget, up from £12.9BN in the November Autumn Statement.

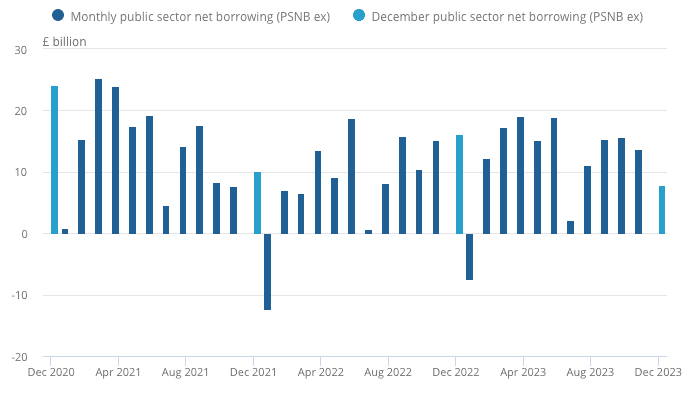

The UK reported government borrowing in December 2023 at £7.8BN (consensus forecast = £11.0BN), which is around half the amount borrowed in December 2022 and the lowest December borrowing since 2019.

A smaller-than-expected deficit in December and favourable revisions mean that borrowing in the year to date was £5BN lower than the latest forecast issued by the Office for Budget Responsibility.

Borrowing in the prior months of the 2023/24 fiscal year was revised down by a total of £5.0BN.

An increased tax take and falling debt repayments are largely behind the improved finances.

The ONS said the year-on-year increase in public sector receipts was largely because of growth in VAT and income tax receipts.

Total tax receipts of £81.5BN were registered in December, which is £4.8BN above that seen in December 2022, but were £1.8BN below the OBR's forecast of £83.3BN.

Image courtesy of Capital Economics.

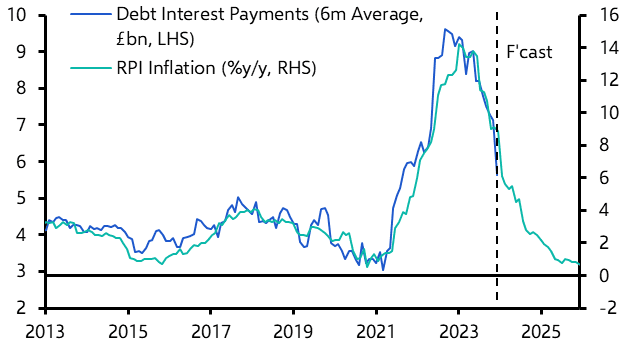

The interest payments on debt have fallen as the increase in the Retail Price Index (RPI) has slowed markedly from a peak of 14.2% year-on-year.

Debt interest stood at £4.0BN in December 2023, which is £14.1BN less than in December 2022.

The UK is uniquely exposed to this inflation-linked debt which accounts for approximately 25% of the debt basket, as opposed to around 10% in other comparable economies.

Image courtesy of Capital Economics.

Simon French, an economist at Panmure Gordon, explains this type of debt proves painfully expensive to hold when inflation is on the way up, but it is now proving a tailwind as inflation comes down.

Total government expenditure was £5.4BN lower than a year ago and a sizeable £8.4BN below the OBR's December 2023 forecast, thanks largely to the decline in interest repayments.

Encouragingly, Gregory says falling inflation is set to drive down debt interest payments further, perhaps to just £2BN by early 2025, suggesting December’s undershoot is not a one-off and will continue in future years.

Rhys Herbert, an economist at Lloyds Bank says the UK government borrowing data supports tax cut hopes in the upcoming March budget.

The OBR said in December that the remainder of the fiscal year would see borrowing rise more slowly than in 2022/23 because tax receipts were expected to be stronger.

"Today’s data seems to support that view," says Rhys Herbert, an economist at Lloyds Bank, adding that next month's data for January will include self-assessment income tax and be particularly revealing about the potential room Chancellor Hunt has for tax cuts.