- Omicron’s impact on growth less than feared

- Late January pick-up bodes well for February

- Rebound indicates continued recovery in Q1

- But inflation subdues growth overall in 2022

Image © Adobe Images

The UK economy weathered the emergence of another edition of the coronavirus better than had been expected during the final quarter last year, according to official data released on Friday, and some economists suspect it’s already recovering from that autumn setback.

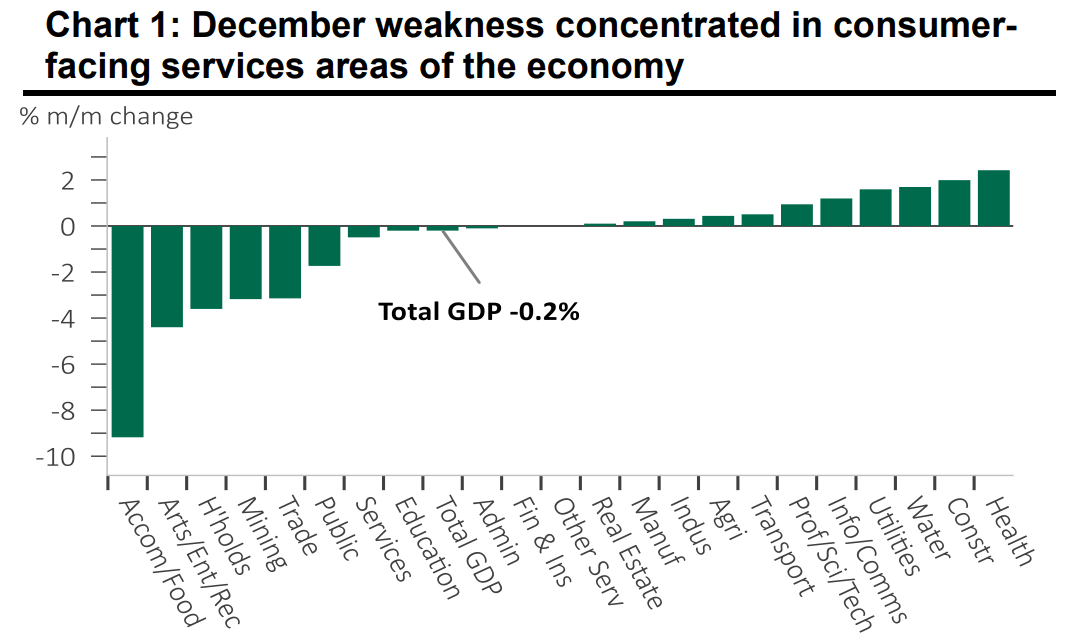

UK GDP fell 0.2% in December as companies and households scaled back activity and spending following the late November emergence of the Omicron strain of the coronavirus, which left the economy growing at a quarter-on-quarter pace of 1% in the final three months of the year.

The consensus or average of economist estimates had suggested that a larger 0.5% decline was likely for December and that quarterly GDP should have been a bit faster at 1.1%, although the final quarter expansion may have been adversely impacted for statistical reasons when the Office for National Statistics revised down its estimate of third quarter growth from 1.3% to 1.1%.

“The negative impact of Omicron on the economy seems to be receding quickly particularly as most restrictions have now been removed again. It is not yet clear whether GDP will have fallen again in January but indications that activity rebounded sharply in the second half of the month point to a sizeable increase in GDP in February,” says Nikesh Sawjani, a UK economist at Lloyds Commercial Banking.

Source: Lloyds Commercial Banking.

“Today’s release means the UK economy recorded solid yearly growth of 7.5% in 2021, with monthly GDP judged to be in line with its pre-pandemic (February 2020) level of output (courtesy of some upward revisions). Differences in methodology, however, meant that on a quarterly basis, GDP was judged to still be 0.4% below its level from Q4 2019,” Sawjani also said.

The latest assessment by the Bank of England (BoE) suggested last week that GDP would be likely to fall in December and January before recovering over the remainder of the opening quarter, although Lloyds’ Sawjani and colleagues say there’s a chance of the economy surprising on the upside for the new year period and that it could also stage a swift comeback by February.

However, the overall pace of economic growth beyond that point is widely expected to be subdued by recent increases in inflation that have raised the cost of living and which could limit companies and households in their ability to spend over the coming quarters.

“It’s possible that GDP fell in January as that’s when Omicron cases peaked and many couldn’t work. But timely indicators suggest activity began to recover from the middle of the month,” says Paul Dales, chief UK economist at Capital Economics.

Source: Capital Economics.

“Together with today’s news that the economy coped with the start of the Omicron wave in December better than we thought, we have revised up our forecast for GDP in January from a 0.5% m/m fall to 0.0% m/m. Either way, a 2.0% fall in real household disposable incomes this year (due to the effects of higher inflation and taxes) will restrain GDP growth from April,” Dales also wrote in a briefing to clients on Friday.

UK inflation reached a multi-decade high of 5.4% in December and is widely expected to rise further over the coming months as the impact of rising wholesale energy prices and other production costs make their way through into consumer prices.

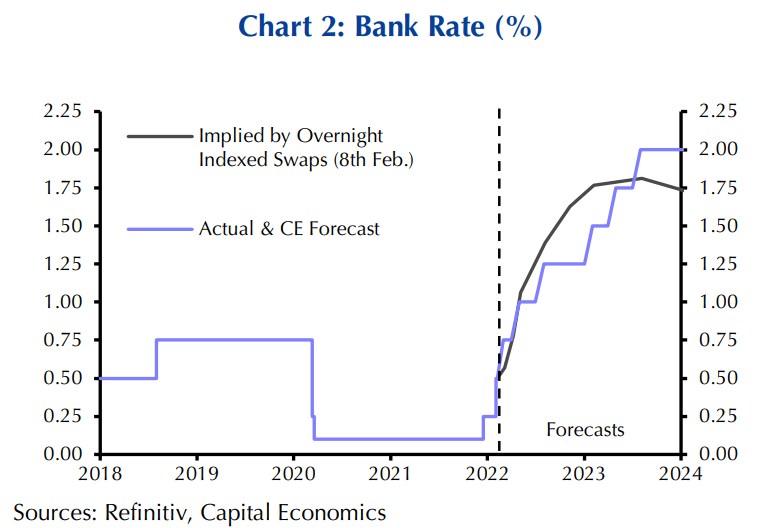

This is a part of why the Bank of England has begun to withdraw the interest rate cuts announced at the onset of the pandemic in 2020, which reduced Bank Rate from 0.75%, and is an underlying factor behind why many economists and even the BoE itself now expect interest rates to rise some distance above that earlier level in the year ahead.

“We now think that Bank Rate will rise from 0.50% currently to 1.25% sooner than we previously thought. What’s more, we now expect three more 25 basis point (bps) rate rises in 2023, resulting in rates ending next year at 2.00%. That compares to the previous peak in our forecast of 1.25% and the peak of 1.75% priced into the financial markets,” says Capital Economics’ Dales.

“The main reason why we now think interest rates will need to rise to a peak of 2.00% in 2023 is because we believe that as a result of the labour market staying tighter for longer, wage and price pressures will be more persistent,” Dales and colleagues said in a note to clients earlier this week.