EUR/USD Forecast: Should be as High as 1.24 - 1.28 say Danske

- Written by: Gary Howes

Danske Bank research suggests that markets are mispricing the EUR to USD rate and if they are correct then the pair should move significantly higher this year.

New research on the prospects facing the euro / dollar rate in 2016 suggest the currency pair is undervalued and should be sitting above 1.20 by some estimates.

Of course currency analysis is a game of weighing probabilities and arguments. Danske concede that there is one argument for a lower EUR/USD based on the relative interest rate level difference between the US and Eurozone.

The differential still advocates for a higher US dollar.

Nevertheless, there are several arguments for a lower euro.

“EUR/USD is substantially undervalued,” says Christin Tuxen, Senior Analyst with Danske Bank who cites external balances as being one reason. “The EU/US CA differential is at its widest level since 2004 - 06.”

Further reasoning for the call is the observation that cyclical drivers are moving in favour of the Eurozone as the business cycle there now looks stronger than the US cycle.

Tuxen also notes that positioning is overstretched in the US dollar's favour with speculators overwhelmingly tied into the short EUR/USD play. As such, the impact of relative rates is fading; and relative rates is the sole argument for a weaker euro / dollar in Danske's view.

Terms of trade are also arguably moving in Europe’s favour with 'lower oil for longer' now becoming a EUR positive.

Finally Tuxen argues that commercial FX hedging of EUR is set to fall, which should support EUR/USD.

“EUR hedge ratios likely to drop as EUR/USD forecasts are no longer being revised lower to the same extent as was the case in 2014 – early 2015,” says Tuxen.

Be under no doubt though that the European Central Bank (ECB) will not be receptive to a higher euro and could well stoke the currency war by announcing aggressive easing action in coming weeks.

The problem the ECB faces argue Danske Bank is that the ECB is already aggressively priced by markets. The central bank may simply no longer have the firepower left in their arsenal to prompt a substantial weakening in the euro.

All the while US Federal Reserve policy is unlikely to spur US dollar strength

As we have been observing of late the prospect of four interest rate rises in 2016 is now highly unlikely ensuring a once crucial pillar of support for the Greenback has fallen away.

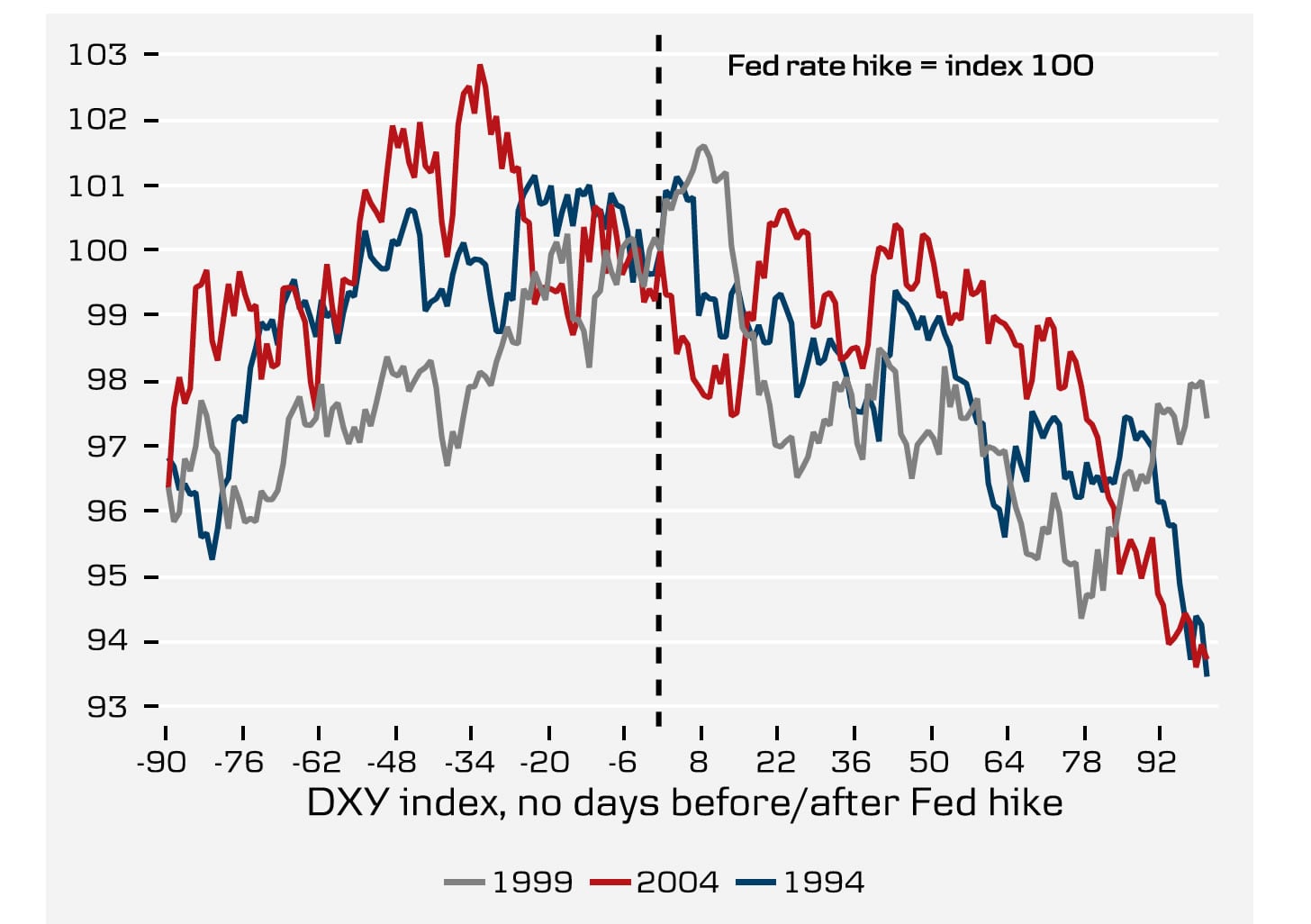

And anyway, if we look at the below; the response of the US dollar index to the interest rate cycle is actually negative if historical context is to be drawn on. In short, the dollar tends to benefit in the run-up to the first hike, and not necessarily in the wake of the hike.

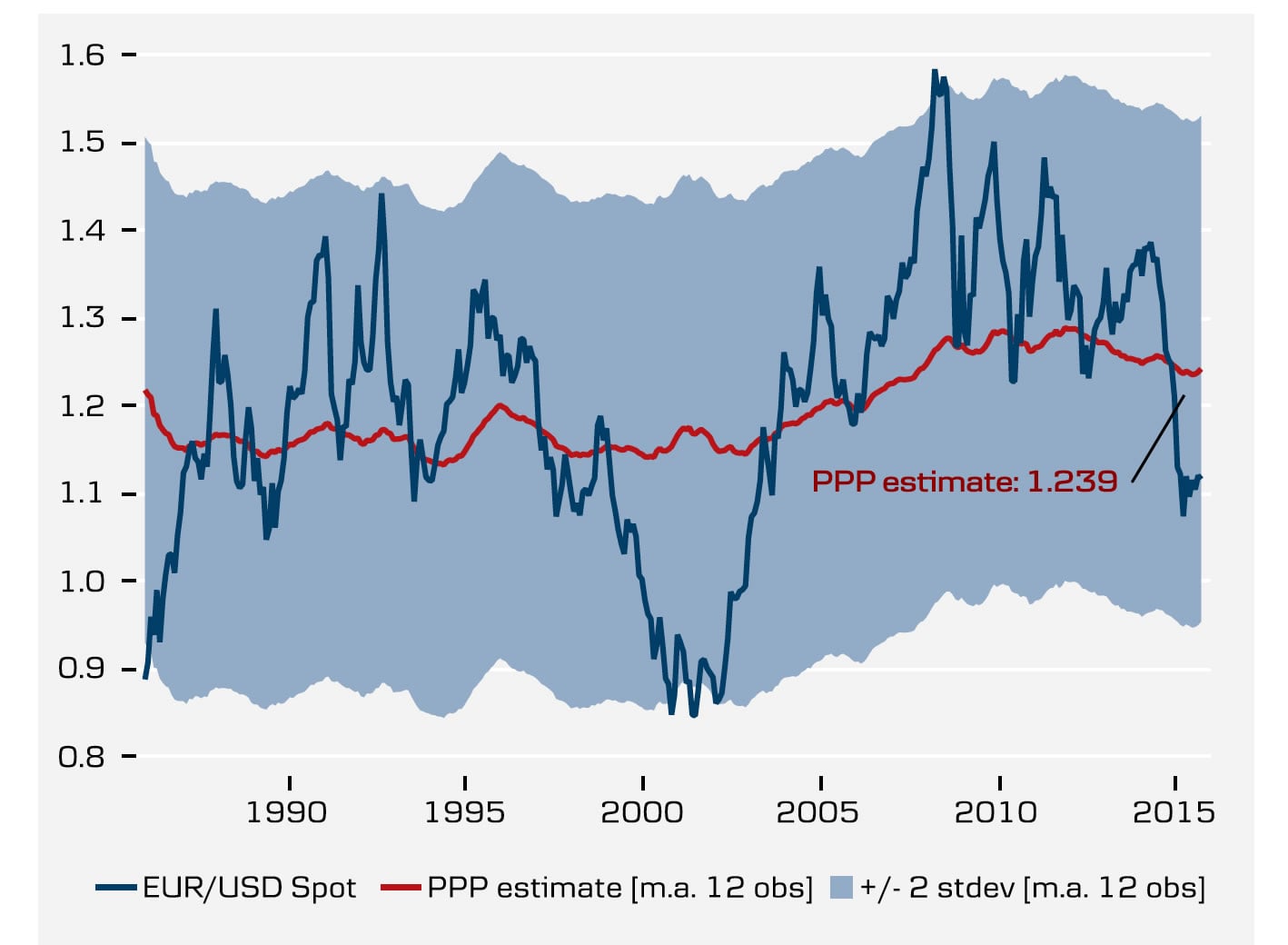

Danske Bank’s Medium-Term Valuation Model actually suggests that the euro to dollar exchange rate should be at 1.28, not the 1.11’s we are presently seeing.

Furthermore, Danke’s Purchasing Power Parity calculation suggests that 1.24 is the longer-term fair value level.

Danske Bank argue that clients should be ready for the EUR to appreciate in effective terms if their FX forecasts prove right and the effective euro exchange rate returns to early 2015 levels in 12 months.

ECB would not have accepted euro appreciation in 2015 when the Harmonised Index of Consumer Prices (HICP) was in deflationary territory.

HICP is an indicator of inflation and price stability for the ECB.

“But tolerance for EUR appreciation higher as inflation creeps up,” argues Tuxen.

Uncertainty Increasing, Fed Could Step Away from Rate Hikes

Economic uncertainty increased further yesterday after the disappointing German production and external trade figures for December and it is questionable whether today's production figures in France and Italy will lead to a turnaround in sentiment, even if the month-on-month results rise as expected.

Market participants will be focusing on the US over the next two days, as Fed chair Yellen will present her semi-annual testimony to the finance committee of the House of Representatives.

"The mixed data, as well as the stock market turmoil of recent weeks above all, have led to any remaining rate hike expectations for March being priced out and such a move is now considered unlikely for 2016 as a whole," says Ralf Umlauf at Helaba Bank in Frankfurt.

"The euro has been remarkably robust amidst the current turbulence, although the EMU spread universe has also begun to simmer.

"The euro has been remarkably robust amidst the current turbulence, although the EMU spread universe has also begun to simmer,” says Umlauf. “The euro also remains at an advantage from a technical perspective and the resistances at 1.1320 and 1.1380 are coming into view. Our favoured trading range: 1.1200 - 1.1350.”