GBP/AUD on the Rise After Jobs Data; Triangle Poised to Break Higher

The GBP/AUD pair is looking poised to strengthen in the short-term but in the medium-term there are indications the up-turn in the pound’s fortunes may be short-lived.

The pound is strengthening following positive employment data, and it looks set to rise even further versus the Australian dollar in the imminent future, but a combination of technical and fundamental factors show there are substantial risks to sterling beyond that, in the short-to-medium term.

Looking at the pair from a technical perspective reveals why we might be bullish in the very short-term: the four-hour time-frame chart is showing tthe formation of a possible ascending, or right-angled triangle, with bullish implications.

Unlike normal triangle patterns, right-angled triangles provide clues as to which direction the exchange rate will breakout after they have completed.

They always possess at least one flat edge and the exchange rate is most likely to break out in the direction of the flat edge, which in this case means up, leading to a rise in the exchange rate.

Such a breakout would probably be confirmed by the exchange rate moving above the 1.7636 highs, which would likely lead to an extension up to an initial target at 1.78, followed by 1.79 and then an eventual potential final target at 1.80 – calculated from extrapolating the height of the triangle at its tallest point higher from the point of the break.

With July PMI's on Friday presenting markets with the first really important piece of economic data post-Brexit, there is a chance that a strong reading my help beat the Brexit blues and orchestrate a breakout from the pair's ascending triangle.

The daily chart is more bearish, however, as it shows the exchange rate having formed what is potentially a bearish ‘flag’ pattern.

These are continuation patterns, which means they tend to result in a continuation of the trend, which in this case means more downside.

A break below the 1.7000 level would confirm the flag pole was extending lower, with an eventual target at roughly 1.65, calculated by extrapolating the length of the move prior to the formation of the flag down.

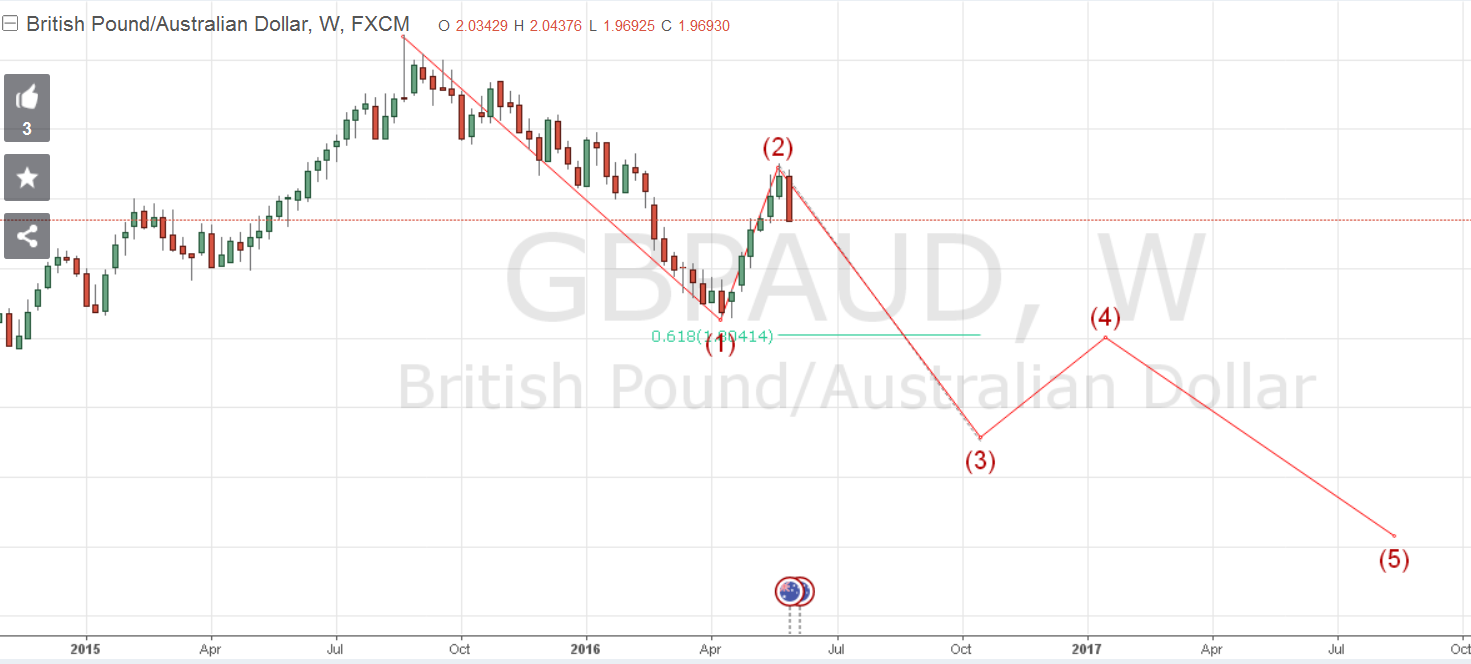

Elliot Wave outlook bearish longer term

Elliot waves (EWs) are a type of advanced cycle analysis technique used by analysts to forecast future prices.

The EW's on GBP/AUD they are indicating probably more downside longer-term.

In late June, Blogging Elliotician Jake66, on TradingView.com said he was, “Shorting wave 3 down to 1.65000.” (See pic below).

His analysis suggests that after 2015 we began a strong impulse wave down which is likely to go all the way to the mid-1.60s.

The recovery rally in April was a smaller wave (2 ) within the larger wave down, and we are on the cusp of beginning a strong move down, or wave (3).

Wave 3's tend to be the strongest most impulsive waves.

Then bearish Elliot wave outlook together with the monthly death cross do not augur well for the pair longer-term.

Westpac’s G10 portfolio algorithm picks AUD as top currency over the short and medium term

The expectation of more downside for the pair chimes to a certain extent with Aussie Bank Westpac’s analysis using their currency picking algo.

According to their FX G10 model the AUD should have the biggest share of a G10 currency portfolio, with 22.7% of the total share.

This is based on the outlook for the domestic economy, yield differentials and commodity prices - which have risen from extreme lows recently.

“Steadier commodity prices, lower core yields and low and falling risk premia across a range of global markets have tilted our logit signal in AUD’s favour for the better part of the last several months, even allowing for a setback around Brexit.” Commented Richard Franulovich, Westpac’s FX Strategist in a recent note explaining the results.

Sterling could weaken further on longer-term risks

Assuming the technical signals outlined above, which are essentially indicating more weakness for the pound, are relatively accurate, then we might very well speculate as to what could cause a further sell-off in sterling.

Clearly the risk that the UK loses its trade privileges during Brexit negotiations, is one source of currency vulnerability, especially concerning things like the EU Passport which allows UK financial services to operate freely across borders.

In a recent article written by ING’s FX Strategist Viraj Patel, the author notes three sources of risk weighing on the outlook for the UK’s sovereign credit rating, according to feedback from credit rating agencies.

One such risk is that Scotland decides to have another referendum on independence.

This could come about because the majority of Scots voted to stay in the EU and they might use this fact as a reason to call another referendum on independence, if they wanted to break away and remain in the EU.

Another referendum would cause a substantial amount of uncertainty in the UK which would probably lead to a further slow-down in the economy, and could bring the UK closer to suffering a credit downgrade.

In the last Scottish referendum, the pound weakened on the uncertainty caused then and the same would be expected again.

The next source of risk according to ING’s Patel comes from the pound losing its status as a reserve currency.

Currently 4.8% of the world’s reserves are held in sterling, but if this were to fall to below 3.0% - for example if the pound continued to weaken - then it might lose reserve status.

This too could trigger a credit downgrade.

The third and final potential nightmare scenario for sterling comes from a pre-existing problem – the country’s oversized current account deficit.

This has reached record proportions in the run up to and since Brexit as foreigner’s turned their back on UK financial assets and inbound investment dried up to a dribble.

It was the popularity of UK stocks, shares and bonds amongst foreign investors which had helped offset the gaping hole in the trade balance due to England’s now decades old problem of not exporting enough and importing too much.

Patel suggests that a continued widening in the current account deficit could be the trigger for a credit downgrade, which would also push down the value of sterling substantially.