GBP/USD: "Underperformance is Certainly the Near-term Risk" Says ING

- Written by: Gary Howes

File image of Andrew Bailey © Pound Sterling Live, Still Courtesy of Bloomberg TV.

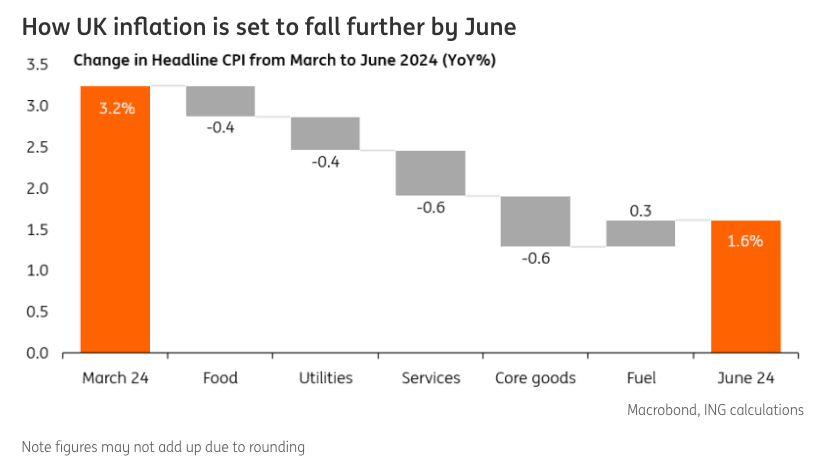

The Bank of England is turning dovish as there is further disinflation in the pipeline in the UK, which should keep the Pound under pressure.

This is according to an analysis from ING Bank, following recent signals from Bank of England policy setters that a June interest rate cut is likely.

"The Bank of England is trying to tell us something, and markets are finally starting to take notice," says James Smith, Developed Markets Economist at ING. "Investors now expect two rate cuts in the UK this year, starting in August. This repricing could have further to run."

Bank of England Governor Andrew Bailey said in April the Bank could cut interest rates at any of the upcoming meetings and UK inflation is "rather different" from U.S. inflation dynamics. Deputy Governor Dave Ramsden said last week said the UK was no longer an inflationary outlier and "domestic inflation pressures are receding".

Pound Sterling has been widely sold due to this signalling; the Pound to Dollar exchange rate has fallen 2.25% already in April, and analysts say more weakness is likely.

GBP to USD Transfer Savings Calculator

How much are you sending from pounds to dollars?

Your potential USD savings on this GBP transfer:

$1,702

By using specialist providers vs high street banks

Data so far in 2024 shows U.S. inflation is reaccelerating and expectations for Fed rate cuts have been lowered dramatically. Previously, markets had expected the Bank of England would follow the interest rate path of the U.S. Federal Reserve, owing to concerns that UK inflation might follow suit. This meant fading U.S. rate cut hopes resulted in fading UK rate cut expectations.

It also meant the Pound was an outperformer alongside the Dollar. However, the Bank of England is ready to diverge from the Fed, which implies a weaker Pound.

"The current chorus of optimism on the inflation outlook among key BoE figures, therefore, feels both intentional and significant. And we could see the Bank’s signalling on rate cuts becoming bolder still in the coming days, given the realignment of market pricing has only just begun," says Smith.

Market implied expectations show investors are now priced for two rate cuts in 2024, with a first 25bp cut fully priced in for August and the odds of a June cut being a 50/50 call.

But the consensus amongst economists surveyed by Bloomberg last week favours a June cut. Therefore, further repricing in a GBP-negative direction must continue as June is yet to be 'fully priced'.

It looks as though May's Bank of England policy meeting will deliver the required final repricing as more members of the MPC will vote for a cut. The guidance from the Bank will also make it clear a cut is coming.

"If the Bank waters down the language on rates needing to stay restrictive for "an extended period", that would be tantamount to signalling policy easing is imminent. It would probably be a catalyst for us to switch our base case to a June rate cut. And if that happens, it would have the potential to be a big market mover," says Smith.

What will happen to the Pound?

Smith's colleague, Chris Turner, says to expect the greater differentiation between the Bank and Fed cycles "to particularly weigh on GBP/USD".

"At an extreme, say 50bp, swing in the GBP:USD one-year swap differential in favour of looser BoE policy, the relationship since the start of 2023 suggests GBP/USD should be trading closer to 1.21. In short, it looks like some further sterling under-performance is certainly the near-term risk," says Turner.