Bank of England in No Rush to Normalise, Pound Falls Following June Statement

- Written by: Gary Howes

- GBP falls in wake of BoE decision

- Bank strikes optimistic tone on the outlook

- Raise economic forecasts

- See inflation bump as temporary

- But markets were looking for an outright 'hawkish' message

Image © Adobe Images

- Market rates at publication: GBP/EUR: 1.1660 | GBP/USD: 1.3922

- Bank transfer rates: 1.1430 | 1.3630

- Specialist transfer rates: 1.1580 | 1.3825

- Get a bank-beating exchange rate quote, here

- Set an exchange rate alert, here

The British Pound was sold after an optimistic Bank of England didn't quite meet the lofty expectations build up by investors ahead of its June policy meeting.

The Bank showed it was in no rush to raise interest rates with the statement issued following the meeting revealing policy setters view the current rise in inflation as being temporary, a potentially disappointing outcome for those in the currency market looking for more urgency.

"The Bank of England's latest statement is a little more upbeat than might have been expected, but crucially offers no new clues on rate hike timing," says James Smith, Developed Markets Economist at ING.

All members of the Bank's Monetary Policy Committee (MPC) opted to keep interest rates unchanged but one member - Andy Haldane - voted to reduce the scale of quantitative easing by £50BN.

That no other members joined Haldane suggests the MPC is in no mood to bring forward expectations for tightening, which might have been a source of disappointment for those positioned for a rise in the Pound.

"First read off BoE looks fairly dovish. No other MPC members joined Haldane in calling for early exit. MPC see inflation is transitory and suggests no rush to tighten. Opposite to the Fed in tone here. Looks like not enough for GBP bulls and could see stretched longs bail," says Viraj Patel, Global Macro Strategist at Vanda Research.

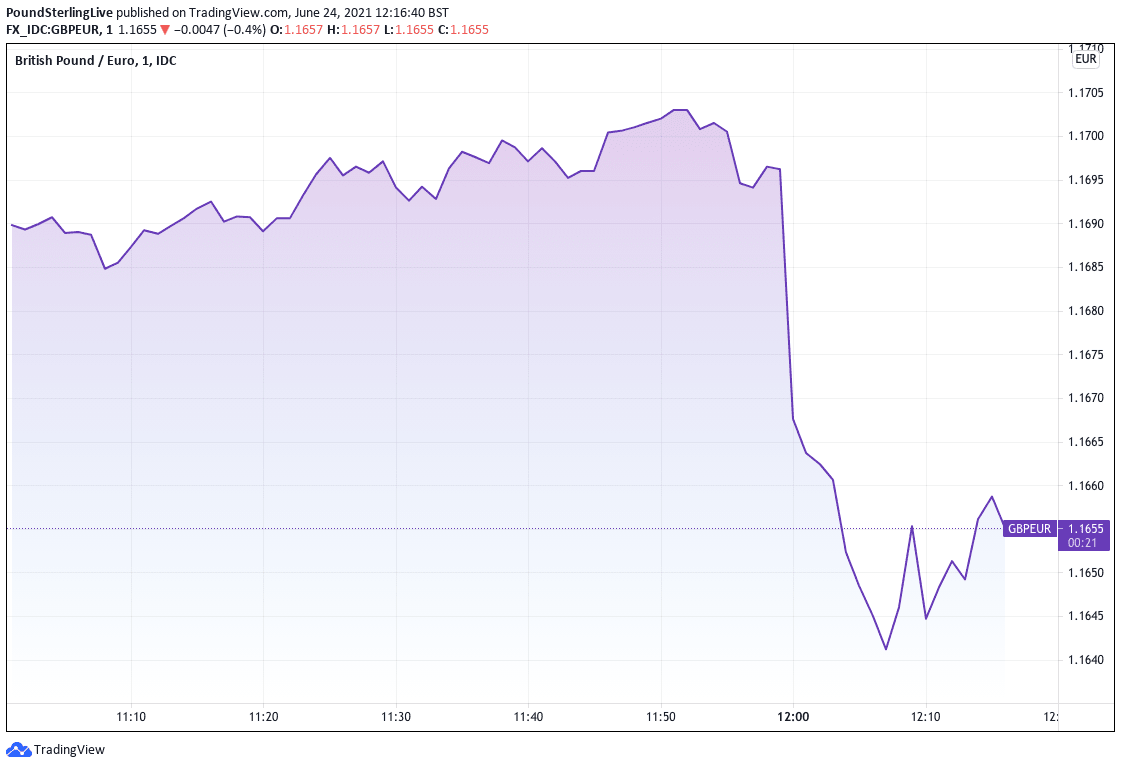

The Pound-to-Euro exchange rate fell half a percent to trade at 1.1658, the Pound-to-Dollar exchange rate fell a third of a percent to trade at 1.3926.

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

"On the whole, today’s policy statement suggests that the Bank of England has an incrementally more dovish reaction function than what was witnessed prior. This has weighed on sterling and gilts this afternoon, with GBPUSD now trading closer to the 1.39 handle than the 1.40 level it was testing yesterday," says Simon Harvey, Senior FX Market Analyst at Monex Europe.

The Bank maintained its basic interest rate at 0.1% and kept quantitative easing levels unchanged.

Economists at the Bank revised up their expectations for the level of UK GDP in 2021 Q2 by around 1.5% since the May Report, as restrictions on economic activity have eased, so that output in June is expected to be around 2.5% below its pre-Covid 2019 Q4 level.

But despite any optimism on the outlook the MPC appear in no mood to raise interest rates.

The Bank mentioned that they view the delay to the final lifting of all covid restrictions, which were originally planned for June 21, as being of little consequence to the economic outlook.

Regarding inflation, the MPC expect the direct impact of rises in commodity prices on CPI inflation will be transitory.

The MPC’s central expectation is that the economy will experience a temporary period of strong GDP growth and above-target CPI inflation, after which growth and inflation will fall back.

The MPC says they see two-sided risks around this central path, and it is possible that near-term upward pressure on prices could prove somewhat larger than expected.

But, taking together the evidence from financial market measures and surveys of households, businesses and professional forecasters, the MPC says it judges that UK inflation expectations remain well anchored.

On balance there is very little by way of surprise in the statement and it marries up with analyst expectations ahead of the event.

Therefore the reaction in Pound Sterling looks to be somewhat overdone and there is the potential for the currency to regain the knee-jerk losses over the near-term.

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

The foreign exchange market reaction does perhaps suggest that the market was potentially getting overly excited about what rising inflation and strong economic readings meant for the future of policy at the Bank.

"It seems that a somewhat more hawkish stance was expected beforehand, or that markets expected that more members had voted in line with Haldane," says economist Knut A. Magnussen at DNB Bank ASA.

The fall in the Pound following what looks to be a relatively unexpected event would hint that the Pound had been bid higher in anticipation of a potentially more 'hawkish' shift at the Bank.

"Other than the MPC noting the growing upside risks to inflation at today’s policy meeting, there were no real signs that it is thinking about tightening policy sooner, à la the Fed," says Paul Dales, Chief UK Economist at Capital Economics.

Capital Economics expect the Bank to raise interest rates much later than the mid-2022 date the markets have assumed. Market expectations currently imply one rate hike will be delivered in the second half of 2022 and another one in the second half 2023.

"The key point is that the MPC still appears willing to ride out the inevitable rise in inflation over the next six months as it thinks it will be short-lived," says Dales.

Capital Economics says the MPC can run the economy hotter for longer (i.e. provide easy money to boost growth) without generating a sustained rise in inflation.

"As such, we think the MPC may not tighten policy until well after the mid-2022 date assumed by the markets, perhaps even as later as 2024. And at that point, we think it will tighten by unwinding some QE before raising interest rates. So interest rate hikes may still be a couple of years away," says Dales.

ING's Smith says assuming the near-term Covid-19 concerns fade towards the end of the summer, following widespread double vaccination, then the debate over rate hike timing is likely to gain more momentum. ING expect the first interest rate rise to come in 2023, "at the earliest".