German Bund 'Tantrum' Behind the Latest Euro Exchange Rate Rally, 1.1619 next focus

A fall in the value of German Bunds has widely been cited as the key driver behind the latest bout of Euro strength.

Where next for Bunds then?

The release of the European Central Bank’s (ECB’s) June meeting minutes has sparked a knee-jerk reaction fall in European bonds, and a simultaneous rise in the Euro.

The minutes revealed for the first time that ECB officials discussed removing from their statement the phrase that they would ‘step-up the pace of bond buying should the economy need more stimulation’.

The revelation that they discussed deleting the phrase about increasing bond purchases was taken as further evidence of a more confident, hawkish stance.

“The minutes show that the ECB was considering to even go beyond the June changes,” said Carsten Brzeski, an analyst at ING. “Today’s minutes come at a time at which speculation about a possible fast and imminent end of the ECB’s ultra-loose monetary policies have started again,” added the analyst, quoted in the FT by Patrick McGee.

For the ECB to have discussed amending their statement is proof that they see Eurozone growth on a more sustainable footing.

Taken together with Mario Draghi’s comments at Sintra, that the threat of deflation had receded, the inference is of an incremental move towards removing the crutch of stimulus.

The ECB’s current pace of bond purchases equals 60 billion euro’s worth per month and this accounts for a substantial share of the overall market.

This explains why Bunds sold off so heavily after the release of the minutes, because the ECB is the market’s biggest buyer.

A fall in European Bonds is generally a sign that the Euro will rise.

Falling bond prices are generally a reflection of higher inflation expectations and consequently higher interest rates, and currencies tend to rise on the back of higher interest rates as they attract more capital inflows from investors seeking higher returns.

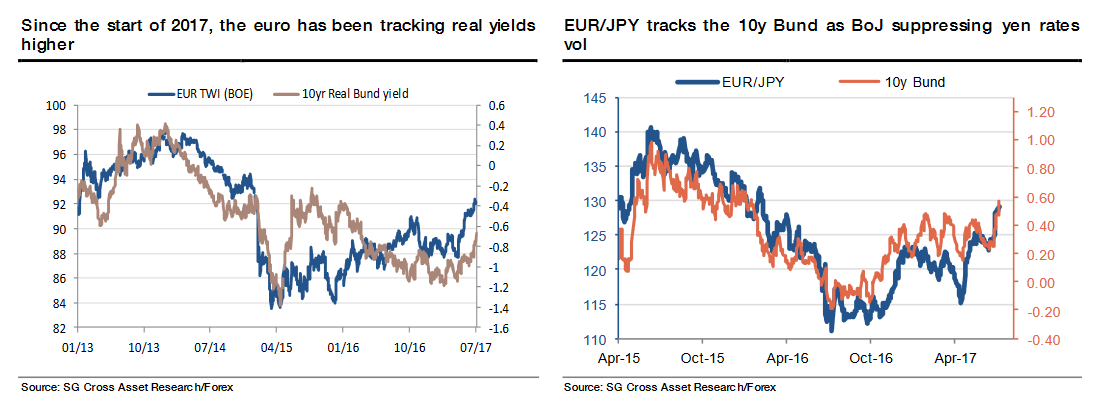

Bond yields – particularly real yields which are inflation adjusted - are a proxy for inflation and interest rate expectations as they rise in tandem with them, therefore analysts often use them as a guide to forecasting currencies.

“The yield on 10-year inflation-adjusted Bunds has risen by 25bp in a couple of weeks and is now 50bp higher than at the start of the year. The euro has gained 9% against the dollar in the process,” said Société Générale’s Kit Juckes.

“As the ECB talks about talking about tapering its bond purchases, we are likely to see Bund yields rise further, and the euro will go on feeling the gravitational pull of fair value (EUR/USD 1.25 is a reasonable guess), adding to ECB President Draghi’s headaches,” he added.

Société Générale see EUR/USD breaking above 1.1460 and then moving up to the May highs at 1.1619.

Other analysts, such as TD Securities Richard Kelly, suggest a break above 1.1619 would change the whole outlook for the chart and signal the beginning of a much more bullish era for the pair.

Juckes, however, is more cautious, seeing such a break as likely to extend to 1.1685 and then perhaps 1.1714.

Significant resistance at 1.1616-1.1714

In a recent technical comment on the pair, KBC Sunrise’s Piet Lammens echoes TD's focus on 1.1619 as the main cieling to breach (after 1.1500).

In the long-term “correction tops are coming in at 1.1616/1.1714,” and a break above them would be important, ending a long consolidation period, “that followed the sharp decline of EUR/USD in 2014/early 2015,” said KBC's Piet Lammens.

However, a break above such a key area would be difficult for now. On the downside 1.1119 is the next important support level and obstacle to further weakness.

Option Strategy for EUR/JPY

Based on their outlook for greater upside in the Euro, Société Générale (Soc Gen) have issued a call to buy EUR/JPY options in expectation of a rise in the exchange rate.

They see the volatility in Eurozone bonds as juxtaposed to the opposite in Japanese bonds which the Bank of Japan are controlling.

SocGen are advocating buying EUR/JPY 6-month call options with a strike price of 135, which means they will only start to make money if the exchange rate moves above 135 in the next 6-months.

They are using a put option on the same instrument as a potential hedge for the option premium costs, should the market move down instead. The put will start to profit if the exchange rate moves below 122.50.