Haldane: Bank of England Approaching a "Dangerous Moment", sees 4.0% Inflation in 2021

- Written by: Gary Howes

- `Haldane warns of slow exit from quantitative easing

- "inflation to rise, significantly and persistently"

- "this is for me an uncomfortable spot"

- "most dangerous moment inflation-targeting has so far faced"

Above: Andy Haldane. File image © Bank of England.

Chief Economist of the Bank of England Andy Haldane has warned the UK economy is starting to overheat and unless quantitative easing is withdrawn soon uncomfortably high levels of inflation will become embedded.

Delivering a farewell speech at the end of his 32 years on Threadneedle Street, Halande said UK inflation was on course to reach 4.0% and bust the current forecasts held by the Bank for inflation to peak at around 3.0%.

Such an outcome would be to the detriment of the Bank's multi-year attempt to keep inflation anchored around 2.0%, a task he says the Bank has been incredibly successful at achieving since it started targeting inflation levels in 1992.

Should inflation expectations being de-anchored from current low levels, higher inflation then becomes increasingly difficult for policy makers to target and there is a risk that the response in turn triggers ugly side effects.

Haldane says the UK economy is now already seeing price surges across a widening array of goods, services and asset markets.

"At present, this is showing itself as pockets of excess demand. But as aggregate excess demand emerges in the second half of the year, I would expect inflation to rise, significantly and persistently," he says.

Driving inflation higher is a rapidly expanding economy, recovering from the unprecedented slump of 2020 when it was shutdown to protect the country's citizens from Covid-19.

Haldane says much of the expansion is natural as businesses refind their feet and consumers opening their wallets to spend the excess savings they have accumulated when locked in their homes.

"The private source of economic energy comes courtesy of the large pool of involuntary savings amassed as a result of restrictions on spending. For UK households these amount to over £200 billion and for UK companies around £100 billion. Leakages from this saving lake are already fuelling spending on goods and assets," says Haldane.

The speech is made on the same day the ONS releases data showing the amount saved in the January lockdown was higher than previously expected.

But, the extraordinary monetary stimulus provided by the Bank and the extraordinary fiscal stimulus provided by the government are fuelling the natural recovery.

According to the economist, the Bank will hold close to £1 trillion of nominal Government assets, around half of their total and 40% of GDP.

"Truth be told, this is for me an uncomfortable spot," says Haldane.

He cites two reasons for this discomfort:

1) A concern as to whether continuing monetary stimulus is consistent with central banks hitting their inflation targets on a sustainable basis.

2) A concern as to whether the monetary policy strategies being pursued by central banks are at risk of time-inconsistency, fiscal dominance and an erosion of central bank independence.

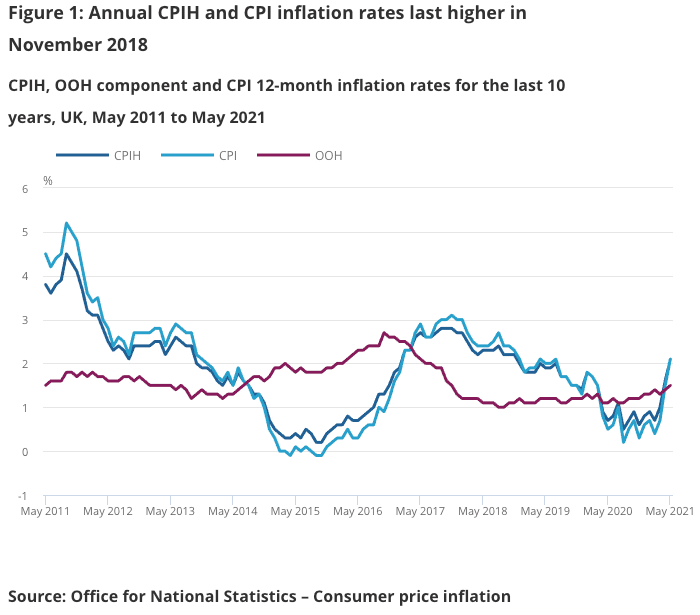

Above: The Bank's most recent forecasts for inflation show 4.0% inflation would pose a significant surprise.

Haldane has been a lone voice on the Bank's Monetary Policy Committee (MPC) calling for the shrinking of the quantitative easing programme.

He was the only member of the MPC to vote for lower levels of easing at the June policy meeting and his departure risks the Bank falling hostage to a group-think that is only too happy to continue providing generous amounts of easy money to keep the economy growing.

The thinking at the Bank is that the current levels of inflation will be temporary and soon subside once the economy has recovered the ground it lost during the crisis.

But, Haldane says: "with public and private financial fuel being injected into a macro-economic engine already running hot, the result could well be macro-economic overheating."

The heating economy, fuelled by stimulus from the Bank and Government, could deliver surprisingly strong levels of inflation he says.

"When resurgent, and probably persistent, demand bumps up against slowly-emerging, and possibly static, supply, the laws of economic gravity mean the prices of goods, services and assets tend to rise, at first in a localised and seemingly temporary fashion, but increasingly in a generalised and persistent fashion," says Haldane.

Haldane says demand will likely be supported by lower-than-expected unemployment levels which he says is encouraging more of those savings created during lockdowns to be spent in a virtuous cycle.

"The size and depth of this saving lake means it could finance demand at scale for some period to come," he says.

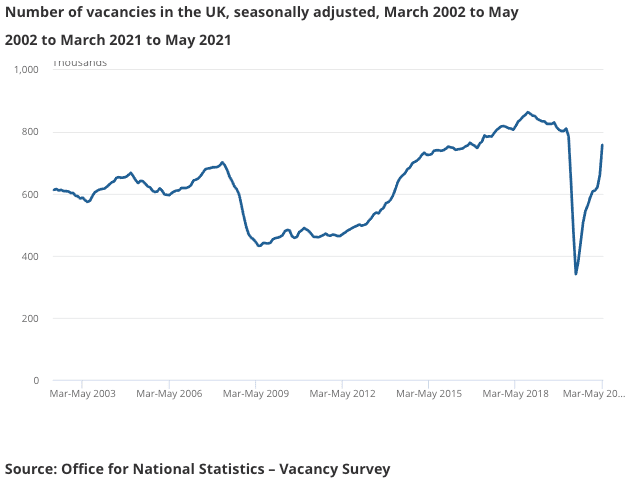

Above: Rising vacancies point to a more robust labour market than had been expected at the start of the year.

Haldane says we are now witnessing inflation becoming increasingly persistent with price surges across a widening array of goods, services and asset markets.

"At present, this is showing itself as pockets of excess demand. But as aggregate excess demand emerges in the second half of the year, I would expect inflation to rise, significantly and persistently," he says.

In his opinion inflation is likely to reach 4.0% by the end of 2021, well ahead of the Bank's current expectations for the peak to reside near 3.0%.

Andrew Sentence, a former MPC member and a critic of the Bank's ongoing 'easy' monetary policy, responded to Haldane's speech by saying 5.0% inflation is more likely in his view if the cut in VAT to the hospitality sector is reversed later this year.

Such a shock would in turn likely only encourage further inflation as expectations for higher inflation levels becomes ingrained.

"This increases the chances of a high inflation narrative becoming the dominant one, a central expectation rather than a risk. If that happened, inflation expectations at all maturities would shift upwards, not only in financial markets but among households and businesses too," says Haldane.

The economist warns that the UK could be on course to suffer a 'Minsky Moment' for monetary policy as a result.

(Hyman Minsky was an economist at Washington University in St. Louis from 1965 to 1990. He proposed a theory he labeled the financial instability hypothesis, which holds that the economy creates its own bubbles and crashes. The gist of his theory is that stable economies sow the seeds of their own destruction because stability, seeming safe, encourages people to take risks. Source.)

Such a moment "would leave monetary policy needing to play catch-up to re-anchor inflation expectations through materially larger and/or faster interest rate rises than are currently expected," says Haldane.

The destabilising effect of such a reaction would have far-reaching consequences as Haldane says a dependency culture around cheap money has emerged over the past decade.

"Only a minority of those with mortgages have ever experienced a rise in borrowing costs. Fewer still have significant inflation in their lived experience".

He says the Bank would therefore better achieve its ends of targeting stable inflation by acting sooner rather than later.

"More fundamentally, a slow exit risks putting central bank balance sheets on an unsustainable footing," says Haldane. "This is the most dangerous moment inflation-targeting has so far faced."

He says it is critical that the Bank maintains and pursues its inflation targeting mandate and that the time has come for "immediate thought, and action, on unwinding the QE currently being provided, given the state of the economy and central banks’ balance sheets."

"Easy money is always an easier decision than tight money. But an asymmetric monetary policy reaction function is a recipe for a Minsky Mistake," says Haldane.