Image © Pound Sterling Live

- GBP/ZAR to find support soon and rebound

- More upside expected in line with longer-term trend

- Rand to be driven by global risk trends and USD

The Pound-to-Rand exchange rate is trading at around 19.120 at the start of the week after declining 1.67% during the week so far. The Rand went higher at the start of the new week as investors expressed relief over a Moody's decision to leave South Africa's 'investment grade' credit rating unchanged in November.

Moody's changed its outlook on South Africa's investment grade rating to negative but left the rating itself in place, sparing the country from the exodus of foreign capital that would come with a downgrade to 'junk' status.

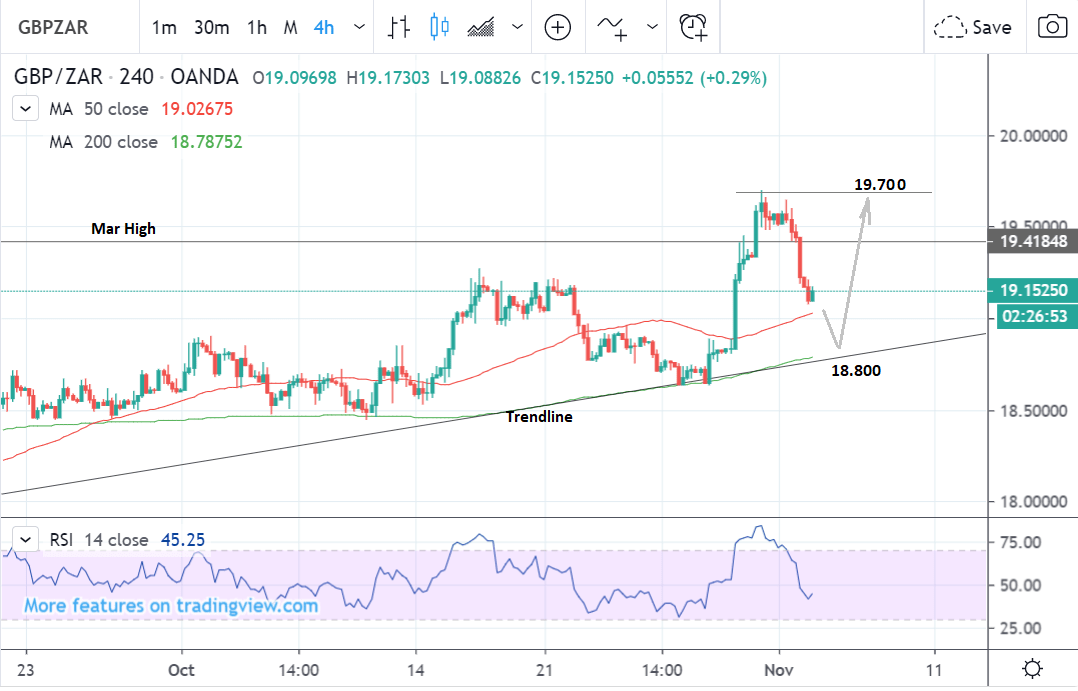

The gains forced the GBP/ZAR exchange rate to 'gap' lower when markets opened Monday, and our studies of the 4hr chart - used to determine the short-term outlook which includes the coming week - shows the pair falling steeply towards an important trendline.

The sell-off looks set to continue down to a target at 18.800 and the trendline where the price will probably find support and pause.

Ever since late July, the trend has been up. This has been evidenced by the sequence of rising peaks and troughs, which is expected to continue once the current sell-off has run its course - probably at the level of the trendline.

From there the exchange rate is likely to recover and start moving back up, potentially reaching the October 31 highs at 19.700 over the near-term.

The daily chart shows the same forecast scenario as the 4hr chart with an extension to a new high.

The pair is likely to fall to the trendline, find support and rebound back up to the old highs, however, a break above those October highs would also confirm a continuation up to the next target at 20.000, which is a major psychological level for the pair.

Traders are more likely to offload bullish bets at this level and so a certain amount of uncertainty and volatility is expected to be associated with it.

The daily chart is used to give us an indication of the outlook for the medium-term, defined as the next week to a month ahead.

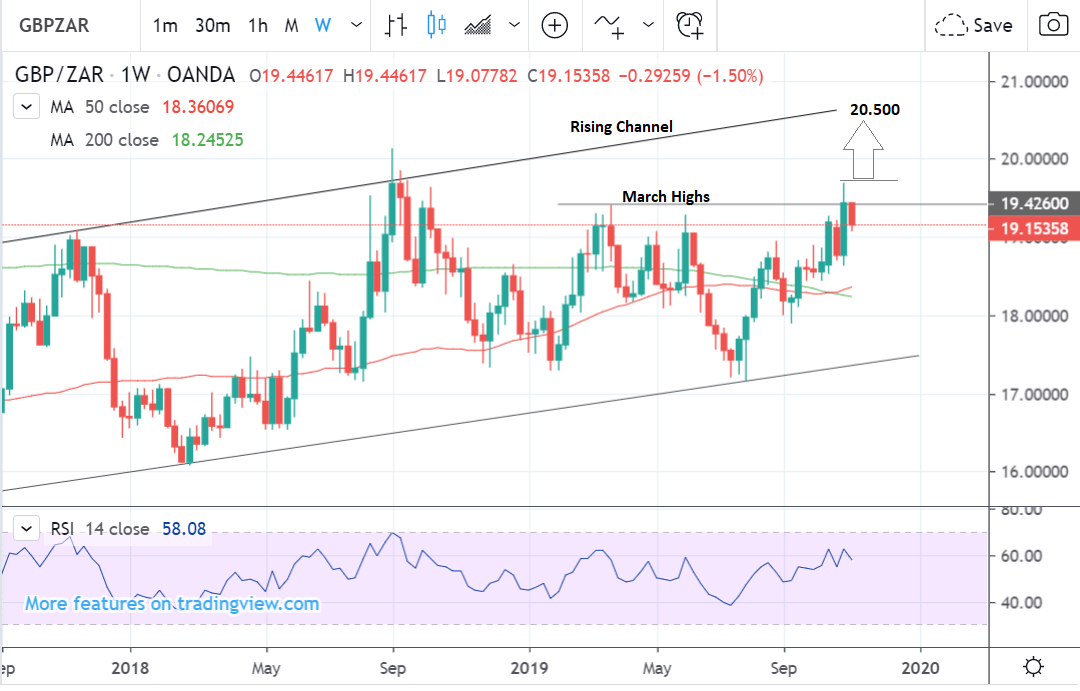

The weekly chart shows how the has successfully broken above the March highs suggesting the possibility of more upside in the future.

A break back above the 19.700 would indicate further bullish activity, potentially up to a target at 20.500 at the top of the longer-term rising channel, which is itself a bullish factor in the chart’s interpretation.

The weekly chart is used to give us an indication of the outlook for the long-term, defined as the next few months.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of a specialist foreign exchange specialist. A payments provider can deliver you an exchange rate closer to the real market rate than your bank would, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

What to Watch this Week

The main drivers of the rand in the near-term will be global risk trends, fluctuations of the U.S. Dollar, and the South African economy-wide PMI, out on Tuesday.

Global markets are still optimistic that the U.S. and China can reach a trade deal and this is reflected in the positive performance of riskier assets and emerging market currencies such as the Rand.

The Phase 1 trade deal still looks set to result in a de-escalation of the trade war, with a signing of the new trade deal scheduled for mid-November.

News out on Sunday suggests that the U.S. is already allowing certain U.S. companies to conduct trade with China’s Huawei again after previously implementing a ban.

U.S. Commerce Secretary Wilbur Ross said, on Sunday, that licenses for American companies to export certain technology products to China’s Huawei “will be forthcoming very shortly”, which is a considerable breakthrough and shows concrete progress.

Positive manufacturing data for small and medium-sized companies in China showed a strong rebound in October which also helped risk appetite.

“The Caixin China manufacturing PMI was also stronger than expected, reaching its highest level since the start of 2017, in a sign that Chinese growth may have bottomed,” says Nick Smyth of BNZ Bank.

If there is a risk from a global perspective it is that the U.S - China trade deal remains limited and does not lead to a bigger more comprehensive deal down the line as was previously promised by Donald Trump.

Chinese officials remain sceptical about the possibility of a more comprehensive deal mainly because they would demand, as a prerequisite, for the U.S. to lift all punitive tariffs on China, essentially undoing all the tariffs implemented under President’s Trump ‘America First’ campaign - a demand which is highly unlikely to be met under this administration.

Another key driver of the Rand is the U.S. Dollar to which it is negatively correlated.

The main driver of the U.S. Dollar this week is the ISM non-manufacturing PMI survey out on Tuesday.

The ISM will provide an insight into the performance of a part of the economy which has remained relatively insulated from the global slowdown in heavy industry.

Analysts will be watching it for signs of contagion, which might signal an impending recession, so substantial weakness in the data is likely to impact negatively on the Dollar - positively on the Rand.

The ISM non-manufacturing PMI is out on Tuesday at 15.00 GST. Current market expectations are for a rise to 53.4 from 52.6. The employment sub-index is also likely to garner a lot of attention due to woeful underperformance in recent months.

In summary, a higher-than-expected reading in either the main or employment sub-index should be taken as positive or bullish for the U.S. Dollar (negative or bearish for the Rand), while a lower than expected reading should be taken as negative or bearish for the Dollar (bullish for the Rand).

The main data release in the near-term is the SA economy-wide PMI, out on Tuesday morning at 9.15 local (SA) time.

“Consensus expectations are for the index to have slipped marginally in October to 49.0 pts from 49.2 pts in September,” says Shireen Darmalingam, an economist at Standard Bank.

Given the recent outlook downgrade by Moody’s to negative, there may be more of a focus on key data as analysts try to determine whether Moody’s will follow up with a full credit rating downgrade in 2020 as some analysts fear.

“The economy-wide PMI has stayed in contraction territory (below the neutral level of 50) since March 2019. The ABSA PMI, which covers the manufacturing sector only, remained in contraction territory in October. Despite this, we cannot make firm inferences on the economy-wide PMI based on the ABSA PMI levels or movements, as the two PMIs have a poor correlation coefficient of 40%, but this might change following the recent re-weighting of the ABSA PMI,” says Peter Worthington, an economist at ABSA.

* Advertisement