- JPY an underperformer this week and in August amid risk rally.

- PM Abe to host 09:00 press conf Friday and address speculation.

- After hospital visits stoke concern about health and tenure as PM.

- Abenomics seen enduring on virus, domestic economy challenges.

Image © Chairman of the Joint Chiefs of Staff, accessed Flickr, reproduced under CC licensing.

- GBP/JPY spot rate at time of writing: 140.04

- Bank transfer rate (indicative guide): 135.14-136.12

- FX specialist providers (indicative guide): 137.94-138.78

- More information on FX specialist rates here

The Yen continued its run of underperformance Thursday amid ongoing speculation suggesting Prime Minister Shinzo Abe could be on the verge of standing down, although analysts say a resignation would likely have little bearing on the outlook for the Japanese currency.

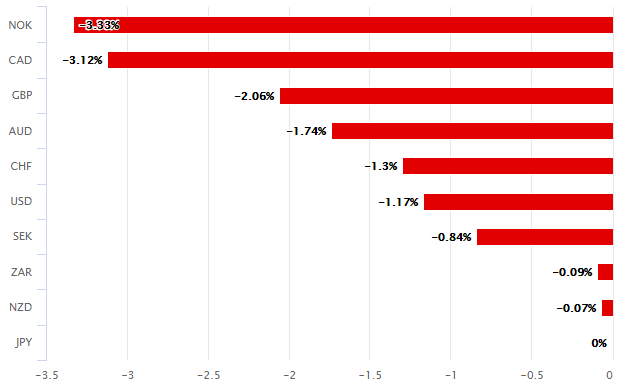

Japan's Yen underperformed most major counterparts and remained firmly at the bottom of the bucket for the week as well as month of August after the safe-haven unit lost ground to riskier rivals amid an upbeat mood among investors, which has lifted global stock markets and bond yields.

This nascent underperformance could be at risk of reversal at least temporarily if local press reports are right that Japanese Prime Minister Shinzo Abe may resign or otherwise set out a succession plan at an eagerly awaited press conference Friday. The conference is reportedly planned for 09:00 London time.

"The visit to a hospital on Monday for a second time has helped fuel uncertainty over his health, so much so that Kyodo News reported that PM Abe intends to hold a press conference on Friday," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG, Japan's pre-eminent lender and the world's fifth largest bank. "Given it is his policies that coined the phrase “Abenomics” that involve the three arrows of Monetary policy easing; fiscal expansion; and reforms to boost economic growth – any doubts about his tenure could have implications for the yen."

Above: Japanese Yen performance against major counterparts in August. Source: Pound Sterling Live.

Prime Minister Abe and his economic policies were instrumental in bringing about the 2013 devaluation of the Yen which saw USD/JPY rise from 86 in January to 105 by year-end, a level it was also trading near to on Thursday, so a resignation at a still-unconfirmed press conference on Friday would be a landmark moment for the currency.

But for an impact to be meaningful and sustained, a change of leadership would need to be accompanied by a change of monetary and fiscal policies. Some say this is unlikley given any changeover would take place amid the coronavirus pandemic and with the economy still dogged by familiar problems.

"Whoever is in charge of Japan’s economy would have little option other than to pursue the current mix of loose monetary and fiscal policy," says Daragh Maher, head of U.S. FX strategy at HSBC. "JPY, however, is more tied to global risk appetite than local economic and political developments. USD-JPY may be range bound as both currencies are safe havens, but JPY crosses such as AUD-JPY are close to recent highs."

Devaluation and the lingering weakness in the Yen resulted from the Prime Minister's so-called Abenomics programme, which amalgamated structural and fiscal reforms with fiscal and monetary policy stimulus.

Above: USD/JPY rate shown a monthly intervals as Dollar Index (black line, left axis) highlights USD trend.

Abenomics was designed to put the public finances on a more sustainable footing while boosting the economy. It was hoped the much-vaunted strategy would end the deflationary stagnation that has haunted Japan since the boom-to-bust decades of the 1970s and 1980s.

"The recent development comes at a time when PM Abe's "personal popularity" is starting to wane," says Izumi Devalier, a Japan economist at BofA Global Research. "No matter who ends up being PM Abe's successor, we think there is unlikely to be much of a difference in basic macro policy in the nearterm and that fears of a policy reversal are overdone. In the short run, the number one priority of the new prime minister will be to (1) consolidate power and (2) deliver a strong result in the general elections."

Abenomics combined 'three arrows' of policy and is a term that was coined to much fanfare in 2013 before the appointment of current Bank of Japan (BoJ) Governor Haruhiko Kuroda and several subsequent, large expansions of the monetary supply through quantitative easing.

The BoJ launched a ¥270 trillion (£1.9 trillion) programme of bond buying financed by newly created money, which was intended to facilitate faster growth by reducing borrowing costs for government, companies and households.

BoJ easing was combined with higher consumption (VAT) taxes and investment in infrastructure and other areas, with the process since repeated several times.

Above: GBP/JPY rate shown a monthly intervals. Little Yen depreciation relative to Pound Sterling.

"Abe's successor is unlikely to risk any kind of negative policy shock that could end up hurting markets and Japan's already-weak economy," Devalier says. "Given the most impactful part of Abenomics has been aggressive BoJ easing, Abe's departure naturally raises the question of whether Governor Kuroda will also leave his post before serving out his current term, which runs till April 2023. While an early Abe departure would raise such risks at the margin, we think this is highly unlikely in the short run (before 2022)."

Abenomics has achieved some success in a range of areas but otherwise fallen short of the ultimate goal to lift Japan out of a stagflationary mire.

Debt-to-GDP growth has slowed and enough for the earlier upward trajectory to have flattened when represented graphically. In addition, and after a short-lived 2013-to-2014 increase above 3%, inflation and core inflation have returned to lower levels but remained consistently above zero.

GDP growth however, has remained largely stagnant and Japan continues to face the same demographic challenges that have its working age population, and tax base, shrinking in the coming decades and to a size that could be increasingly unsustainable given the elevated level of debt-to-GDP. At 236.6% of GDP in 2019, the Japanese debt pile remains the largest in the world.

"If Abe does unexpectedly step down and we are in office to see it (only expectoration of time is Tokyo afternoon) we would be participating in the move," says the J.P. Morgan London dealing desk. "If you wake up to see USDJPY over 100 pips lower on that outcome I would be cautious about piling in – any relief rally on Abe throwing cold water could be an opportunity to add to shorts."