Image © Adobe Stock

- GBP/USD remains in a short-term uptrend

- Break of previous week's highs will provide green-light for bulls

- Brexit and inflation data dominate Sterling's calendar

The Pound-to-US Dollar exchange rate crossed the 1.30 Rubicon last week when it rose from an open price of 1.2927 to a close, on Friday, of 1.3066 after Brexit risks subsided on the back of hopes of a deal being brokered.

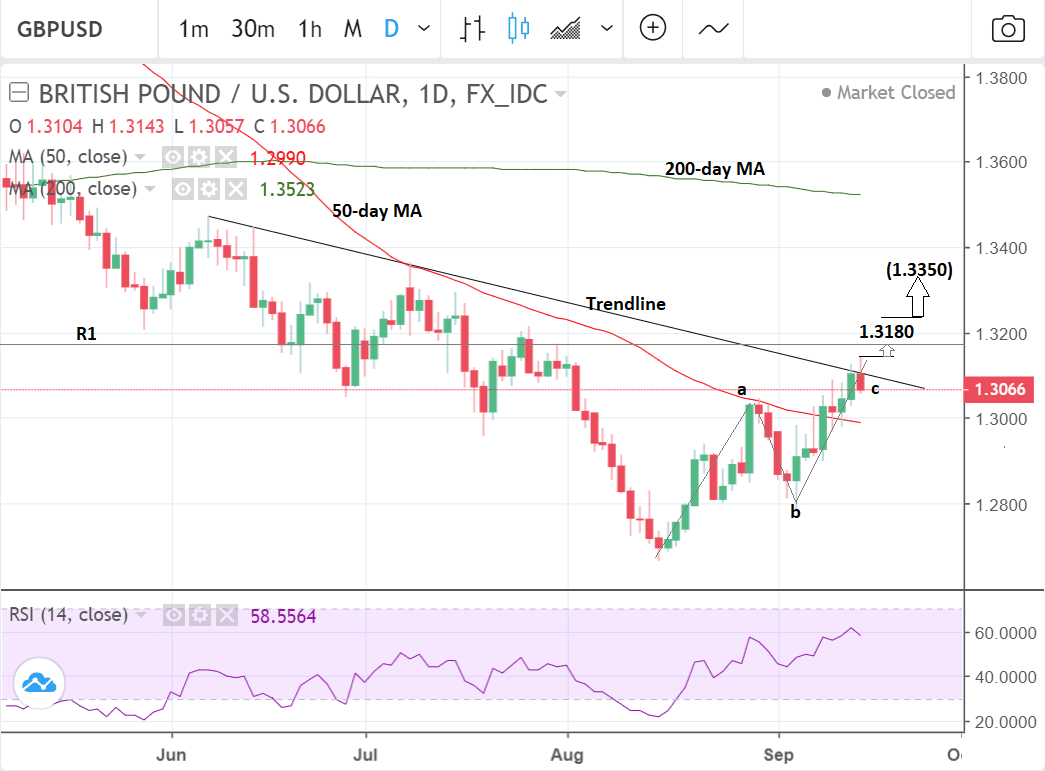

From a technical standpoint there are really two interpretations that can be drawn from the GBP/USD chart as it stands: one is straight-forwardly bullish and the other is bearish.

The bullish interpretation is based on the fact the pair is now probably in a short-term uptrend which is biased to go higher based on the principle that the trend is more likely to extend than reverse.

Image © Pound Sterling Live, TradingView

Although the pair has reached a key trendline drawn from the June highs and has failed to break through it - withdrawing instead to just below it - the exchange rate is still more likely to eventually pierce through it than reverse.

A re-break above the 1.3134 highs would provide the necessary confirmation for such a move, with the next target at 1.3190, at the level of the R1 monthly pivot, a level - as its names suggests - where traders expect the price to rotate and pull-back and which thus attracts a lot of technical traders fading the trend.

Nevertheless, if there is a move up to 1.3190 we would expect it to probably extend even higher on the back of the bullish euphoria following the trendline break, and a further move above 1.3210 would, we would estimate, probably confirm such an extension to the next target at 1.3350, at the same level as the July highs.

The alternative interpretation is that the pair has just finished forming a classic three-wave abc correction, which is a fairly common pattern in markets suggesting a corrective rather than impulsive move is afoot.

If this interpretation is correct, it would indicate that not far off lies the possibility of a resumption of the downtrend. This would also fit well with the recent price-stall at the trendline which would posit a natural barrier against further evolution and probably signal the place for bears to jump back in and push the exchange rate lower again.

Overall we do not see sufficient evidence to support the second, bearish, interpretation over the first, and so the bullish view remains our preferred interpretation of the two.

Advertisement

Lock in your Dollars: Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Dollar: What to Watch

Ongoing trade-tensions could very well set the tone for the way the Dollar trades in the week ahead given data is unlikely to be significant enough to lead to major volatility.

The possibility of $200bn extra tariffs on Chinese imports to the US remains a 'sword of Damocles' hanging over markets.

Currently Beijing and Washington are still in talks but if they break down the US could announce the feared expansion of duties. The effect is likely to be positive for the US Dollar in line with previous trends as investors turn to US assets for safety.

There is also a possibility the US Dollar could suffer from political uncertainty after Trump's former campaign chairman Paul Manafort turned state's witness on Friday and agreed to help special council Robert Mueller with his investigation into links with Russia in return for a reduced sentence.

One former US attorney said this posed an "existential threat to the President."

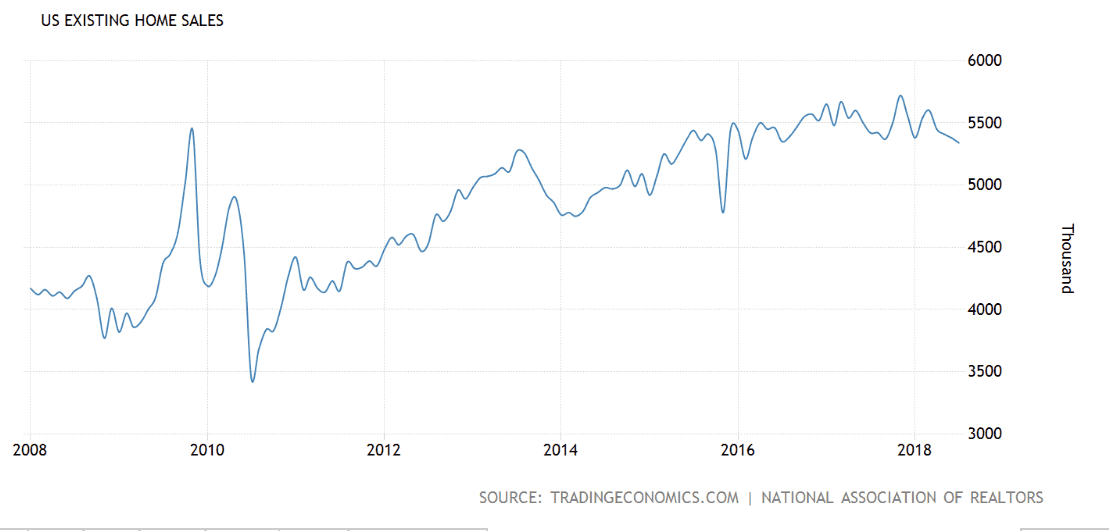

As far as hard data goes, however, the main releases for the Dollar in the week ahead is housing related data, Fed regional activity gauges and September PMI's on Friday.

Housing data are out - both new and existing sales - and have shown marginal declines over recent months but are still not at levels deemed concerning.

The main gauge to watch is probably existing sales as these are showing some stress linked to the economy. The gauge fell by - 0.7% in July in the fourth decline in a row and the lowest level since February of 2016.

The median house price fell to $269,600 from $273,800 in June.

As the chart below shows sales are starting to break their smooth uptrend and need to be watched. That 'housing leads the economy' is an old economic adage which certainly held true in the last crisis, so this release warrants attention.

"Existing home sales remain stuck in low gear, and affordability is an increasing concern. Mortgage rates have ticked higher the past year, and continued low levels of inventory on the market have translated to home prices rising well ahead of income growth. Still, signs continue to point to economic growth remaining solid headed into the fall, which should allow existing home sales to pick up from their current pace," says a note from investment bank Wells Fargo.

Existing Home sales are scheduled for release on Thursday, September 20 at 15.00.

The leading Index is another useful gauge as it is an alloy of several economic metrics. It is expected to show a 0.5% rise compared to 0.6% previously, when it is released at the same time as Existing home sales on Thursday.

"The Leading Economic Index (LEI) increased 0.6% in the July, further evidence that economic growth should remain solid in the second half of 2018," says Wells Fargo. "The monthly gain follows a 0.5% rise in June and has now climbed 5.5% on a six-month annualised basis. July’s improvement was also comprehensive, as each of the underlying components contributed to the 0.7 point increase in the headline index."

"The largest contributor was initial jobless claims, which added 0.15 points. Meanwhile, manufacturing hours worked had the smallest impact and remained neutral to the overall index," add the bank.

The NY Empire State Manufacturing Index is out on Monday and is forecast to show a slide to 23.0 from 25.6 in September when it is released at 13.30.

It is followed by the Philadelphia Fed Manufacturing Index in September on Thursday at 13.30 which is forecast to show a rise to 16.9 from 11.5.

Finally, Friday sees the other main release for the Eurozone in the form of initial estimates for Manufacturing and Services PMIs in September, at 14.45.

PMI's measure activity and Manufacturing activity in the US is expected to show a slight rise to 55.0 from 54.7, whilst services is forecast to increase to 55.0 from 54.8.

A result over 50 is indicative of expansion and of under 50 of contraction. PMI's are surveys of purchasing managers conducted by data provider Markit IHS.

A higher-than-expected result is likely to support the Dollar and vice versa for a lower-than-expected result.

The Pound: What to Watch this Week

Sterling has made a decisive recovery in September as the terms of reference of the Brexit debate have undergone a dramatic change.

Whereas previously they were somewhat polarised into the Chequers proposal on the one hand and a 'no-deal' pure Brexit on the other the gap now appears to have closed.

Now even 'die hard' Brexit purists appear to be advocating a deal based on the EU's deal with Canada - known as a 'Canada plus' deal - whilst Chequers, and even continued membership of EEA is being considered as the soft option avoiding the most economic disruption.

We heard from analysts at Nordea Markets in the week past that the Pound should actually rise under all Brexit scenarios, but expect a bloodbath if a 'no deal' arises.

The bottom line for the Pound is should the probability of a 'no-deal' continue to diminish the currency should see more gains.

"Brexit talks between the UK and the EU are expected to be stepped up in the coming days with the topic likely to dominate the informal summit of EU leaders in Austria on September 20. Sterling should therefore continue to see high volatility as it remains sensitive to Brexit headlines," says a note from forex broker XM.com.

On the hard data front, meanwhile, there are also some notable releases in the week ahead including inflation figures for August and retail sales.

Headline inflation is forecast to dip back to 2.4% in August (from 2.5%) on a year-ago comparison basis, while the core rate is predicted to fall to 1.8% from 1.9% previously (year-on-year).

Analysts are overall a bit downbeat about the prospects of economic data in the week ahead so surprises to the upside would be likely to drive the Pound higher, whilst those to the downside might weigh but to a certain extent will already be accounted for.

"Next week’s indicators may not be as positive and could fail to provide support for the pound in case the Brexit negotiations were to break down," says XM.com, "CPI figures will be watched on Wednesday for evidence that inflationary pressures in the UK continue to edge lower towards the Bank of England’s 2% target."

The other hard data release is retail sales on Thursday which is forecast to show a 0.2% month-on-month contraction in sales in August after a 0.7% bounce in July.

The overall assessment for UK data is that it remains 'sluggish' and more at risk of decline than growth.

Regardless of data no-one expects the Bank of England (BOE) to raise rates until Brexit is clarified.

Since interest rates are the main driver of foreign exchange - pushing the Pound up if they are hiked - the currency is ultimately at the mercy of Brexit negotiations rather than data, since everything hinges on the terms of divorce.

Put a different way, pure economic data is not the main consideration of when the BOE will next raise interest rates, and as such has less impact on the exchange rate. Indeed, this appears to have been the message from last week's September Bank of England policy decision.

"While inflation has started to come back down to earth and retail sales have firmed, economic growth in the U.K. has remained sluggish, with real GDP rising 1.5% annualised in Q2. Given slower economic growth and ongoing Brexit negotiations, we look for the Bank of England to remain on hold in coming quarters until these concerns subside," says a note from analysts at investment bank Wells Fargo.

Advertisement

Lock in your Dollars: Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here