Image © Andrey Popov, Adobe Stock

- Sterling-Dollar hits downside targets and is in the oversold zone

- Increasing chances of a pull-back although downtrend still intact

- The main release for Sterling is inflation and wage data; for the Dollar housing, retail sales and industrial production top list

GBP/USD weakened substantially in the previous week as the Dollar continued rising and fears of a no-deal Brexit weighed on Sterling.

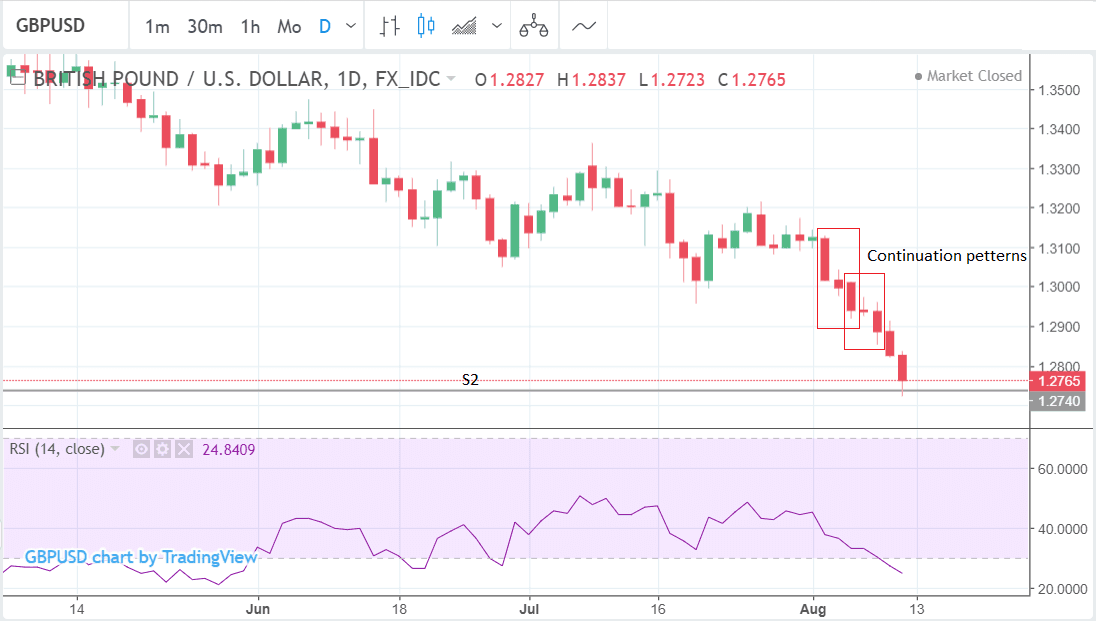

From a technical perspective the pair is oversold, but in the absence of any strong reversal signs the downtrend remains intact, and therefore likely to continue, albeit probably after a pull-back.

The daily chart clearly shows the established downtrend and how momentum in the pane below is now below the 30 level which indicates oversold. If RSI is oversold it is not a wise idea to open further short positions. Of RSI moves out of oversold it is a trend reversal signal and a good time to buy.

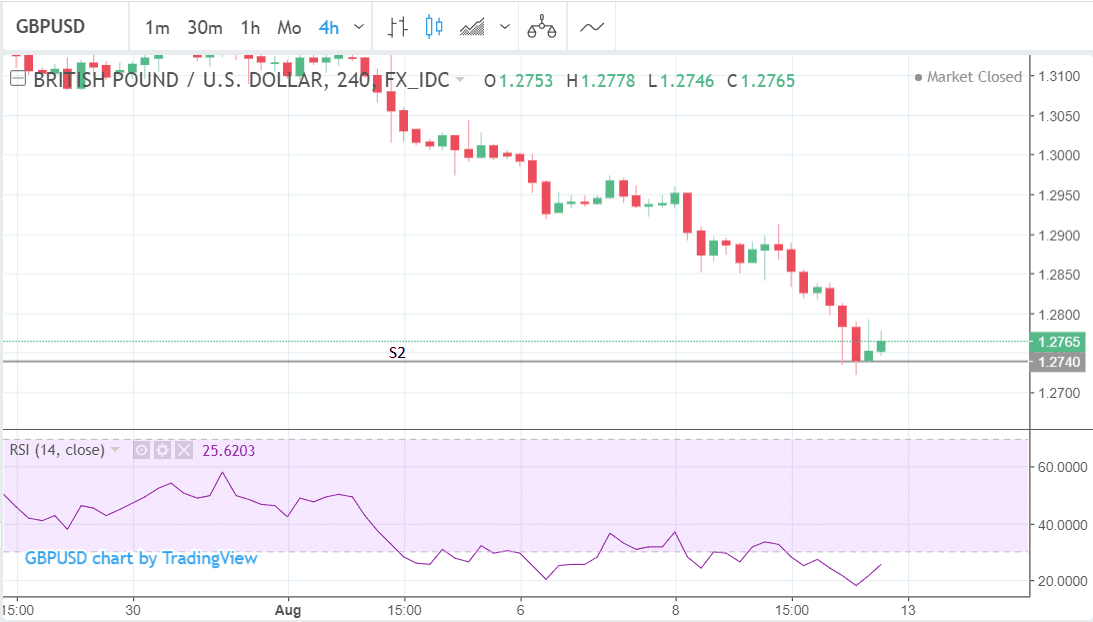

GBP/USD fell to a new low of 1.2725 in the previous week and then bounced. Interaction with the S2 monthly pivot at 1.2740 was probably partly responsible for the bounce since pivots are - as their name suggests - often the location for reversals.

The 4hr chart below shows how perfectly the rebound coincided with the touch of S2.

Downside targets generated by the three-bar continuation patterns we mentioned in previous reports have now been met, the latest being between 1.2700-50. This further suggests an oversold assessment and inclines us to expect a rebound of some description.

It is quite possible that after a short period of consolidation the downtrend will resume and bring the exchange rate to new lows since the downtrend is strong.

Overall we are bearish, but due to the pair's temporary oversold conditions would caution against expecting further immediate declines and await a possibly pull-back before the downtrend resumes.

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The US Dollar: What to Watch this Week

There is a high number or economic data releases out of the US in the week ahead but most of them are unlikely to be market moving unless they disappoint.

The Dollar has grown used to a period of solid US economic outperformance relative to the rest of the world, and we reckon the currency might be vulnerable to any disappointments going forward.

The US-initiated trade war and sanctions (Iran, Russia, Turkey) have raised tensions," says Michael Gapen with Barclays in New York. "While data look set to remain resilient in the short term, we expect the constant threat of escalation to gradually and increasingly weigh on H2 18 activity."

The first big release is retail sales on Wednesday at 13.30 B.S.T, which is forecast to show a 0.1% rise in July compared to the previous month.

Core retail sales, which excludes autos and fuel, is expected to show a 0.3% rise in July.

"Revision to US national accounts suggests a reduced propensity to spend extra income consistent with higher future saving rates," warns Gapen.

Industrial Production, out at 14.15 on Wednesday is forecast to show a 0.3% increase.

"We are a little less optimistic than consensus regarding data forecasts and expect US production to contract," says Gapen.

The next important release is building permits, which is expected to show a 1.4% rise in July compared to the previous month, when released at 13.30 on Thursday.

Housing starts, which showed such a massive -12.4% decline in the month before, are out at the same time and expected to reveal a 7.4% rebound in July.

The Philadelphia Fed Manufacturing Index is out at the same time and expected to come out at 22.3 from 25.7 previously.

The big release on Friday is the University of Michigan sentiment gauge for August, which is expected to come out at 98.1 when it is released at 15.00, a rise from 97.9 previously.

There is a also a fair amount of oil related data, including an OPEC report on Monday, Crude Oil Inventories on Wednesday and API weekly stock on Tuesday.

Sterling: What to Watch this Week

Brexit headlines could be on tap over the next week with EU/UK negotiations resuming on Monday and recent media stories have reported a conditional willingness on the part of EU leaders to accept Theresa May’s plan to aim for a free trade zone in goods, which could be discussed at a special EU Summit in Salzburg next month.

We note this to be one reason why downside damage to Sterling could have been worse.

"This could help to stem further Sterling selling pressure," says George Brown, an analyst with Investec.

We will keep an eye out for any media set-pieces from the main negotiators.

On the calendar, the Pound has three main data releases in the week ahead, the first of which is wage and employment data for July, out on Tuesday, August 14 at 9.30 B.S.T.

Current expectations are for average earnings to come out at 2.5% - the same as in June; and for the unemployment rate to also remain the same at 4.2%.

The next major release is inflation data, also for July, out on Wednesday at the same time. Headline CPI is expected to show a 2.5% rise compared to the same time a year ago, but a -0.1% fall compared to the previous month of June. Core inflation which excludes volatile food and fuel components is forecast to show a 1.9% rise compared to a year ago.

"If inflation turns out to be more robust than expected, then this will fuel speculation over further rate hikes from the Bank of England," says a note from brokers Actionforex.

The inference is that this could also support the Pound since higher interest rates tend to increase foreign capital inflows due to the higher return promised.

"Inflation may rise more sharply in the coming months as the weakness in the exchange rate will likely push up import costs. If the pound’s weakness persistence then in the long-term this should help to boost exports, assuming Britain will strike a good deal with the EU. So whichever way you look at it, sterling will probably make a good comeback in the longer term outlook," add Actionforex.

The final major release for the Pound is retail sales in July out on Thursday, also at 9.30.

Broad, headline retail sales are forecast to show a 2.9% rise compared to a year ago and 0.2% compared to the previous month of June (month-on-month).

Core retail sales, which excludes auto sales and fuel is forecast to rise 2.8% on a yearly basis and 0.2% month-on-month.

Despite the important data on schedule in the week ahead its important to note that broader political and macro themes may be more dominant.

The Pound shrugged off a recent interest rate hike by the Bank of England and fell on Brexit fears anyway, and on Friday it was more moved by Turkish themes than domestic data which was positive, as macro themes dominated its main counterparts and somewhat overshadowed the data.

Domestic economic numbers released on Friday showed GDP expanding by 0.4% quarter-over-quarter in Q2 and construction output surging 1.4% month-over-month in June.

The data had little impact on Sterling which was instead focussed on external drivers like broad-based Dollar strength and the Euro's Turkish-generated woes.

Advertisement

Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here