-US Dollar posts mixed performance Tuesday as rally grows tired.

-TD Securities warn of capitulation after Wednesday's FOMC minutes.

-Economists flag rising inflation expectations, hawks winning at Fed.

© Nazli Sart, Adobe Stock

The US Dollar posted a mixed performance against the developed world currency basket Tuesday as the greenback's month-long rally appeared to grow long in the tooth, leaving strategists and economists divided in their outlook for the currency.

Tuesday's price action comes as strategists at Toronto-based investment bank TD Securities warn of a possible capitulation by the Dollar later this week when the Federal Open Market Committee (FOMC) meeting minutes are released.

"The USD is beginning to exhibit signs of rally fatigue. The upcoming Fed minutes are likely to contain dovish undertones and could be a tipping point for the USD. With the Fed priced to perfection and appreciable backup in yields, the USD may have exhausted the "divergence" narrative," says Mazen Issa, an FX strategist at TD Securities.

This call follow a weeks-long period in which US 2 and 10 year bond yields have reached mulit-year highs of 2.57% and 3.15% respectively, which shocked the US Dollar back into life and helped it convert a 3% 2018 loss into a 1.38% gain.

US yields have stepped higher as the twin forces of rising inflation and President Donald Trump's fiscal largesse, embodied by the budget-busting tax reforms and infrastructure spending plans unveilled in January, saw US Treasuries offered lower on fears over increasing supply and concerns over the impact that accelerating inflation will have on returns.

This has been a game changer as it has altered the relative returns equation for international investors and so called carry traders so that a greater number of those money managers are now incentivised to sell a range of other currencies in order to by the Dollar and invest in the American bond market to exploit these higher US yields.

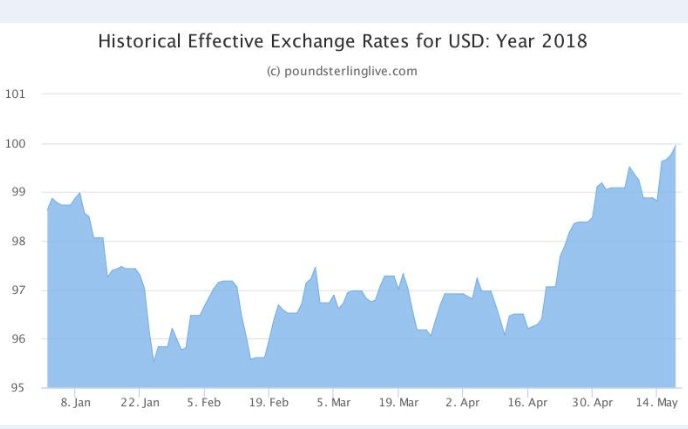

Above: US Dollar index in 2018. Captures April and May rally.

"Against a backdrop of higher rates (including through the overly-emphasized 3% mark in US10s) and a very fully priced Fed (i.e. in line with 2018/2019 dotplot and terminal rate), the USD may have exhausted the “divergence” narrative we have written about over the last several weeks," Issa elaborates. "And, with curve flatness top of mind for many investors and the impending doom it may signal, we are on the lookout for a discussion on this subject matter."

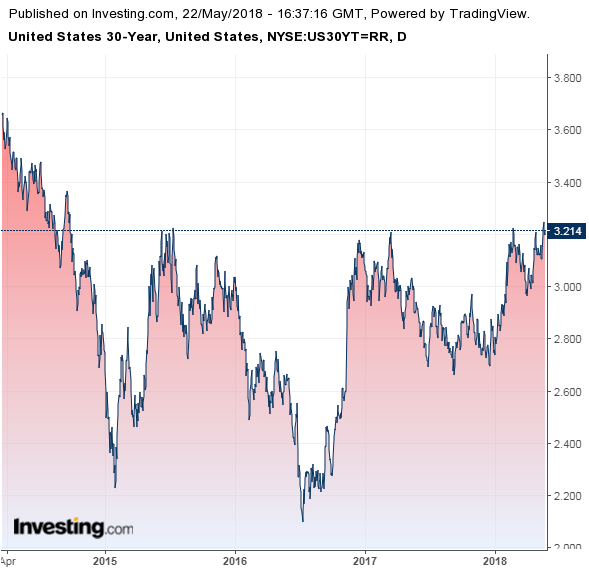

As much as 2-year and 10-year US yields have risen during the last month, and over the last year or two, the increase in longer term 30-year bond yields has been much less impressive. The 30-year yield was at just 3.21% Tuesday making for what it is known in financial jargon as a "flat curve", which describes a situation where short term interest rates are almost equal to much longer-term rates.

Above: 10 Year US Government Bond Yield.

Conventional thinking dictates that, in ordinary times, long term rates should always be higher than short term interest rates so one would expect 30-year bonds to offer a much higher yield than their shorter tenured counterparts. But they don't, the so called "curve" is flat.

Economists are now debating whether this levelling of short and long term rates is a sign of the market calling last orders on the current economic cycle and pricing in an eventual recession - which would explain lower interest rates further out along the "curve".

Above: 30 Year US Government Bond Yield.

TD Securities' Issa expects the Federal Reserve to acknowledge these events in the bond market within the minutes of its latest policy meeting when they are released Wednesday at 1900 London time. But there is a danger that any reference to this would be interpreted as a "dovish" signal of concern at the Fed, or a hint that the central bank may think twice about raising interest rates again in June, which would then be negative for the US Dollar.

However, Tuesday's price action and accompanying strategy note from Issa and the TD team comes at the same time as economists at Capital Economics cite inflation developments as grounds for thinking the Federal Reserve could soon become a bit more hawkish, meaning they would be even more keen to go on raising interest rates.

"The recent rebound in inflation expectations is significant not only because it provides another reason to expect core inflation to trend higher this year, but also because it further weakens the case of those Fed officials arguing against additional rate hikes," says Andrew Hunter, a US economist at Capital Economics.

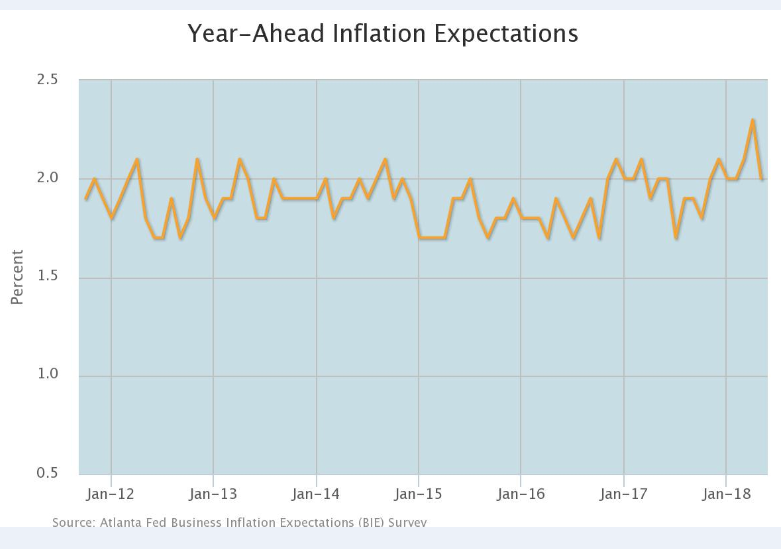

An Atlanta Federal Reserve survey showed business expectations for inflation rising to their highest level since at least the beginning of 2012 last month, with the average projection being for consumer prices to grow around 2.3% over the next year. This is above the Federal Reserve's 2% target and marks a regime shift in the inflation picture because, before now, regular surveys of business expectations had always put year-ahead inflation comfortably below the target rate.

Above: Atlanta Federal Reserve inflation expecations survey graph.

As it stands, the US consumer price index rose to 2.5% during April while the core-CPI measure, which removes volatile food and energy items from the goods basket and so is seen as more representative of domestically generated inflation pressures, held steady at 2.1% Both of these numbers are above the Federal Reserve's 2% target and already prompted the central bank to say at its most recent meeting that it will tolerate an "overshoot" for a period of time in order to avoid a knee-jerk interest rate response that would risk damaging the economy.

"A rise in inflation expectations doesn’t in itself mean that actual inflation will then pick up. But there is evidence that the recent rebound is feeding through to firms’ pricing decisions, with the net share of small firms planning to raise prices now close to its highest level in a decade. On past form, that suggests that core inflation will continue to trend higher this year. Similarly, the rebound in household inflation expectations should be putting upward pressure on nominal wage demands," Hunter adds.

If anything, the current levels of inflation and convergence of inflation expectations with levels that are above the Fed's target would command a more aggressive monetary policy response at some time in the future. On this note, and ahead of the release of the latest FOMC meeting minutes Wednesday, it may prove to have been telling that FOMC rate setters included the following note in the official record of their previous meeting;

"Several participants expressed the judgment that it would likely become appropriate at some point for the Committee to set the federal funds rate above its longerrun normal value for a time. Some participants suggested that, at some point...monetary policy eventually would likely gradually move from an accommodative stance to being a neutral or restraining factor for economic activity."

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.