Adobe Stock

The Pound maintains an upside bias against the Dolalr as we enter the new trading week in which inflation data is the stand out release for the Dollar.

GBP/USD has been rising steadily in a channel in the medium term and given that the trend remains intact the overall forecast is for it to continue.

However, the Pound is still below its 2018 highs nearer the 1.44 region, but the pull-back witnessed over the last few weeks has not done enough damage to suggest the rally is over and shouldn't worry Sterling bulls unduly.

Only a break below the March lows at 1.3712 would suggest the beginnings of a new trend lower; whilst those lows hold, however, we see the bias as bullish overall.

Scoping in to the daily chart and we notice how the pull-back of the last several weeks since the January highs has formed a clear ABC corrective pattern.

ABC's are composed of three waves in a clear zig-zag configuration. We discussed the significance of the ABC on GBP/USD in detail in last week's week ahead forecast, but in summary, ABC's are text book corrections which end at the low of wave C, before the market starts to trend higher again.

Thus so far the market has conformed with this blueprint, completing the correction at the C-wave lows and marching higher for four consecutive days, however, it then sold off quite aggressively last Thursday (March 8), bringing into doubt the validity of the rebound. Overall, however, we remain of the view that it will continue to forge higher and eventually, probably retouch the 1.4345 Jan highs, even if that target seems dubiously distant at the moment.

A break above the downsloping trendline for the correction from the January highs would provide stronger confirmation of a resumption of the uptrend and the eventual retouching of the Jan highs.

Such a break would probably be confirmed by a close above 1.3975.

The bullish forecast is also supported by an analysis of the chart using Elliot Waves. These are labelled on the chart above as bracketed numbers. They indicate the pair has probably just completed a wave 4 correction and is in the process of starting a wave 5 up, which will probably go as far as the wave 3 highs.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Data and Events to Watch For the Dollar

The most important release for the Dollar in the week ahead is inflation data for February, which is forecast to show a rise of 0.2% month-on-month, for both headline and core when released at 12.30 GMT on Tuesday.

Given the extremely strong labour market data out on Friday, which showed payrolls increasing by 313k in February, expectations are tilted to the upside, since a healthy labour market generally creates greater inflation pressure.

"Unless CPI or retail sales is abysmal, Fed Chair Jerome Powell will deliver his very first rate hike the following week," says Kathy Lien, Managing Director of BK Asset Managment.

A more inflationary result would indicate that the Federal Reserve (Fed) might need to increase interest rates more aggresively than previously expected, and higher interest rates tend to lead to a stronger currency because they attract more foreign capital inflows.

Retail Sales is the other big release in the week ahead when it is scheduled to come out at 12.30, on Wednesday, March 14.

The consensus expectation is for a 0.3% rise month-on-month in February; a higher result would be benificial for the US Dollar and vice versa in the event of a lower print.

Other data in the week ahead includes Empire State and Phillidelphia Fed Manufacturing data, with the former expected to show a rise and the later a fall when they are released on Thursday at 12.30.

Housing and Michigan sentiment data round of the week when they are released on Friday.

The ongoing trade war and Trump's promise to meet Kim Yong-Un are further matters which could rattle markets in the coming week.

The main threat to the Dollar is from retaliatory measures taken by large trade blocks against the US - such as the EU or China since these will hit US exports and therefore direct demand for Dollar denominated goods.

The meeting with Kim is likely to impact on traditional safe-haven currencies like the Yen and the Swiss Franc more than the Dollar, with the greater signs there are of an entente cordial pressuring havens lower versus the Dollar.

Data and Events to Watch for the Pound

The main event for the Pound in the week ahead is probably the Chancellors’ Spring Statement. This is a new initiative brought in by Philip Hammond to provide an update on the economic and fiscal outlook.

No changes to the budget are expected and the statement is only scheduled to last 15-20mins according to media reports, which is a mere rump of the Autumn statement.

Budget's do not often move currencies so the Pound may not react, however, alongside the statement are revised forecasts from the Office of Budgetary Responsibility (OBR) which if substantially altered may impact on growth prospects and therefore Sterling.

The OBR has, on balance, been overly pessimistic in the past, generally undershooting with its forecasts and leading some commentators to expect it to revise up its forecasts on Tuesday.

"It is always difficult to predict other institutions’ forecasts. However in terms of the Spring Statement, we would expect the GDP growth projections to be a little more upbeat," says Ryan Djajasaputra, analyst at Investec.

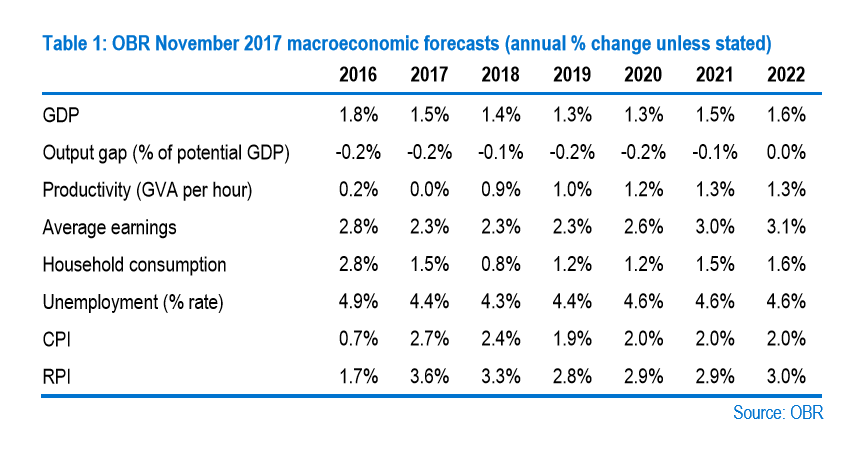

The OBR's most recent forecasts are contained in the table below.

For the sake of context, Investec's own house forecasts are for 1.7% growth in each year.

The other main event is the Bank of England's (BOE) Financial Policy Committee (FPC) meeting on Monday (statement published Friday 16) to discuss possible changes to capital buffers, introduced after the financial crisis under the Basel 3 regulatory framework.

The focus will be on whether the BOE reviews the size of the "Counter Cyclical Capital Buffer" (CCYB), a piece of regulation which guards against excessive bank-lending during upturns and excessive parsimony during downturns - thus the "counter-cyclical" sobriquet.

In November it was raised to 1%, with the FPC also indicating that it could be increased further in H1 2018 - so there is a possibility of a change at the meeting.

Again, this is unlikely to hit FX markets in any major way, and even if it does the impact may be difficult to gauge beforehand.

The CCYB impacts on the supply of credit, and therefore on inflation and growth, which in turn influence currency value, and it will probably form a part of the bigger picture that currency analysts consider in relation to their forecasts.

Generally increases in the supply of credit are seen as inflationary and likely to increase interest rates, which in turn lead to capital accumulation and a stronger currency.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.