© ulu_bird, Adobe Stock

The White House budget and Wednesday's US inflation numbers are both Icebergs in the water for markets this week. Meanwhile, the Dollar and stocks will take their cues from the 10 year yield.

It is still too early to begin selling Dollars and piling back into global stock markets, according to one strategist, despite Friday’s recovery in American stocks and a softer Dollar on Monday morning.

The statement comes as the greenback and stock markets are increasingly slaves to the trajectory of the 10 year US government bond yield, which embodies market concerns about the future direction of both inflation and interest rates.

“The FX market (in my opinion, anyway) is now more sensitive to long-term rates than to short-term ones. It's interested in the destination of rates rather than short-term path, and so is interested in where terminal fed Funds are, rather than how many times the Fed hikes this year,” says Kit Juckes, chief FX strategist at Societe Generale.

Wednesday's inflation figures will provide bond markets and the Dollar with their next cues, while the 2.9% yield threshold is a key level to watch as far as the 10 year note goes, according to Juckes.

“So the dollar (it can be argued) has benefited from a jump in longer-dated yields because that reflects speculation about a higher terminal Fed Funds rate,” Juckes adds.

“Likewise, equities have fallen and volatility spiked because the market's confidence in the idea of a sub-3% peak in Fed Funds has been challenged.”

Juckes’ statements come after the US Dollar snapped a two month long losing streak, leading the Dollar index to rise by 1.17% during the seven days to Monday 12, February. The last year has been peppered with intermittent bouts of Dollar strength although all have been short lived.

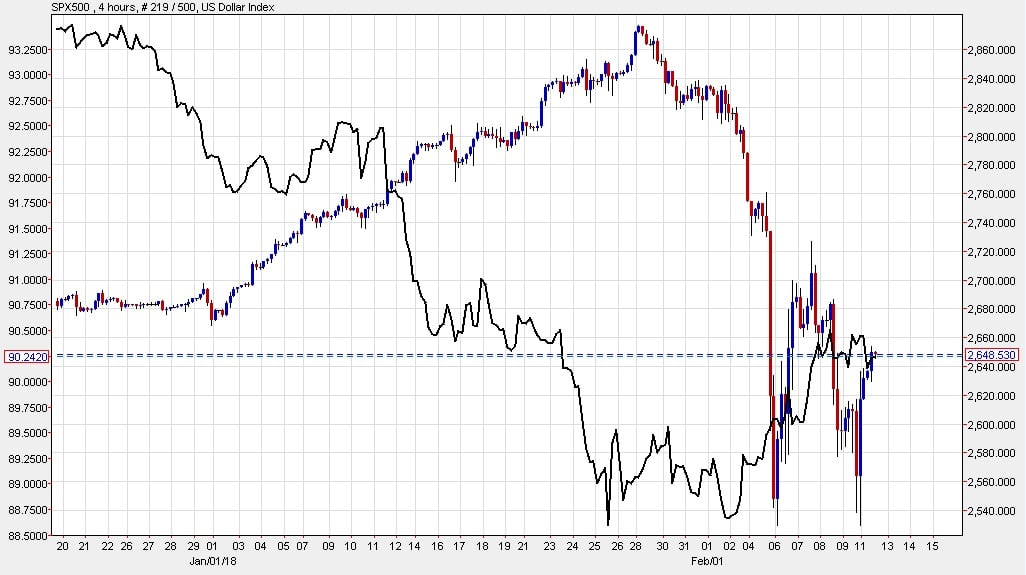

Source: Netdania Markets. S&P 500 index (red and blue) with US Dollar index (black) overlay.

The Dollar’s latest resurgence is a symptom of financial market volatility having come back with a bang at the start of February, following more than a year of relatively benign trading conditions.

Clearly, the Dollar moves inversely to US stock markets at the moment, although this is a trend that dates all the way back to the 2016 election of President Donald Trump.

Recent volatility is the result of investors having been forced to consider whether they were being too complacent about the outlook for inflation and interest rates.

January jobs numbers from the US gave impetus for this soul searching after it showed wages and new jobs both growing strongly during the month, leading some observers to float the idea that the Federal Reserve may be less patient about raising rates in 2018 than it has in prior years.

“The price action for the S&P 500 will be crucial for financial markets in the near-term. One of the most telling observations so far has been the relative containment of the move, particularly in FX where the fallout has been relatively modest,” says Derek Halpenny, European head of global markets research at MUFG.

“That is often the case initially and it is only when the move becomes sustained or large enough to alter expectations about the economy that broader financial market turmoil begins to set in. We are certainly not there yet.”

The jobs report and subsequent fears over inflation and interest rates sent stock markets tumbling and the VIX index, which is a measure of volatility on the S&P 500, surging by more than 150% in a single session. It’s largest single day rise on record.

However, these inflation fears were exacerbated Friday when the US government set out details of its new budget, which promises big increases in Federal government spending and will be unveiled in full on Monday.

“In some ways, the rising fear of inflation is understandable. In December, we had confirmation of a USD 1.5trn unfunded tax giveaway, which has been followed by a government spending deal that adds a further USD 300bn of stimulus on top of the evidence of stronger wage growth and a 10% depreciation of the dollar last year,” Halpenny adds.

Above: Pound-to-Dollar rate shown at 2 hour intervals. Captures February.

The US Dollar index was quoted 0.20% lower at 90.28 during early trading in London Monday while the Pound and Euro managed to advance on the American currency, posing the question of whether the Dollar recovery has run out of steam already.

“That said, if a better risk mood just encourages 10s to spike up through 2.9% at the start of the week, it seems unlikely that we will see equities bounce too far and by the same token, it's too early to sell dollars and go looking for either higher-yielding currencies, or Euros, to buy instead,” writes Societe Generale’s Juckes.

America’s 10 year yield rose to 2.877% during early trading in London Monday, taking it to its highest level since December 2013 and within an inch of the 2.9% threshold that Juckes suggests is key for an extension of the stock market rout and Dollar bull run.

“As for the next proper test, it comes with Wednesday's CPI data, where a dip in core inflation to 1.7% is expected. The market's fears about higher inflation are going to need to be validated at some point, or the dollar downtrend will resume,” Juckes adds.

Above: US 10 Year Yield dating back to 2015.

Wednesday will mark the release of January’s US inflation numbers, which are expected to show headline inflation picking up while core inflation falls by a fraction for the month.

Core inflation excludes volatile commodity items from the price basket and so it is seen as a better measure of underlying, or true, domestic inflation pressures. It is this measure that markets will be watching more closely.

“A softer print on Wednesday would go some way to easing current investor fears. Wage inflation did not emerge in 2017 and even if you believe the data last week is a sign of things to come, usual lags mean this will not be evident in consumer prices until toward year-end or even into 2019,” says MUFG’s Halpenny.

A weaker than expected inflation number might be enough to bury the current fears over inflation for a while longer, which would pave the way for a recovery in stock markets and a resumption of the US Dollar downtrend.

Equally, but on the opposite side of the coin, a stronger than expected rise could mean yet more losses for stocks and continued recovery for the greenback.

“We suspect that investors’ fears over inflation should subside over the coming weeks...But after the scale of this equity price correction, investors are likely to remain defensive this week. Even a slight upward surprise in the inflation data could be enough to warrant a further sell-off,” Halpenny concludes, in a note Monday.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.