- GBP/USD softer but holds week’s lows after fed's taper surprise

- Fed suggests QE taper to be announced & commenced in 2021

- Amid economic progress, but bond yield impact to be “modest”

Above: Federal Reserve Chairman Jerome Powell. Image © Federal Reserve.

- GBP/USD reference rates at publication:

- Spot: 1.3704

- Bank transfers (indicative guide): 1.3324-1.3420

- Money transfer specialist rates (indicative): 1.3580-1.3608

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Pound-to-Dollar exchange rate entered the Thursday session on the back foot but having weathered better than many others the Federal Reserve’s revelation that it will likely announce as well as commence a tapering of its quantitative easing programme before year-end, triggering a rally by the Dollar in response.

Minutes of the Fed’s July meeting revealed late on Wednesday that a majority of Federal Open Market Committee members felt the necessary economic conditions would likely be met over the coming months so that the process of steadily reducing the bank’s $120BN per month quantitative easing (QE) programme could not only be announced, but also be commenced before the year is out.

“Looking ahead, most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year because they saw the Committee’s “substantial further progress” criterion as satisfied with respect to the price-stability goal and as close to being satisfied with respect to the maximum employment goal,” the minutes read.

That was something of a bombshell for the great many investors, traders, analysts and observers out there who’d assumed the FOMC would go no further this year than announcing mere plans to begin reducing bond purchases from some time in the New Year.

“Participants agreed that the Committee would provide advance notice before making changes to its balance sheet policy,” the minutes later say. “Many participants noted that, when a reduction in the pace of asset purchases became appropriate, it would be important that the Committee clearly reaffirm the absence of any mechanical link between the timing of tapering and that of an eventual increase in the target range for the federal funds rate.”

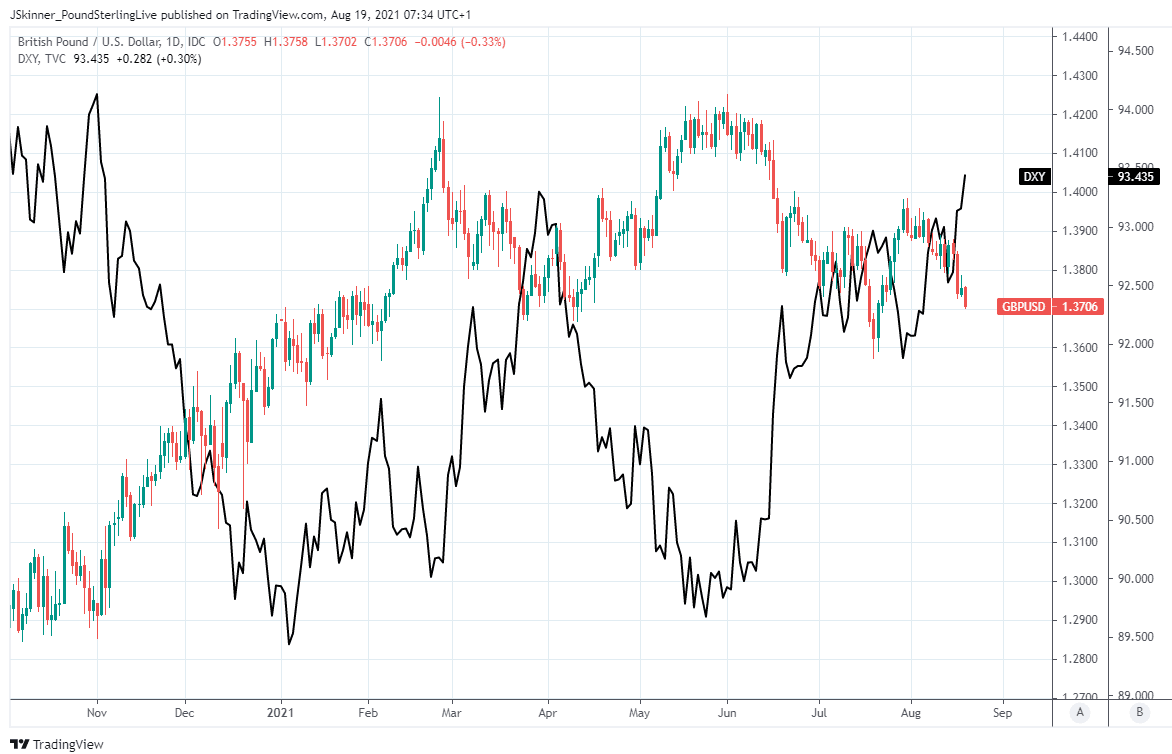

Above: Pound-to-Dollar rate shown at daily intervals alongside U.S. Dollar Index.

The Dollar and broader currency market had approached Wednesday’s release of the July 27-to-28 meeting record with only a hope of a hint offering some kind of clarity on the Fed’s plans as far as the QE taper and its other monetary policies are concerned, and more than indulged by the bank.

“It is worth remembering the FOMC’s July meeting took place before the bumper July non‑farm payrolls report where the unemployment rate dropped from 5.7% to 5.4%,” says Joseph Capurso, head of international economics at Commonwealth Bank of Australia.

“We retain our call that the FOMC will announce a tapering in September followed by implementation in October or possibly November,” Capurso adds.

July’s non-farm payrolls report released in early August showed the U.S. economy creating close to a million jobs for the second consecutive month, cultivating as a result the appearance of a mounting risk that something would be announced in September, although unlike the CBA team few had envisaged the bank as likely to actually begin reducing the monthly pace of asset purchases this year.

“We are tentatively of the view that the Federal Reserve will announce QE tapering at the September FOMC meeting with the slowing of purchases starting in October. Comments from Fed officials suggest it will be fairly swift and most probably conclude in 2Q 2022. That is, of course, contingent on the resurgence of Covid not leading to a reversal in economic performance,” says James Knightley, chief international economist at ING.

With only three more FOMC meetings left to go in the year, and the bank having made a commitment to provide advanced notice before beginning to reduce its footprint in the bond market, any announcement would need to come in either September or November if it’s to go into effect this year.

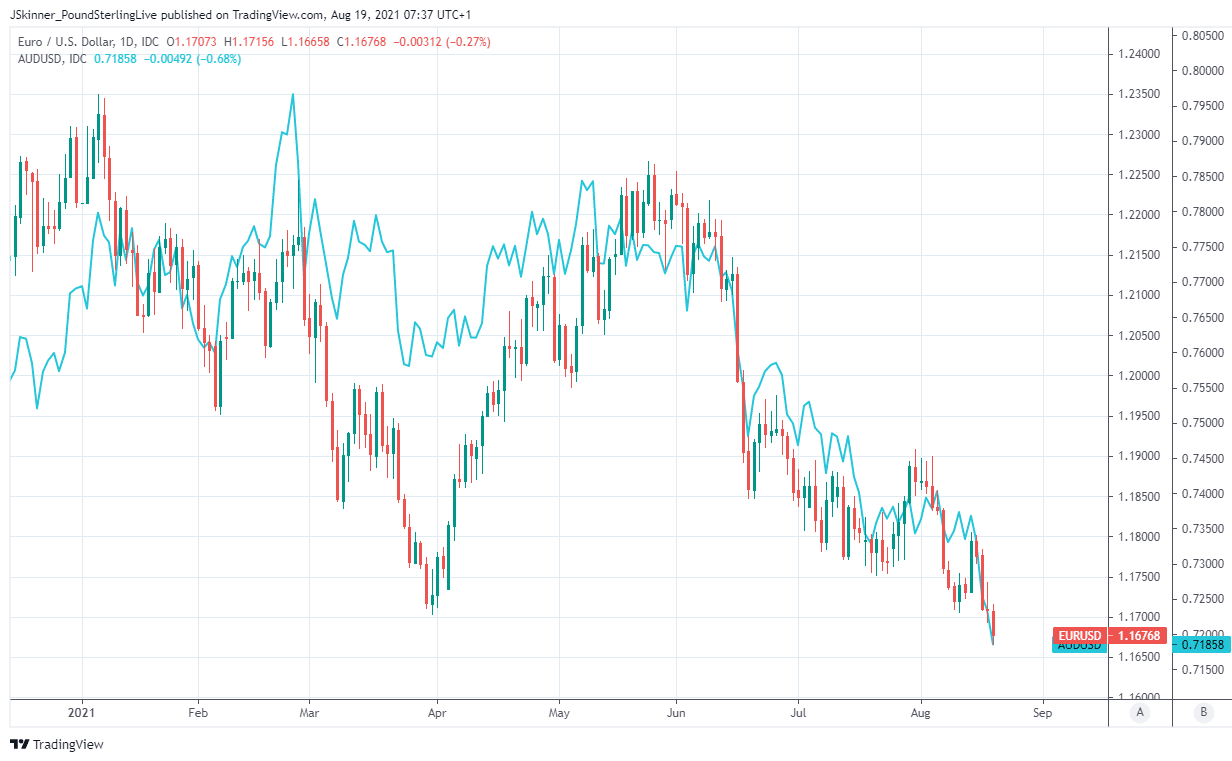

Above: Euro-Dollar rate shown at daily intervals alongside AUD/USD.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

“The next key Fed event will be the Jackson Hole seminar next week, with the chairman likely speaking on Friday, August 27. (The daily schedule has not yet been released.) We don't expect the message to be dramatically different from what came out of the minutes today, but the advance signaling process for tapering can probably be stepped up a bit more,” says Jim O’Sullivan, chief U.S. macro strategist at TD Securities.

“We continue to forecast a formal taper announcement in December, although November remains possible if the next two employment reports are unexpectedly strong,” O’Sullivan adds.

The Pound-to-Dollar exchange rate slipped back toward, but remained above the week’s lows near 1.3720 in the overnight session, while other Dollar facing exchange rates fell to new lows including the Euro-Dollar rate which dipped a fraction below 1.17 for the first time in 2021.

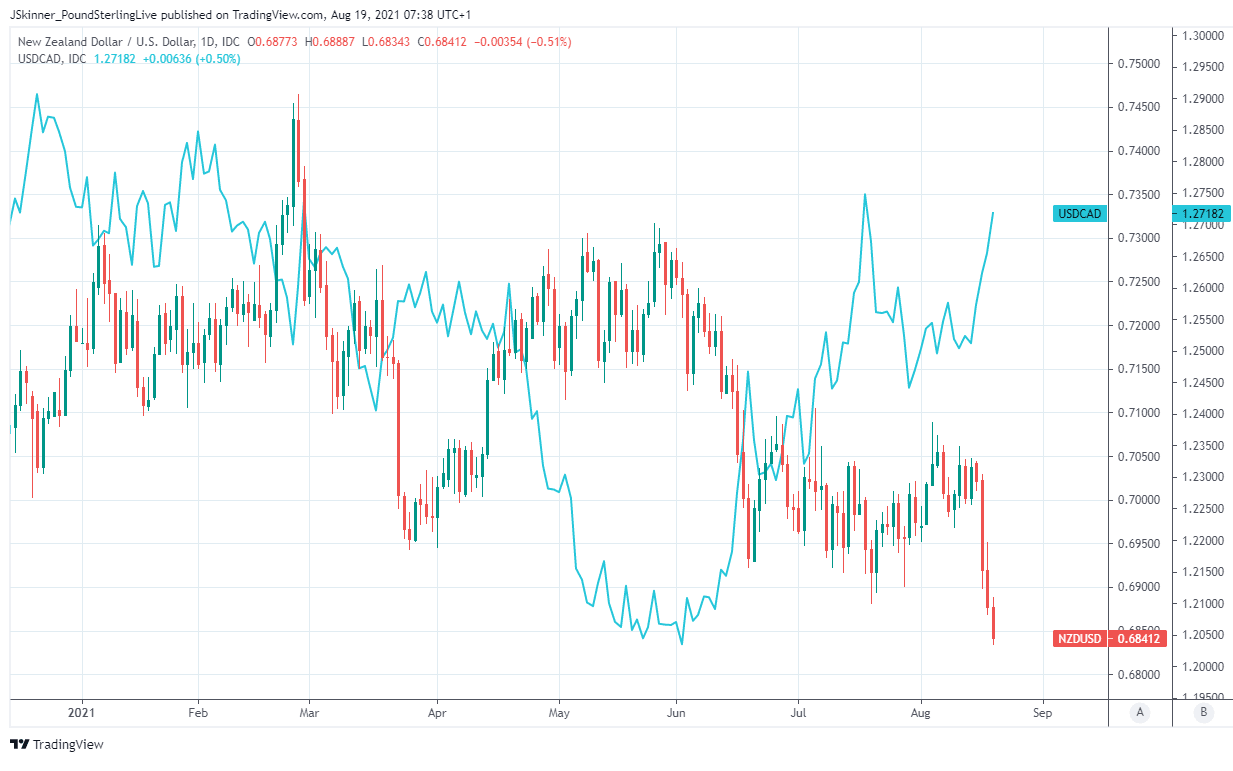

The Australian and New Zealand Dollars both slipped to new lows for the year of 0.7210 and 0.6850 respectively following the release, while the USD/CAD exchange rate reached 1.2678; a mere one-month high.

“Changes in asset purchases could be interpreted by the public as signaling a shift in the Committee’s view of the economic outlook or in its overall policy strategy, with implications for the expected path of the federal funds rate,” the FOMC minutes noted. “Changes in the flow of asset purchases could also influence yields, but this influence would likely be modest outside of periods of stressed financial market conditions.”

Above: NZD/USD shown at daily intervals alongside USD/CAD.

The potential rub for the Dollar, and possible saving grace for other currencies in the months ahead however, is the Fed’s estimation that an eventual decision to reduce the scale of its bond purchases will have only a limited impact on the overall level of U.S. bond yields.

That potentially blunts the extent to which a QE taper can burnish the greenback’s appeal to investors, while the FOMC’s stated intention to discourage the market from reading a tapering decision as having implications for its benchmark interest rate is also potentially a dampener for the currency.

“Our read is that Fed officials will continue to signal ongoing steps toward normalising policy, providing the USD with crucial ongoing underlying support,” says Richard Franulovich, head of FX strategy at Westpac.

“Delta’s spread will likely slow US recovery momentum in coming weeks but it’s still much better placed than other less vaccinated regions, notably Asia. Dollar Index weakness should be limited to the 91.50-92.0 area, with new highs likely in Q3,” Franulovich warns.

The Fed has been buying $120BN per month of U.S. government and publicly insured but private sector mortgage bonds since soon after the onset of the coronavirus crisis, and has kept the Fed Funds rate range at 0%-to-0.25% throughout this time.

It has guided since December last year that “substantial further progress” toward a full recovery of the labour market is necessary before it would contemplate changing the quantitative easing programme, and still insists on a full job market recovery and sustainable achievement of its 2%-average inflation target before any changes to the Fed Funds rate range are announced.