- GBP/USD in sharp drop

- Surging bond yields scare equity investors

- 'Risk on' GBP suffers

- But analysts say no reason to be alarmed just yet

Image © Adobe Images

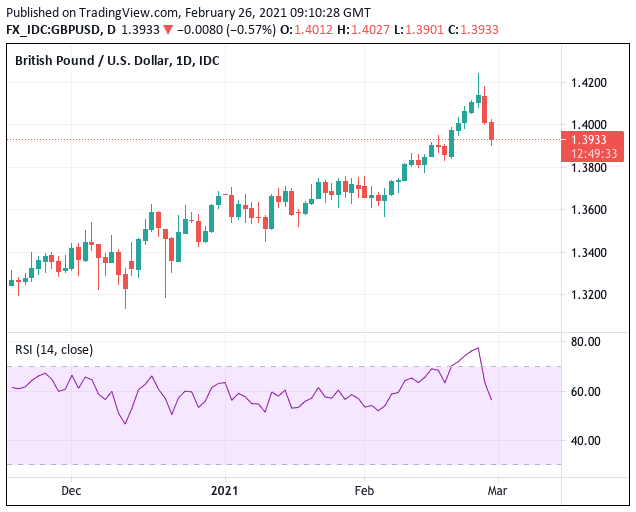

- GBP/USD spot at publication: 1.3933

- Bank transfer rates (indicative): 1.3545-1.3643

- Money transfer specialist rates (indicative): 1.3728-1.3835

- More information on securing bank beating rates, here

The British Pound has fallen ahead of the weekend and has unwound some of its stellar 2021 advance, amidst a global sell-off in government bonds and an associated equity market slump.

The Dollar has meanwhile found favour as investors bring forward their expected date of the next Federal Reserve interest rate hike, resulting in the GBP/USD shedding over a percent of its value since its mid-week peak.

"Cable is now over 300 points from the Wednesday morning flash highs and we have month end to contend with which has certainly been shaken up by the recent moves in assets in the past 24 hours," says a note from the JP Morgan spot trading desk in London.

Where Sterling once traded as a proxy to Brexit-related sentiment and anxieties, it now follows the ups and downs of global investor sentiment.

Ahead of the weekend this sentiment has taken a turn for the worse with stock markets shedding weight and bonds selling off, leading to a sharp spike in the yield these bonds offer.

Analysts say the developments indicate investors are expecting a boom in economic activity over coming quarters that will lead to higher inflation and reduced central bank support.

The perverse market function whereby good news = bad news for stocks is therefore firmly in play.

Above: GBP/USD corrects lower following a strong rally that left the pair overbought (See overbought RSI conditions in lower pane).

"The move in yields (nominal and real) has become too burdensome for the market to take and this was triggered in part by continued apathy from the Fed towards recent developments and then the shocking 7 year auction. Sharp deleveraging ensued with the favourites taking significant baths, GBP, NOK, CAD, AUD, TRY, you name them," says JP Morgan.

What matters for Sterling at this juncture is whether or not investors rediscover their confidence and therefore how bond markets proceed will be key.

"Yields on 10yr Treasuries rose an astonishing +14.4bps yesterday to 1.520%, bringing them to levels not seen for over a year now, albeit they’ve fallen back -2.6bps this morning. To demonstrate how rare daily moves of this size are, the only times in the last 5 years we’ve seen a rise in yields this large have been at the height of the coronavirus pandemic last March, and the day after President Trump’s election in 2016. So not moves you expect to see every day," says Jim Reid, an economist at Deutsche Bank.

Crédit Agricole says the rationale for dumping U.S. government bonds (thereby driving up their yield) is "fairly simple" and cites a yawning U.S. budget deficit and building inflationary pressures.

They note that Congressional Budget Office estimates the current U.S. output gap to be around 3.0% of GDP and the Biden administration is trying to pass through US Congress a fiscal package valued at around 9.0% of GDP.

This comes on the back of the December stimulus of around 3.0% of GDP that has already led to a blowout retail sales print in January.

"Also boosting the yield rally is growing government bond supply as well as the rebound of global commodity prices," says Valentin Marinov, Head of G10 FX Strategy at Crédit Agricole.

{wbamp-hide start}

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |

For now, policy makers do not seem too concerned however, with U.S. central bankers tending to view the moves in bond markets as being a healthy response to expectations for improved economic growth rates over coming months.

Reid cites the case of Kansas City Fed President George who on Thursday said "much of this increase likely reflects growing optimism in the strength of the recovery and could be viewed as an encouraging sign of increasing growth expectations."

St. Louis Fed President Bullard said that "I think the rise in yields is probably a good sign so far because it does reflect better outlook for U.S. economic growth and inflation expectations which are closer to the committee’s inflation target".

But Reid says there are signs that markets could well be moving faster than the Fed, with a full first hike now priced in within the next two years.

"For reference, the most recent dot plot from the FOMC in December showed the median dot remaining on hold even at the end of 2023, so there’ll be intense focus on the release of the next set of dots at the meeting in mid-March to see if officials stick to that assessment," says Reid.

The foreign exchange playbook says that when market expectations for a central bank interest rate rise are brought forward, the currency that central bank issues rises in value.

So despite a host of reasons for the Dollar to be weaker in 2021, expectations for an interest rate rise are proving supportive.

Reid notes a string of better-than-expected data releases that bolstered an argument that investors were reacting to the potential for a stronger recovery than they were previously anticipating.

Better-than-expected data includes weekly initial jobless claims for the week through February 20 which fell to 730k (vs. 825k expected), which is one of the timeliest indicators we get on the state of the economy.

Furthermore, the previous week’s figure was revised down by -20k while the number of continuing claims also fell to a post-pandemic low of 4.419m (vs. 4.460m expected).

"And if that weren’t enough, durable goods orders similarly rose by a stronger-than-expected +3.4% in January (vs. +1.1% expected), with the previous month’s growth also revised up seven-tenths. Data releases over the coming days should help to fill in the picture further, with both the ISM readings and the February jobs report coming out next week," says Reid.

For the Pound-to-Dollar exchange rate to find its feet again investors will need to shake off recent nerves and start dipping back into the market.