Image © Adobe Images

- GBP/USD spot rate at time of writing: 1.3650

- Bank transfer rate (indicative guide): 1.3272-1.3368

- FX specialist providers (indicative guide): 1.3445-1.3554

- More information on FX specialist rates here

The U.S. Dollar cemented its position as the best performing major currency of the week following the release of December inflation figures that appear to have revived concerns about a possible 2021 tapering of the Federal Reserve's (Fed) quantitative easing programme.

U.S. inflation rose 0.4% in December alone, taking the annualised rate of consumer price growth up to 1.4% and not a country mile away from the symmetric 2% target of the Federal Reserve.

The more important core rate of inflation, which ignores volatile prices of energy, food and regulated items like tobacco and alcohol, rose by a lesser 0.1% but left sitting even higher than the headline measure and at some 1.6%.

Fed policymakers face a significant logistical challenge in the wake of last week's Georgia State election victory by the Democratic Party, which gave the incoming administration of President Elect Joe Biden a narrow but viable congressional majority and likely means much higher federal government spending and debt issuance than would otherwise be the case.

The prospect of increased government spending has lead to some market speculation that inflation could soon start rising more agressively, with some econonomists warning that inflation could accelerate faster than many market participants are assuming.

Rising inflation expectations were reflected in a rise in U.S. bond yields as investors demanded greater future returns to compensate for any erosion to their investments caused by inflation over coming years.

"The year-to-date move higher in 10-year yields is now 28bps before yields corrected lower yesterday and that under any circumstance is a notable move in just seven trading days. It was laying the ground for a correction stronger for the US dollar over the short-term," says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG.

Above: Pound-to-Dollar rate shown at 4-hour intervals alongside AUD/USD.

Investors have so-far assumed that issuance resulting from federal government spending will be automatically lapped up by a Fed that has closely matched its bond purchases with the extraordinarily increased spending needs of the government throughout the pandemic.

Matching the extraordinary demands of the public the purse was necessary to preserve “market functioning” and minimise economic scarring from the pandemic.

But if members of the Federal Open Market Committee of rate setters were to allow investors to go on assuming that they'll underwrite whatever profligacy does or doesn't characterise the incoming administration, they would risk aiding and abetting an eventual 'taper tantrum' that leaves the stock, bond and currency market volatility of 2013 looking like a teddy bears' picnic, given the vastly increased numbers involved.

"It seems the ‘taper talk’ of Monday is part of an intellectual discussion playing out that is designed to focus our attention on the possibility of tapering to avoid complacency without spooking markets later," says Neilson Wilson, chief market analyst at Markets.com.

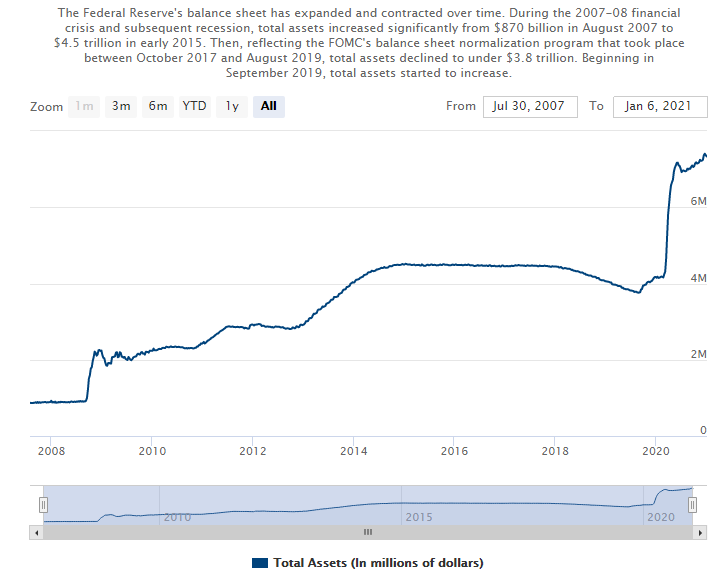

Above: Total assets held on Federal Reserve system balance sheet as of January 06.

This is likely why despite almost no economists seeing a credible case for a near-term tapering of the bank's $120bn per month bond buying programme, FOMC officials have begun to contemplate aloud the likely timing of an eventual tapering excercise, taking great care in the process to make clear that such a move will be expressly tied to attainment of its statutory employment and inflation and not the whims of Biden's Treasury Department which will be lead by former Fed Chairwoman Janet Yellen.

That more than anything else may be why currency markets responded with a bid for the U.S. Dollar to December inflation figures released on Wednesday, which may have been an investment equivalent of fools' gold, given the above.

The Dollar was higher against all major currencies for the session, cementing its position as the best performer of the week and in contrast to widespread expectations for declines this month as well as throughout 2021.

"Looking ahead, inflation will continue to rise. Assuming we do see a full reopening in the months ahead, the combination of increased demand in an economy that has seen supply capacity shrink is likely to generate rapid price increases in several components of the inflation basket. The question is whether this is merely price level recovery or the start of something longer lasting and potentially destabilising," says James Knightley, chief international economist based in the New York office of ING.

Above: U.S. Dollar Index shown at daily intervals alongside Euro-to-Dollar rate (blue).

U.S. inflation rose 0.4% in December alone, taking the annualised rate of consumer price growth up to 1.4% and not a country mile away from the symmetric 2% target of the Federal Reserve. The more important core rate of inflation, which ignores volatile prices of energy, food and regulated items like tobacco and alcohol, rose by a lesser 0.1% but left sitting even higher than the headline measure and at some 1.6%.

Fed policymakers are charged with using interest rates and other monetary policies in order to ensure that inflation - which is sensitive to both economic demand as well as supply side factores - averages a steady 2% over time. They did much of what they have done in the last year for the sake of safeguarding as much of the economy's long-term inflation generating potential as possible, but currency and bond market's are now clearly concerned about rising price pressures and what the Fed might do in response to them.

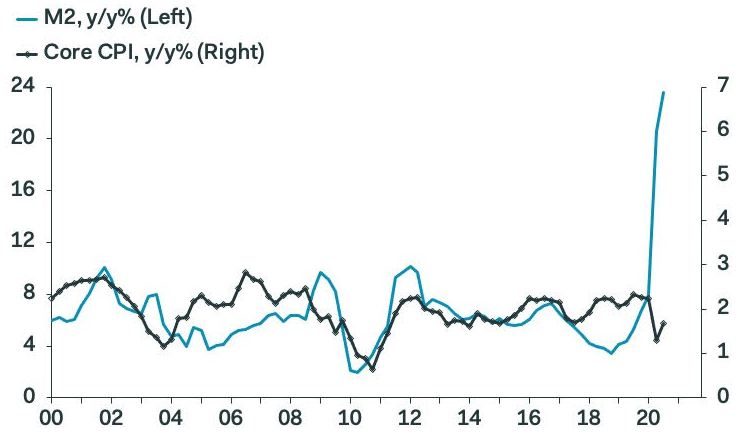

"Margin expansion is very clearly visible in components where demand has been strong throughout the pandemic, notably household appliances - up 16.6% y/y - and limited service restaurants," says Ian Shepherdson, chief economist at Pantheon Macroeconomics. "We just don’t know yet if the surge in demand we expect post-pandemic will drive margin expansion across much broader swathes of the CPI. But the 25% y/y rate of growth of the M2 money supply - by far the fastest since 1960, when consistent data start - is making us nervous."

Source: Pantheon Macroeconomics.