Image © Adobe Images

Image © Adobe Images

- USD set for losses after Fed's Williams pitches large cuts.

- Says not to risk inflation target just to "keep powder dry".

- Comments seen as argument for large 0.5% July rate cut.

- Morgan Stanley says hobbling USD is key to global recovery.

- GBP losses slow USD decline, Morgan Stanley sells USDJPY.

The Dollar stabilised Friday after a steep overnight fall but the greenback is set for further declines in the final session of the week and will remain on its back foot into month-end, according to multiple analysts, who're tipping the currency to weaken as the Federal Reserve (Fed) begins cutting its interest rate.

New York Federal Reserve President John Williams said late Thursday that U.S. central bankers should not seek to "keep powder dry" amid signs that inflation pressures are ebbing from the economy while interest rates are still close to their record lows.

Williams analogised vaccinations and the short-term discomfort they create in order to avoid disease or pain in the long-term in what appeared to be an argument for decisive preemptive action from the Federal Reserve at the end of July. He held up Japan and the Eurozone, which have resorted to increasingly extraordinary and unorthodox interest rate policies due to a complete loss of sufficient inflation pressures, as examples of what could happen to the U.S. if the Fed doesn't act quickly.

I like New York Fed President John Williams first statement much better than his second. His first statement is 100% correct in that the Fed “raised” far too fast & too early. Also must stop with the crazy quantitative tightening. We are in a World competition, & winning big,...

— Donald J. Trump (@realDonaldTrump) July 19, 2019

The speech came at a time when momentum is believed to be ebbing from the economy, when many measures show inflation pressures weakening and while expectations of future prices pressures are low and falling further. There's been significant uncertainty over the likely response from the Federal Reserve this month, with markets unsure whether it will cut U.S. interest rates to 2.25% or 2.5%. The difference, and outlook beyond there, is significant for markets.

Above: Dollar Index shown at daily intervals, annotated for recent events.

"Fed communication indicates that it does not intend to repeat the BoJ’s mistake of the 1990s," says Hans Redeker, head of FX strategy at Morgan Stanley. "The Fed's focus has shifted towards external demand weakness and disturbingly low US inflation expectations. Dovish Fed policy is warranted to compensate for low inflation and the potentially growth-weakening effect of low inflation on highly leveraged sectors of the US economy."

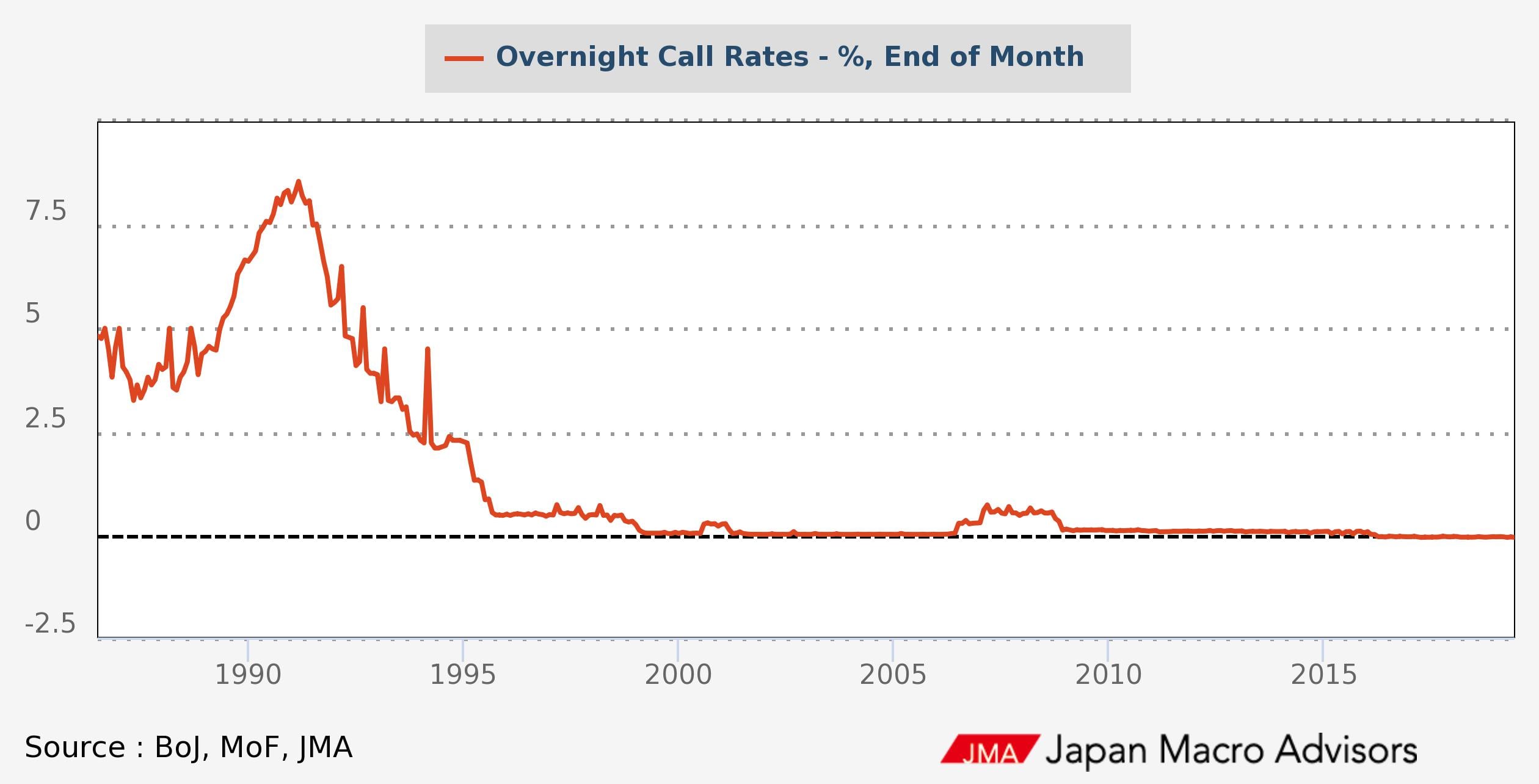

After a long and sustained economic boom, the Bank of Japan (BoJ) lifted its interest rate from 5.25% to 8.5% between June 1989 and March 1991, which not only burst a stock market bubble that had taken almost a decade to inflate but also drove a then-highly leveraged economy into recession.

The BoJ's response to the burst bubble and ensuing recession ultimately led to a 'lost decade' of low or negative inflation and weakening GDP growth. It took the bank until May 1992 to reverse those growth-killing rate hikes. It wasn't until the end of 1993 that the economy had received stimulus equal in size to the monetary tightening that drove the country over the edge. Many economists have since lamented that the BoJ was far too slow to respond to the recession and the deflation it set off.

Above: Bank of Japan interest rate since 1989. Source: Japan Macro Advisors.

"John Williams and Richard Clarida have also re-ignited expectations that the Fed starts off with a 50bp rate cut on 31 July – though our team still prefers 25bp. Importantly it is clear that the market has sunk its teeth into the disinflainterestedtion, secular stagnation story and is only interested in the response from policy makers," says Chris Turner, head of FX strategy at ING Group. "Investors will ultimately buy into the Fed’s reflationary efforts – which include a weaker dollar."

U.S. policymakers who're seeking to avoid repeating the mistakes of the BoJ would most likely be in favour of significant action from the Federal Reserve in response to signs of a downturn being on the way. If the numbers of those people on the Federal-Open-Market-Committee outnumber those who want to take things more slowly then it could be bad news for the U.S. Dollar and good news for the Pound-to-Dollar rate.

Turner says the Dollar index should fall from 96.99 to 96.35 this Friday evening and that it's likely to weaken further in the months ahead. ING is looking for only one 25 basis point interest rate cut from the Fed in July and but Morgan Stanley and many others in the market still see a risk of a larger 50 basis point cut that's followed by a further 25 basis point reduction in early 2020.

Above: Pound-to-Dollar rate shown at daily intervals.

"We think the most topical market question is not whether the Fed will cut 25bp or 50bp in July but if it is enough to stop global growth weakness," writes Morgan Stanley's Redeker. "The DXY USD index should weaken materially if the Fed suggests it is open to more than just an insurance rate cut.For now, however, the DXY index may take longer than we anticipated to weaken as GBPUSD remains on a downtrend, limiting EUR too."

Changes in interest rates are normally only made in response to movements in inflation, which is sensitive to growth, but impact currencies because of the push and pull influence they have over capital flows. Capital flows tend to move in the direction of the most advantageous or improving returns, with a threat of lower rates normally seeing investors driven out of and deterred away from a currency. Rising rates have the opposite effect.

The Federal Reserve raised its interest rate four times in 2018 as the U.S. economy expanded at an increased pace, aided by White House tax cuts, and inflation rose above the 2% target. It has now lifted rates nine times since the end of 2015 but inflation has recently fallen below the target and growth is now expected to slow as global growth decelerates in response to the White House trade war with China.

Above: USD/JPY rate shown at daily intervals.

"We remain short USD/JPY given our expectation for the Fed to continue surprising the market to the dovish side. Fed communications may begin guiding the market toward anticipating 50bps of cutting (in line with our expectation). We think a 50bp cut is particularly likely," Redeker says. "We like fading the small USD rally after a stronger-than-expected retail sales print, since the June Fed minutes indicated that 14 members of the committee cited downside risks to the US growth outlook."

Some surveys have suggested the manufacturing sector is creaking under stress from the trade war, with U.S. firms contending not only with the cost of President Trump's import tariffs but also a deterioration of the global economy that is threatening domestic and international demand. Official data did confirm Tuesday that U.S. industrial firms struggled in the recent quarter, with production falling 1.2%, which marks a second consecutive fall that means the industrial sector is now in recession.

Those surveys could yet portend a U.S. slowdown but official data has so-far revealed only that the economy gathered steam in the opening quarter. Second quarter data due out in August will reveal what happened to the economy after its strong start to the year. That data will also tell the Federal Reserve whether it needs to panic about the outlook for growth and inflation or not.

"The overvalued USD would be a tool to reflate on a global scale by reducing its value," says Morgan Stanley's Redeker. "The Fed has policy options that the ECB and BoJ no longer appear to have. The July 31 FOMC meeting may show that the Fed is willing to use this flexibility. This meeting may reveal how much international responsibility the Fed is willing to bear at this point."

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement