Image © Adobe Images

- Pull-back meets key support level and could bounce

- Resumption of established bull-trend forecast

- Pound eyes potential surprise Brexit vote

- Dollar eyes labour market statistics

The Technical outlook for GBP/USD is constructive and we would expect Sterling to maintain its 2019 bias for strengthening. But, we are wary of a surprise vote on Brexit, while a broadly stronger U.S. Dollar could provide headwinds.

The Pound-to-U.S. Dollar rate is trading at 1.3204 at the start of the new week after rising 1.15% during the week before..

The gains were all the more impressive given the U.S. Dollar was broadly well supported across global FX markets, suggesting there is genuine Sterling strength behind the move.

The U.S. currency rose on a variety of factors last week, including stronger-than-expected Q4 GDP data, which helped assuage slowdown fears, U.S. 10-year Treasury yields hitting 1-month highs, tensions between India and Pakistan helping to drive up safe-haven flows and Federal Reserve Chairman Jerome Powell expressing optimism on the U.S. economy.

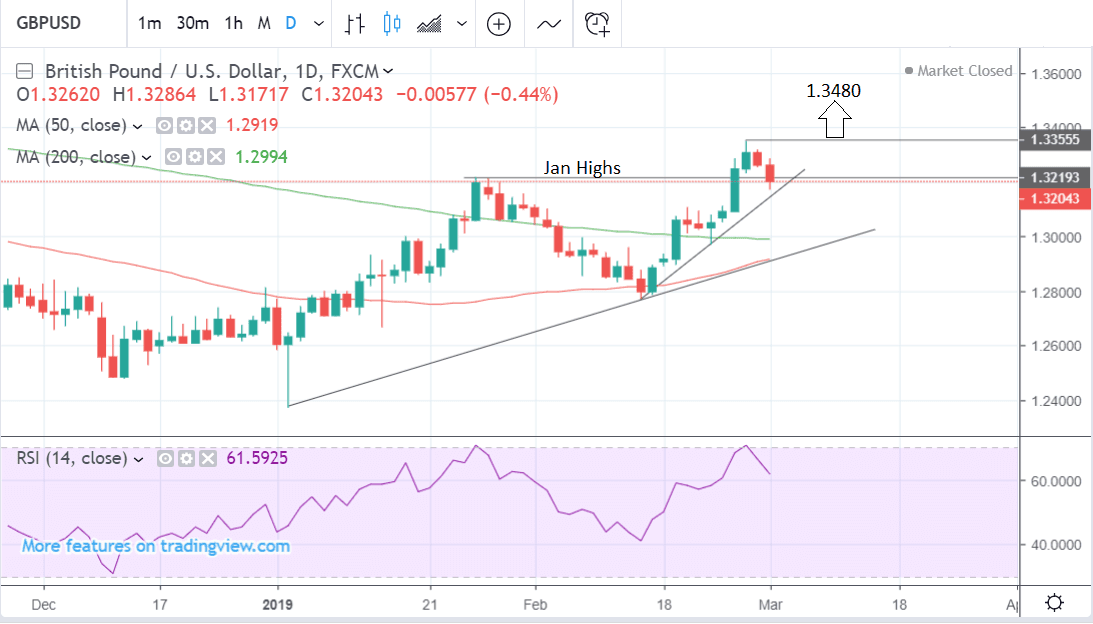

From a technical perspective, the GBP/USD outlook is similar to that of its sister pair GBP/EUR: which is in an established short-term uptrend, and whilst it has pulled back of late, is forecast to resume.

After peaking last Wednesday at 1.3350 the pair corrected back on Thursday and Friday but the correction is relatively shallow and unlikely to extend. What is more likely is that the dominant uptrend will resume and push the exchange rate higher. Although GBP/EUR looks more bullish, GBP/USD is still biased to gain, on balance, and a break above last week’s highs would provide confirmation of an extension higher.

The pair has now touched down on a major support level at the 1.3218 January highs, which is a prime candidate for a rotation higher.

The pull-back on Thursday and Friday is shallower than the previous rally, and this indicates a greater (circa 60%) chance that Monday will probably be an up-day. This is further evidence the uptrend is likely to resume.

Momentum, which was overbought, has now also moved back down out of the overbought zone, indicating traders have lightened their positions a little and the market is now more balanced. This suggests the conditions are more supportive for a resumption higher as the long trade is less ‘crowded’.

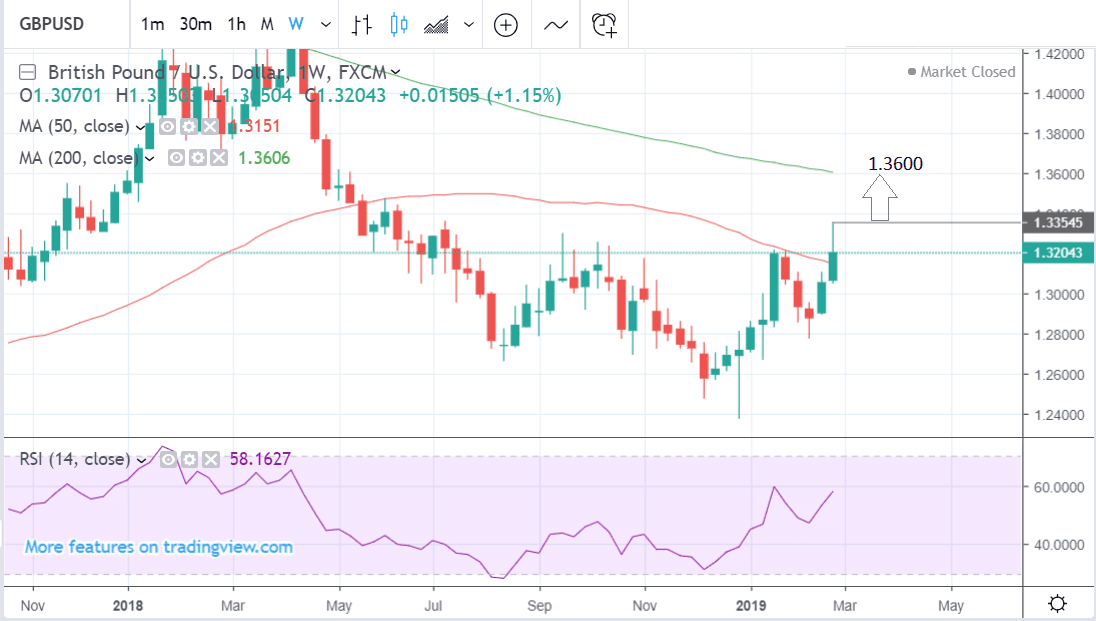

A break above the 1.3350 highs would provide confirmation of gains to the next target at 1.3480, followed by 1.3600. This is possible in the next week or two.

Last week ended with the exchange rate above the key 50-week moving average, which was a major sign of strength. It means the MA has been broken on a ‘closing basis’. This increases the bullish bias.

The 50-week at 1.3151 is also a support level like the January highs and could also be the site of a rotation higher should the exchange rate fall to it.

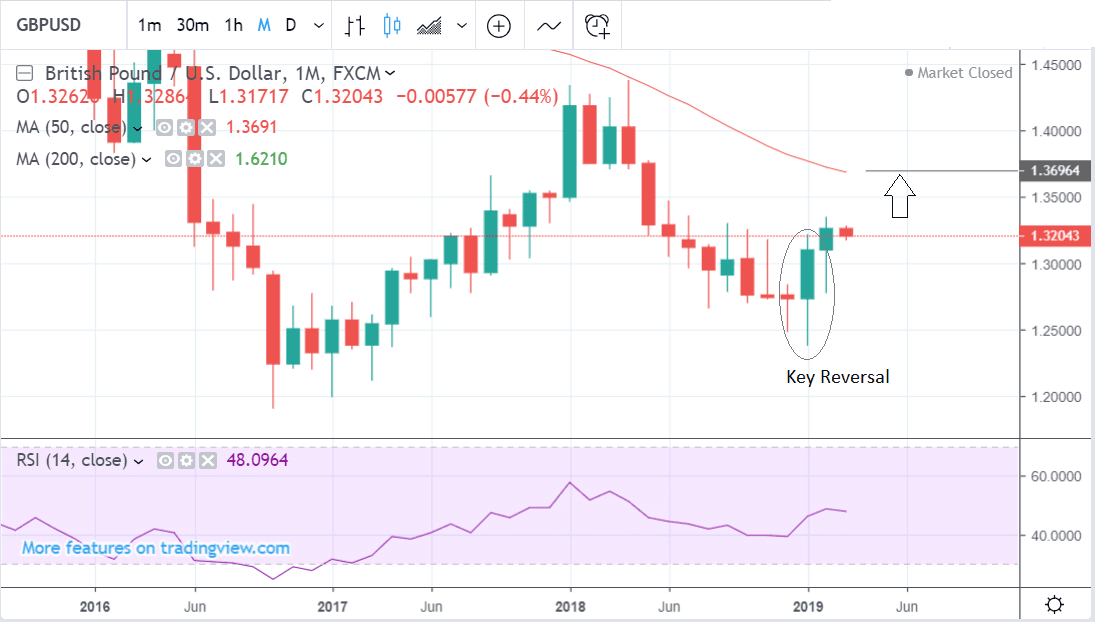

The key reversal candlestick which formed in January is another bullish sign which indicates the longer-term trend has probably reversed from bearish to bullish. This is especially true now that it has been followed up by another bullish month in February.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The Dollar: What to Watch this Week

Labour market statistics form the main 'hard' data release in the week ahead for the Dollar.

Non-farm Payrolls are forecast to rise 180k in February after increasing by a very strong 304k in January. Most of the attention, however, will not be on the headline payrolls figure but on the accompanying wage data since this has more of a bearing on inflation and therefore Federal Reserve policy on interest rates.

Average hourly earnings are expected to have risen by 0.3% in February from 0.1% in January. A greater or lesser-than-expected rise could impact on the U.S. Dollar.

Higher wages equal higher inflation normally, and this puts pressure on the Federal Reserve's FOMC to raise interest rates. Higher interest rates tend to push up the value of a currency by attracting and keeping greater inflows of foreign capital.

“Another blowout report would raise questions about how long the FOMC may remain “patient” before lifting rates further this year. A surprisingly soft number, however, is unlikely to sway the Fed’s near-term policy stance given that a broad array of data still point to a strong jobs market overall,” says a client briefing from economists at U.S. lender Wells Fargo.

Non-manufacturing ISM data is a major release for the U.S. Dollar in the coming week. It is forecast to show a 57.2 rise from 56.7 previously when it is released at 15.00 on Monday, March 4.

The ISM is a sentiment survey based on the responses to questionnaires from pivotal procurement managers in the sector under observation. A result above 50 indicates expansion and below contraction. They are normally strong leading indicators for the economy.

“With the shutdown over, we expect to see a modest bounce-back in the February ISM non-manufacturing index, consistent with the service-sector PMIs from the Federal Reserve system rebounding,” say Wells Fargo. “Another near-60 reading would suggest that the U.S. economy is handling recent “crosscurrents” without much issue and therefore raise the prospect of the FOMC increasing the fed funds rate again this year. A downside miss, however, would support the FOMC remaining in its current holding pattern on rates.”

Other key data for the Dollar next week includes December new home sales on Tuesday (at 15.00), and the final reading of the December trade balance (at 13.30) on Wednesday.

The Pound: What to Watch this Week

The main releases for the Pound next week are services and construction PMIs for February, although, the possibility of an early meaningful vote on Theresa May’s latest Brexit deal remains an overarching risk.

If Theresa May can win concessions from the EU on making the Irish backstop temporary, she may bring forward the meaningful vote before the March 12 deadline date, which means it could happen as soon as next week.

Due to political manoeuvring, any deal she agrees has a higher chance of getting voted through than was the case in January when the deal was shot down by parliament. Brexiteers fearful of Brexit being reversed could be more prone to back May, provided she can get a legal concession on the backstop.

Last week Sterling rose sharply after the Prime Minister announced a series of votes would take place in the event of her Brexit deal being rejected: one of them would be a vote on requesting a delay to Brexit.

With parliament heavily skewed against a 'no deal' Brexit, markets expect a delay to be requested should May's deal fail: for Brexiteers such an outcome would be incredibly problematic as it could open the door to a series of events that results in a much 'softer' Brexit, or no Brexit at all. Suddenly May's Brexit is looking a whole lot more attractive. Last week we heard Jacob Rees-Mogg, the head of the European Research Group which is a cabal of Brexiteer Conservative Party MPs, was softening his stance on the changes required for the deal to get his backing.

“British Prime Minister Theresa May could bring the meaningful vote on her Brexit deal to Parliament early before the March 12 deadline if she manages to secure the legal assurances she is seeking from the EU that the Irish backstop would be temporary if triggered,” says Raffi Boyadijian, economist at broker XM.com. “There seems to be growing movement within MPs, particularly among Eurosceptics, to back the deal if May obtains the legal guarantee after she offered lawmakers a vote on ruling out a no-deal scenario and extending Article 50. Labour’s backing of a second referendum also rattled hardline Brexiteers who may now fear Brexit could be postponed or even aborted.”

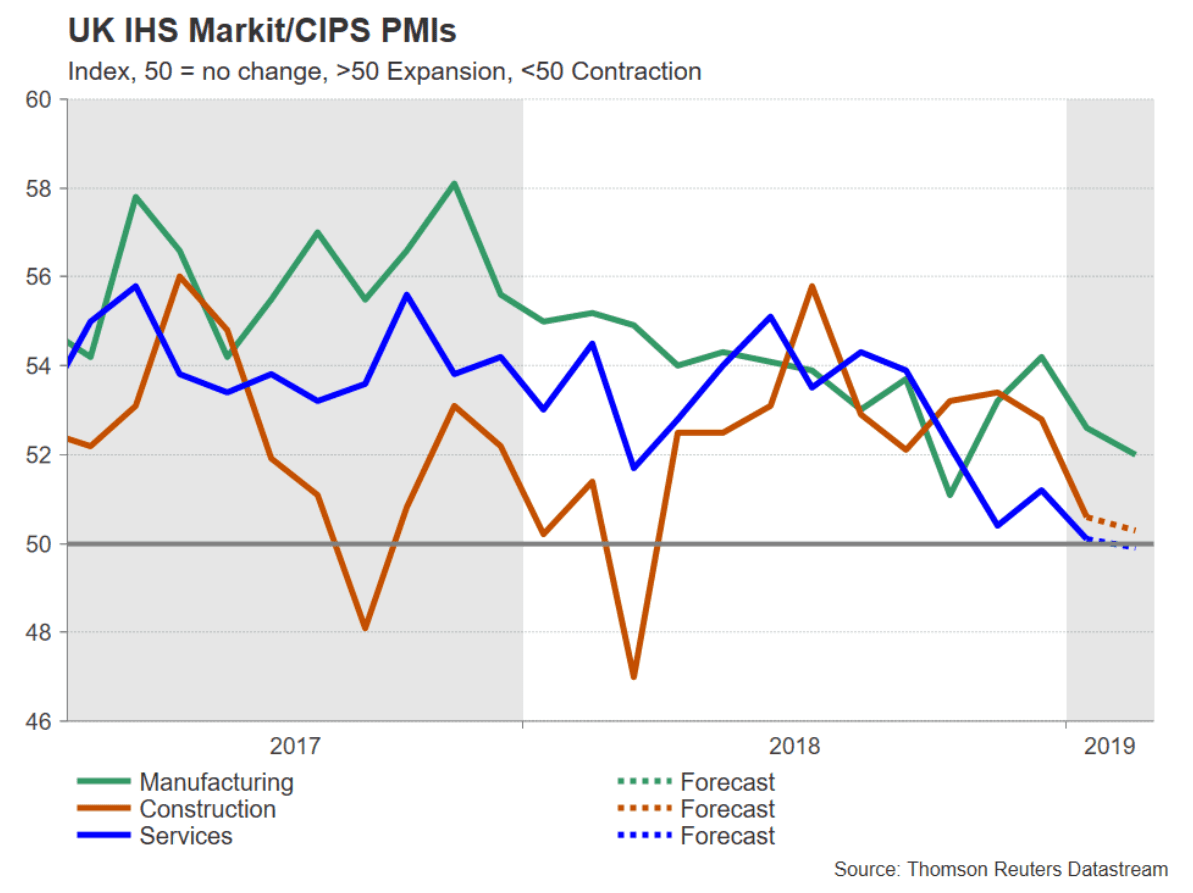

The other main release for the Pound is services and construction PMIs. Construction is the first to be released, on Monday at 9.30 GMT, and is forecast to slow to 50.3 from 50.6 previously.

Services is out on Tuesday at the same time and is forecast to come out at 49.9 from 50.1 in January. The services sector accounts for over 80% of UK economic activity and is therefore the survey markets are most interested in and has the greatest market-moving potential.

PMIs are surveys of pivotal purchasing managers in companies within the target sector. They are a leading indicator for the economy. A lower-than-forecast result could weaken the Pound. The possible dip below 50 for the UK’s key services sector is particularly concerning since 50 is the dividing line between growth and contraction. Brexit is not the only determinant of Sterling. Now that fears of no-deal have eased economic data is playing a greater role too.

* Advertisement