Image © jcomp, Adobe Stock

- GBP/USD forecast to fall as trend extends

- 1.2660 key ‘make or break’ level for outlook

- GBP dominated by Brexit vote; USD by inflation data

The Pound-to-Dollar rate ended the week at 1.2726, marginally below the previous week's close, after UK political uncertainty dragged Sterling lower.

In the coming week GBP/USD is forecast to continue its trend lower, subject to technical confirmation, although we stress our call is not a conviction call, since strong hints of bullish potential are also evident.

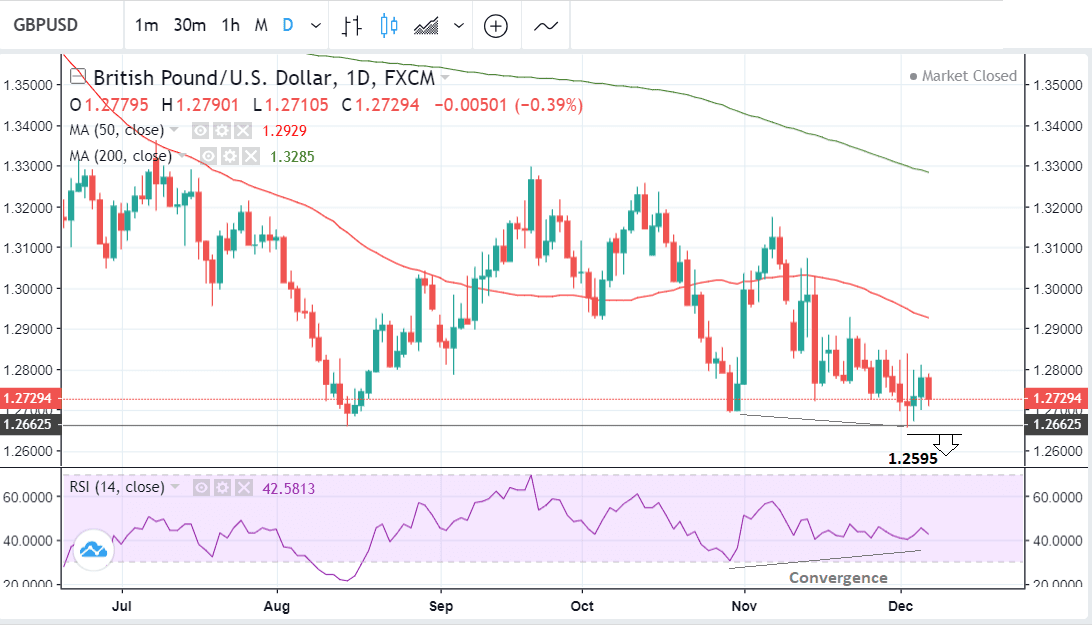

The absence of a reversal in actual price action, however, means the downtrend remains intact and the advantage is still with ‘bears’.

We expect a continuation of the short-term downtrend confirmed by a clear break below the 1.2660 floor, heralded by a move below 1.2650.

Such a move would green-light a continuation down to a target at 1.2595 and the S1 monthly pivot. Pivots, as the name suggests, are levels where prices are more at risk of reversal, they, therefore, lend themselves to adoption as targets.

As already mentioned, there are substantial bullish indicators also evident on the charts.

The pair recently touched down on support at the 1.2660 August lows and bounced. This appears to be a key support level and is likely to be a tough floor to crack, and a bounce is perhaps more likely than a breakdown.

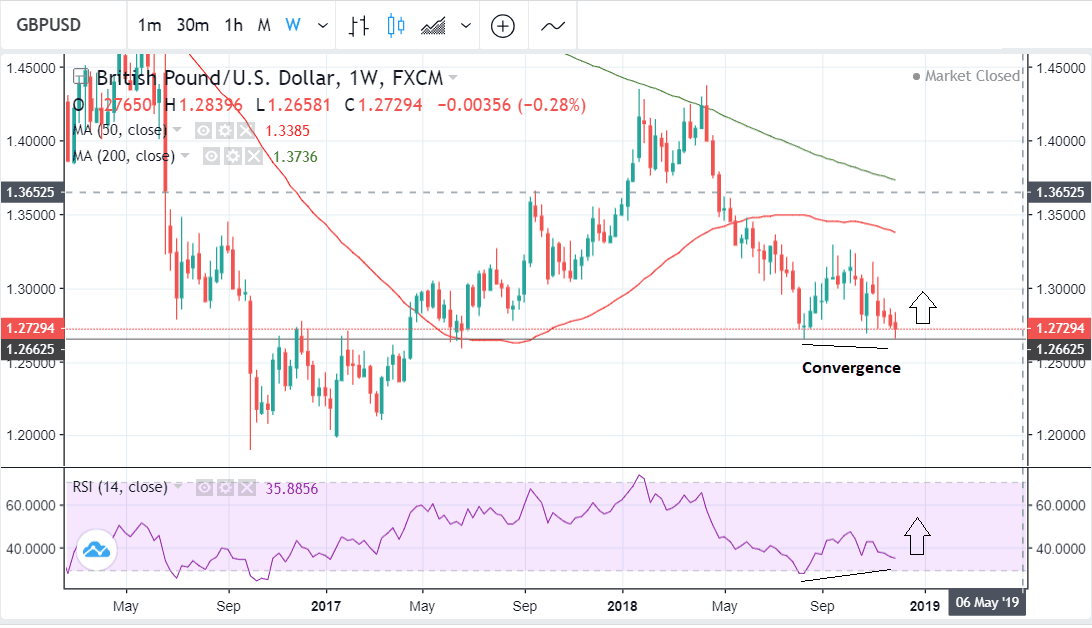

The converging RSI momentum indicator on both the daily and weekly charts in the bottom panel is also a bullish sign.

Convergence occurs when new lows in the exchange rate are not matched by corresponding new lows in momentum. It suggests bearish sentiment is lacking and the pair is vulnerable to a reversal.

These two signs together introduce doubt into the bearish forecast but do not totally negate it. Nevertheless we urge caution for anyone dealing in the markets given the contradictory signals, especially because of the high fundamental event risk scheduled in the week ahead.

Advertisement

Bank-beating GBP/USD exchange rates. Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Dollar: What to Watch

The main data release for the U.S. Dollar is inflation data out on Wednesday because of its impact on interest rates, a primary driver of currencies.

Broad US inflation is forecast to rise by 0.0% in November after a 0.2% rise in October. The slowdown is thought to be partly as a result of a precipitous fall in oil prices.

Core inflation which excludes food and fuel is forecast to rise by 0.2% like it did in the previous month.

Higher inflation pushes up interest rates, especially if it is due to stronger growth, and this pushes up currencies. Even if inflation eases in November analysts at Wells Fargo do not expect the US Federal Reserve, the body tasked with setting base interest rates, to change their expected course of raising interest rates in December.

“We expect the pullback in headline inflation to have no bearing on the Fed’s rate decision for December. A softer-than-expected print for core inflation would also be unlikely to deter the Fed from going ahead with its widely-telegraphed hike in December. A miss on the core, however, could make officials comfortable with a more gradual path of policy tightening in 2019,” says a client note from economists at Wells Fargo.

Another event which might impact on the Dollar is the growing diplomatic crisis between Beijing, Ottawa, and Washington over the arrest of Meng Wangzhou, the CFO of Chinese mobile phone company Huawei, (and daughter of its owner) over her alleged fraud to avoid U.S.-imposed sanctions on Iran.

Meng is being held in Canada pending extradition to the US for trial. China has demanded she be released, saying her detention is, “unreasonable, unconscionable and vile in nature.”

The issue is fast becoming a major diplomatic incident which could easily boil over and impact the fragile trade war truce struck between the U.S. and China at the previous week's G20 summit.

Something similar is possible between China and the U.S. Quite how this would play out for the economies and currencies of the two superpowers is difficult to predict, but given China’s greater dependence on the U.S. then the other way around it is more likely to lose out from an escalation.

As such, if anything the Wangzhou incident could benefit the Dollar more than the Yuan, initially, if the conflict deepens.

The other key hard data release for the Dollar is Retail Sales on Friday, at 13.30, which is forecast to show a slower 0.2% rise in November from the previous month’s 0.8%. Given the power of the US consumer, retail sales is a pivotal metric of growth.

Industrial Production, out at 14.15 on Friday is forecast to rise 0.3% in October.

The other key hard data release for the US Dollar is IHS Markit PMIs for Manufacturing and Services, out at 14.45 on Friday. These are survey based gauges of activity and reliable leading indicators of broader economic growth.

Manufacturing PMI is expected to pull-back a basis point to 55.2 in December from 55.3 previously. Services is forecast to rise to 55.0 from 54.7.

The Pound: What to Watch

Despite rumours the vote may be postponed, the coming week promises to be busy for Sterling if the crucial Brexit vote in Parliament goes ahead.

It is an event which has the potential to start a new era for the Brexit story and Theresa May’s future in her role as Prime Minister and leader of the Conservative party.

Parliament’s meaningful vote on the government’s Brexit deal is scheduled for Tuesday 11, at 19.00 GMT. The government is currently expected to lose the vote and this could cause some short-term weakness for the Pound.

Rumours have surfaced over the weekend that the vote could be delayed whilst Theresa May attempts to draw more concessions from Brussels, but further clarification from Downing Street confirm the vote will indeed progress as planned.

For Sterling, the extent of the loss is key. If the loss is smaller than expected, May will take heart that some further concessions on the political declaration from European leaders can help the deal go through.

"We would not expect Sterling to slump if she loses by a narrow margin," says Thomas Pugh with Capital Economics.

If the government loses by 200 or more votes Theresa May could resign. She could also simply head back to Brussels and insist talks are reopened telling the European Union if they do not a 'hard Brexit' becomes inevitable.

The Labour party may also force a vote of no-confidence which could lead to a general election if the government loses, however this would require some Conservative party MPs to vote with the opposition, which is unlikely.

"A decisive defeat could have a more significant market impact though. Theresa May might have to face down a vote of no confidence in the government and a leadership challenge, which would rattle markets," says Pugh.

A second referendum is also said to be a further possible outcome, however we doubt there is a majority in the House of Commons for this.

The bottom line? No one quite knows what will happen next.

"Political uncertainty is likely to continue to hang over the economy for at least the next few months," says Pugh.

Beyond Brexit, a major release for the Pound is GDP data, which is forecast to show a slowdown in October when it is released at 9.30 on Monday. The average over the previous 3 month period was 0.6% but this is expected to slow to 0.4% in the most recent period.

Industrial and Manufacturing production are also released at the same time and forecast to show a slowdown.

Industrial production is expected to show a -0.1% decline in October, and Manufacturing a 0.0% change.

Labour market data is forecast to show little change in November with the unemployment rate stuck at 4.1% and pay excluding bonuses at 3.2% whilst pay including bonuses continues to show a 3.0% rise. Overall employment change is expected to show a 20k rise.

"We expect to see another robust, if unspectacular, rise in employment in the three months to October. Meanwhile, wage growth probably edged up further," say Capital Economics.

Finally, balance of trade data is out on Monday at 9.30. The deficit in the previous month of September was a very marginal -£0.03bn.

"We think the trade balance slipped back in to deficit in October, as imports rebounded and the recent strength of exports came to a halt," says Capital Economics in a note covering the coming week. "Surveys also suggest that exports, which performed well in recent months, fell back in October."

Advertisement

Bank-beating GBP/USD exchange rates. Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here