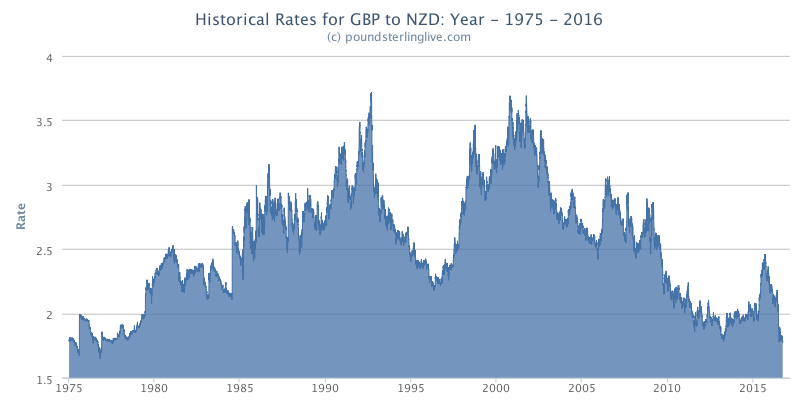

The GBP/NZD exchange rate has finally broken below a key support line that has exposed the Pound to the lowest levels since the mid-1970's against the New Zealand Dollar.

The Pound to New Zealand Dollar exchange rate is seen at 1.7553 at the time of writing, the previous record low for the pair in 2016 was at 1.7613.

At current spot market rates those using New Zealand Dollars to buy Pound Sterling are therefore looking at the best exchange rate to do so since 1975:

While the NZ Dollar retains notable strength, the lion's share of the declines falls at the door of Sterling.

The currency continues to suffer notable declines on confirmation by the UK’s Prime Minister May that Article 50 of the Lisbon Treaty will be triggered before the end of March 2017 which will begin a two-year negotiation process to leave the EU.

While clarity is always welcomed it appears that traders sold GBP on May’s tough stance on the nature of negotiations.

The Government appears keen to make control over EU immigration a red line in negotiations which will likely mean the UK loses access to the European single market.

The freedom of movement of people between members of the single market is a fundamental cornerstone of the agreement.

The imposition of tariffs on UK imports by Europe, and potential loss of financial passporting, would likely have a negative impact on economic growth over coming years.

Details on what the UK will aim for in negotiations remain thin.

May says it won't be a Swiss or Norwegian model (Norway has full single market access; Switzerland access for most industries) but claims, "I want to give British companies the maximum opportunity to trade in and operate in the single market".

"The more limited the access to the single market, the worse for GBP," says Elsa Lignos at RBC Capital Markets.

The Government also said it would introduce a Great Repeal Bill which would remove the 1972 European Communities Act and convert all existing EU legislation into UK law on the day of departure from the bloc.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3521▼ -0.03%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2721 - 2.2815 |

**Independent Specialist | 2.3192 - 2.3286 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

More Losses Forecast

The GBP/NZD pair has nearly completed forming a right angle triangle.

The move higher over the previous week may have formed an ‘e’ wave up, which is normally the last wave in the formation of a triangle:

Right-angled triangles are special in that they provide clues as to the direction of the eventual breakout, which is always in the direction of the flat edge, which in this case would be down.

Such a move would have to break below the base of the pattern and 1.7590 for confirmation, but once below would probably run down to robust support at 1.7485 as an initial target.

A further break below that support level, confirmed by a move below 1.7400, would probably move down to 1.7200 - the minimum price expectation calculated from the height of the triangle pattern.

New Zealand Dollar to Remain Supported

The most recent data from New Zealand showed a rise in Business Confidence which was positive for the economic outlook, however, inflation remains subdued and there is no major change in expectations that the Reserve Bank of New Zealand (RBNZ) are likely to cut interest rates.

These expectations see a cut in November following comments in the RBNZ’s September statement in which they stated the New Zealand dollar (kiwi) was too strong and admitted to the need for further monetary easing.

The kiwi continues to be supported by New Zealand’s higher interest rates, which offer international investors 2.0% and this attracts a lot of foreign capital and therefore demand for the kiwi.

This compares favourably to the UK’s meagre 0.25%, and so favours more kiwi strength and therefore more downside for GBP/NZD.

A November rate cut to weaken the kiwi would slow the decline in GBP/NZD somewhat, however, given the Bank of England (BOE) also likely to cut rates soon, the large difference will probably remain, supporting the kiwi and more downside for the pair.

Hard data for the kiwi in the week ahead includes NZ Business Confidence in Q3 on Monday, Global Dairy Auction prices on Tuesday, October 4. This continues to cap sterling gains.

UK Economy Resilient but Brexit Uncertainty Looms

The UK economy continues to defy pre-referendum predictions that it would weaken substantially on a Brexit vote.

Some relief for GBP was provided on October 3rd with the release of some impressive manufacturing PMI data which showed the sector to be growing at its fastest rate since 2014 having in September posted a joint-record highest reading.

"In the short term the UK economy is benefiting from the current course of events as the lower Pound continues to spur manufacturing demand. Today's UK PMI reading was sharply higher than forecast coming in at 55.4 versus 52.1 projected. Presently, the UK is enjoying the best of both worlds as its firms have full access to the European market but while seeing their exports becomes instantly competitive after the Pounds 15% decline since Brexit vote," says Boris Schlossberg at BK Asset Management.

We await Wednesday's release of Service PMI for further data guidance as this sector accounts for over 80% of all UK economic activity.

Unicredit’s, UK Economist Daniel Vernazza argued, that Friday’s UK Services Output data which resoundingly beat forecasts of 0.1% by rising 0.4% in July, was a strong positive sign for growth since Services Output has a major impact on the economy.

“Services output accounts for almost 80% of GDP and today’s number suggests the UK economy was much stronger than we had initially expected in the immediate aftermath of the vote,” said Vernazza.

Other data released by the Office for National Statistics (ONS) on Friday, revised growth up in Q2 to 0.7%, from 0.6% previously, which is above the long-term average of 0.5-0.6%.

Longer-term the Unicredit economist is sceptical about whether the economy can continue to lay such ‘golden eggs’:

“Today's services output release for July suggests the risks to even our upward-revised forecast are now to the upside, but importantly it’s still early days.

“Looking ahead, we expect the UK economy to slow materially, with GDP growth of 0.2% in 2017, as it faces a lengthy period of heightened uncertainty ahead,” he said.

Indeed, many believe it is not until Article 50 is triggered that Brexit will become an economic reality, with more impact on the economy.

Citibank’s analysis focuses more on Brexit negotiations as a driver of sterling, which it concludes is likely to lead to weakness.

“The current consolidation in sterling is likely to give way to lower levels.

“GBPUSD triggers stops below 1.3000 overnight as the unit remains highly sensitive to UK – EU trade negotiations later this year,” said CIBC.

They also fear a ‘Hard Brexit’ devaluing sterling.

“As time has progressed, the likelihood of a so-called ‘hard-Brexit’ has increased.

“That situation would involve giving up single market access for control over immigration.

“While the Bank of England can’t offset the long-term growth implications of such a scenario, it is increasing the chances that the MPC decides to take rates down to its effective lower bound of 0.10% in the coming months.”

Most analysts still expect a move from the BOE before the end of the year.