ANZ Research still see another RBNZ interest rate cut in 2016, however the timing of the cut has been delayed ensuring the New Zealand dollar should remain buoyant.

The threat of another interest rate cut at the Reserve Bank of New Zealand (RBNZ) hangs like an axe of the the necks of those betting on a stronger kiwi dollar.

A further cut to the 2% OCR would greatly diminish global investor appetite for New Zealand debt products, thereby diminishing demand for the NZD.

The timing of the next cut, which is a given assumption held by all the big-name forecasters we follow, is the only question up for debate.

You can bet that if it were not coming, the NZD would be higher than it currently is.

Last week we had the RBNZ deliver its FSR, and to be honest, it was a disappointment for those who wanted to see decisive actions taken by the RBNZ on the country’s over-heating housing market.

It is the house market that is preventing the RBNZ from cutting interest rates, thereby ensuring the NZD remains expensive by historical standards.

“We still see the OCR heading lower, but further down the track than June; it doesn’t pass the smell test to be upping the ante on housing and pouring petrol on the fire at the same time,” says a client note issued by ANZ Research.

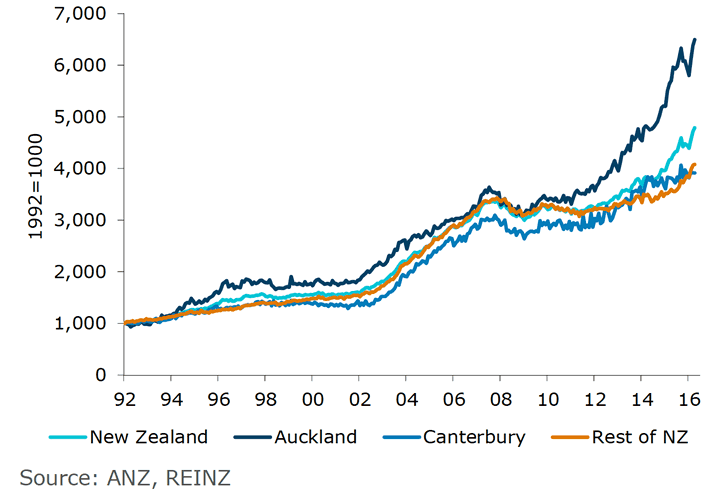

Indeed, ANZ reckon the housing market is once more a run-away train, and strength is now far broader than it has been in the past few years.

The latest April REINZ data showed annual sales growth running in excess of 20% in nine of 12 regions.

It is believed that regional housing markets are now fast approaching the overpriced levels seen in Auckland where house prices are rising again, with the stratified measure up 6% in the past two months alone, and back to all-time highs.

Weaker house price inflation early in the year gave the RBNZ some confidence to surprise the market with a NZD-negative rate cut.

The RBNZ would like lower interest rates to put downward pressure on the currency and to boost inflation which is worryingly low.

Latest Pound / New Zealand Dollar Exchange Rates

| Live: 2.3518▲ + 0.14%12 Month Best:2.3553 |

*Your Bank's Retail Rate

| 2.2719 - 2.2813 |

**Independent Specialist | 2.3189 - 2.3283 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

New Zealand exporters, particularly dairy farmers, could do with a softer dollar to boost demand for their products on the global economy.

However, with the latest data showing a renewed uptick in house price inflation, the central bank wasn’t prepared to deliver another easing in policy as soon as May which suggests the NZ dollar should find some breathing space and arrest the declines seen in the currency over recent weeks.

Indeed, this decline in the NZD is window dressing when compared to the 2016 performance thus far.

For sustained declines in the NZD markets will want to see sustained cuts to interest rates, but cutting interest rates at the central bank is likely to continue pushing house lending costs lower and thus stimulate prices.

The effective mortgage rate is yet to fully reflect previous monetary policy loosening.

“Together with expected further OCR cuts, we estimate there is another circa 35bps of easing still in the pipeline out to the middle of next year,” say ANZ on the prospect of even lower interest rates.

The movement in house prices is however storing up potential problems down the line as debt levels are high and speculative behaviour is clearer to see.

While household debt-servicing burdens are sitting only slightly above average levels given historically low interest rates, the household debt-to-income ratio (162%) is already at all-time highs and rising.

Debt servicing only looks okay because interest rates are so low; it wouldn’t take much to change that via even small movements in rates.

Investors are accounting for a growing share of both new lending and housing sales turnover.

And for the first time that the team at ANZ can recall, the RBNZ is now acknowledging risks stemming from “the high share of new housing lending being undertaken on interest-only terms or at high debt-to-income multiples”.

The share of interest-only lending for new investor and owner-occupied borrowing is over 50% and 30% respectively.

It is therefore a question of when, not if, the RBNZ will implement additional macro-prudential measures targeting the housing market.

While we have learned over the past couple of years that these measures are not the most optimal policy outcome – they are distortionary, their effects are often temporary and they are far less powerful than the RBNZ’s traditional interest rate lever.

The RBNZ looks set to take another crack via prudential means anyway.

All options appear to be on the table, but the way the RBNZ talked about debt-to-income ratios, a limit of that description looks a likely contender.

“We also don’t think we’ll have to wait too long to find out. Something within the next three months wouldn’t surprise us, though it may be a struggle to sell it politically as there will be concern over the impact on first home buyers,” say ANZ.

This will allow for interest rate cuts to be delivered which could dampen demand for the NZD.

ANZ are forecasting the next interest rate cut to be delivered in July.

Outlook for the New Zealand Dollar

It is reluctance to cut interest rates that has seen researchers at BNZ backtrack on their negative-NZD forecasts for 2016 and 2017.

BNZ reckon the New Zealand dollar will continue to fall, but at a slower pace then previously anticipated as more strength than previously anticipated is felt in the market.

The pound to New Zealand dollar exchange rate is expected to appreciate from its current levels at 2.1421 and by June GBP/NZD is forecast to trade at 2.1740.

This is a downgrade on the previously forecast 2.2222 for the same period, a reflection of a solidifying path for the kiwi.

The rate is forecast at 2.2222 in September, with the target lowered from 2.2727.

Local data remains mixed, but at a level that is still NZD-supportive over the short term.

“We expect the NZD/USD to remain range-bound, caught between domestic data that has the market second guessing a June RBNZ cut and prospects for the USD to firm amidst solid data and tame Fed hike expectations at present,” say ANZ.

Analysts say long-term factors suggest strength will be transient.

From a technical perspective we note the NZD to USD exchange rate has broken out of its uptrend and pivotal support at 0.6680-0.6720 is now all that prevents NZD/USD from testing towards 0.65 again.

“A double top has formed just above 0.7050 and markets will be hard pressed to push kiwi through that level,” say ANZ.