- NZD/USD benefits from buy recommendation at HSBC

- In anticipation of a soft USD & possible RBNZ rate rise

- Market prices RBNZ reversal, Westpac tips luxury hike

- Westpac forecasts NZD/USD rally to 0.74 by year-end

Above: RBNZ Governor Adrian Orr. File Image © Pound Sterling, Still Courtesy of RBNZ

- GBP/NZD reference rates at publication:

- Spot: 1.9922

- Bank transfers (indicative guide): 1.9225-1.9364

- Money transfer specialist rates (indicative): 1.9743-1.9822

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

New Zealand’s Dollar could benefit over the coming months from what are increasingly ‘hawkish’ expectations for Reserve Bank of New Zealand (RBNZ) monetary policy, according to HSBC and Westpac, though notably around interest rates which could begin rising as soon as the second quarter next year if investors are correct in how they’ve recently wagered.

Pricing in certain markets has indicated in recent weeks that investors, traders and other participants are becoming ever more optimistic or otherwise cautious on the outlook for borrowing costs in New Zealand, with notable increase in the prevalence of ‘hawkish’ views building since the RBNZ’s May policy decision when for the first time since the onset of the pandemic it presented the market with assumptions about future interest rates.

Included here was the assumption that New Zealand’s 0.25% official cash rate would be lifted to 0.5% in the third-quarter of next year, although since then some market participants and analysts have wagered or otherwise forecast that lift-off could come even sooner than that.

The New Zealand Dollar has been slow to close the performance gap between itself and other currencies which have also benefited in recent months from optimism, or simply a lesser sense of caution at their respective central banks, leading it to catch the eye of analysts at HSBC.

“The oversized USD reaction to an incremental shift in guidance and tone from the Fed is likely to reverse in the coming weeks, barring a persistent run of upside US activity surprises or ongoing hawkish Fed commentary,” says Paul Mackel, global head of FX research in a recent briefing to clients.

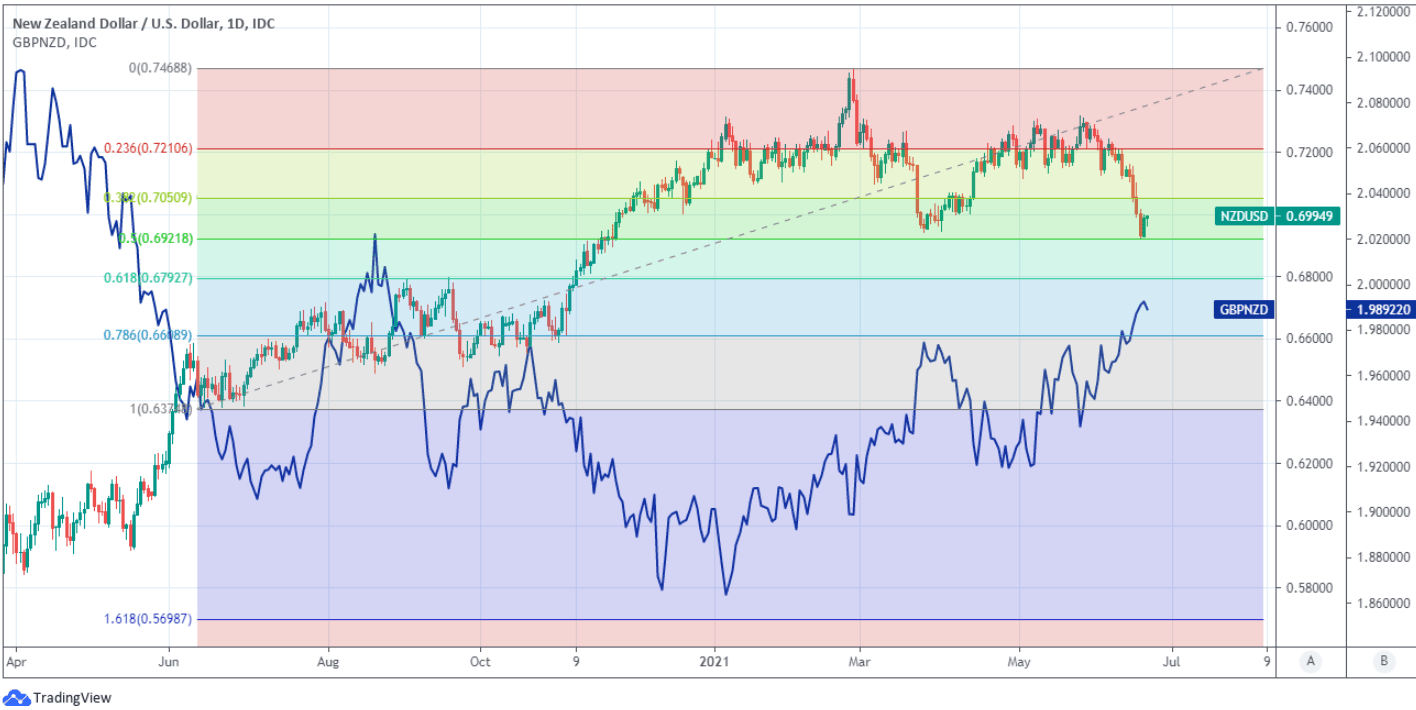

Above: NZD/USD shown at daily intervals with Fibonacci retracements of June 2020 rally and GBP/NZD.

“We believe the best avenue to play a USD reversal weaker is against the NZD. The latter currency now looks cheap relative to the hawkish shift in rate expectations seen so far this year. In other words, while the RBNZ is clearly hawkish, it is not so clear that this is priced into the currency,” Mackel says.

Mackel and the HSBC team advocated this week that clients of the bank buy NZD/USD around 0.6970 and look for a move up to 0.7290 in the weeks or months ahead, citing the RBNZ’s evolving stance and house forecasts which look for the nascent bout of strength in U.S. Dollar exchange rates to reverse in the absence of comment from the Federal Reserve (Fed) to validate the market response to last week’s policy decision.

That saw a majority of the Fed’s rate setters indicate that they now individually expect to vote to lift U.S. rates before the end of 2023 and with a substantial minority on the Federal Open Market Committee even seeing a potential case for a move as soon as next year, although Chair Powell played down the significance of that so-called dot-plot of projections in a press conference after the announcement while barely evolving if-at-all the Fed’s guidance in relation to its $120bn per month quantitative easing programme.

“We look for USD weakness in the coming month. The marked response of the USD to the FOMC was most likely a position squeeze, as reflected in our USD speculative flow data. We expect a still patient tone from the Fed to counter the hawkish reflex of the market,” Mackel says.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Much about the immediate outlook depends Tuesday on if the market was right to view last Wednesday’s update as meaning that upside risks to the Fed’s 2% average inflation target are becoming sufficient to warrant the kinds of interest rate rises placed on the table through the Fed’s dot-plot, although in the event of any renewed decline by the U.S. Dollar; the Kiwi could be among the most likely to benefit from it.

In addition, much about the outlook for RBNZ interest policy and its resulting influence on the Kiwi Dollar is hinged upon whether the New Zealand economy can recover strongly enough to lift inflation back above the 2% midpoint of the bank’s 1%-to-3% target with enough gusto for that target to be sustainably delivered over the coming years, although the Westpac research team has a slightly different view.

“We now expect the Reserve Bank to start increasing the OCR from August 2022,” says Michael Gordon, chief New Zealand economist at Westpac in a Monday research briefing.

“Previously we expected interest rate hikes to be delayed until early 2024. However, with signs of solid momentum in domestic demand, we’re now more confident that the economy can withstand a gradual normalisation of monetary policy settings,” Gordon adds.

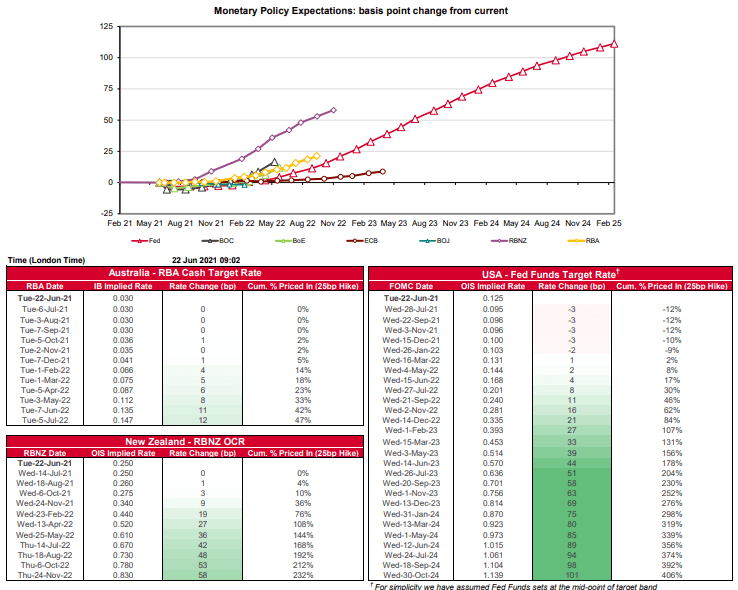

Above: Westpac data sheet showing overnight-indexed-swap (OIS) market expectations for RBNZ, RBA and Fed interest rates.

Gordon and the Westpac team’s view is notable in any case but especially so in this instance because the bank said on Monday that “our change of call is not motivated by inflation concerns,” when lifting its forecasts to take account of their new expectation that New Zealand’s interest rates will rise next year rather than in three-years time.

For readers’ background, it’s inflation which central banks are seeking to manage when they tinker with interest rates and other tools like quantitative easing programmes, and it’s a central bank’s perception that rising inflation is at risk of becoming a problem which typically leads rate setters to begin lifting borrowing costs.

However, Westpac sees a rising chance of the RBNZ lifting its cash rate slightly next year even if Kiwi inflation pressures are still well contained: This would be the RBNZ reloading its monetary policy cannon by lifting the cash rate - after having cut it to a record low and close to zero - simply in order to ensure that it’s able to then reduce borrowing costs again at a later date and in the event of another crisis.

Ordinarily central banks might be unlikely to take such a course of action, although with governments across the world including in New Zealand still spending large percentages of GDP on fiscal support programmes, it’s possible that some including the RBNZ could choose to do exactly this if they see government efforts as sufficient to ward off any adverse impacts of such action.

“We think that the RBNZ has time on its side to deal with inflationary pressures,” says Gordon, who’s foreign exchange research colleagues forecast an NZD/USD rally to 0.74 by year-end. “We see little evidence that the economy is overheating. Activity is still running below its full potential, although the gap is closing.”