Above: RBNZ Governor Adrian Orr. File Image © Pound Sterling, Still Courtesy of RBNZ

- NZD bottom of pack after RBNZ hikes capital requirements for NZ banks.

- But long-awaited decision is silver-lined, less onerous than expected.

- Banks given seven years, not five, to meet new regulatory requirements.

- Only one RBNZ rate cut necessary to soften blow to economy says ANZ.

- Market eyes less RBNZ cuts, implied probability of June 2020 cut @ 50%.

- Westpac tips more NZD, GBP gains Vs USD amid lofty GBP/NZD rates.

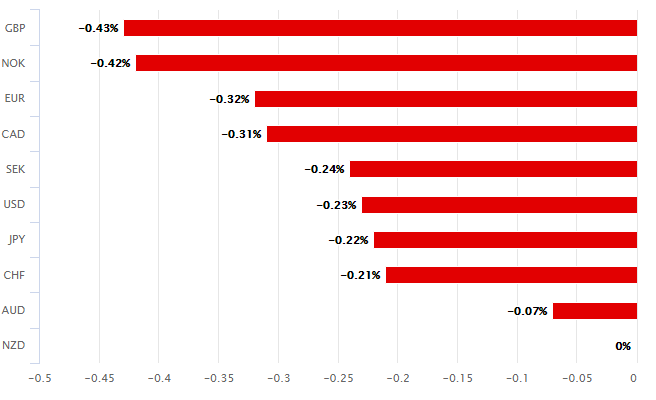

The New Zealand Dollar ceded ground to all major rivals Thursday even after a long-awaited Reserve Bank of New Zealand (RBNZ) decision on new regulatory capital requirements came out on the softer side of expectations.

RBNZ Governor Adrian Orr said Thursday that Kiwi banks will need to keep more capital in reserve for rainy days than at any other point in the past.

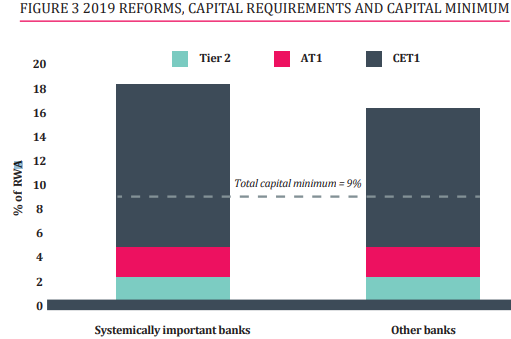

The bank decided that lenders of all stripes will need to hold more than the current 10.5% of ‘risk-weighted-assets’ (RWA) in reserve from July 01, 2020, with New Zealand’s four largest firms being required to lift that number to 18% while smaller outfits will only need to go as far as 16%. These are “total capital” levels, with the exact amount to be split between ‘tier 1’ and ‘additional tier 1’ capital as well as ‘tier 2’ capital.

“While the changes announced today are broadly in line with expectations and commentary provided by the Major Banks with their recent earnings releases, they are supportive compared to the original release and remove further downside risk,” says Brendon Cooper, head of credit and ABS strategy at Westpac, one of the four larger banks affected by the review.

Above: New Zealand Dollar performance Vs major rivals Thursday. Source: Pound Sterling Live.

Decisions unveiled in the ‘capital review’ will still require Kiwi lenders to raise large amounts of new money that will spend its existence parked on the sidelines of balance sheets rather than being deployed for any meaningful revenue generating purpose. And they could yet deprive the economy of much-needed finance for commercial activity however, the new requirements are also less onerous in some ways than many had expected.

The RBNZ had suggested lenders would have only five years to meet the new requirements, which are typically phased in incrementally over time, but has actually given them seven. It had also, at times in the two-year review of existing rules, suggested it could make other onerous changes to the composition of reserve buffers that would have required firms to raise more money through a lesser number of channels.

“Importantly, the definition and amount of allowable Tier-1 capital has been expanded from the original proposals,” says Sharon Zollner, chief economist at ANZ, another of the four larger lenders impacted by the decisions. “We expect a larger impact on both retail interest rates (30-60bp, spread unevenly by sector and subject to considerable uncertainty) and credit availability than the RBNZ does, and therefore more of a negative impact on GDP. However, any impact will be difficult to separately identify, since it will occur over a long time period where many other offsetting forces will be at play.”

Above: Total capital buffers required by small and large banks, broken down according to composition.

Some concerns about the decision had centred on whether firms would be able to call redeemable preference shares ‘tier 1 capital’ - the foundation stone of all ‘capital buffers’ that is meant to be comprised of the highest quality equity. Preference shares are a hybrid form of equity and debt because they have characteristics of both, although the RBNZ has said Kiwi lenders can use preference shares equal to 2.5% of total RWA to help meet the new requirement for tier 1 capital. Raising money through the sale of preference shares can be easier than doing so through regular shares and is not as contentious with regular shareholders as the sale of new voting rights in the company.

However, most of the Kiwi Dollar’s concerns about Thursday’s decision were centred upon the likely impact on the RBNZ’s cash rate. The Kiwi economy has, after all, slowed notably while already mired in a multi-year period of disinflation. That’s already compelled the RBNZ to cut interest rates three times this year, although on November 04 it left the cash rate at 1% which prompted investors to reassess their assumptions about when the next cut is likely to come.

“We continue to see a lower OCR in time and these changes will contribute to that, though less than previously expected. A softening of the proposals, combined with a more positive domestic outlook (and in particular upside to government infrastructure spending), mean we are changing our OCR call to only one further 25bp OCR cut in May next year, taking the OCR to 0.75%. We will review once we have more detail in the fiscal update,” says ANZ’s Zollner.

Above: Pound-to-Kiwi rate shown hourly intervals.

Pricing in the overnight-index-swap market implied on Thursday, June 24, 2020 cash rate of 0.88%, up from 0.87% in the prior session. The implied interest rate for the mid-way mark next year is also sat around the half-way point between the current cash rate and the 0.75% that would prevail in the wake of another standard 25 basis point cut. The RBNZ is trying to lift growth and inflation, which have fallen further amid the U.S.-China trade war and low business confidence at home, by lowering borrowing costs for companies and households.

The longer phase-in for the new rules and the modest increase in OIS-implied cash rates for next year might have helped temper the Kiwi’s losses on Thursday. The currency was down against all major rivals although its largest intraday loss was 0.5% and came against a strengthening Pound Sterling.

“Near-term momentum remains positive. NZ fundamentals continue to beat expectations. Next week’s half-year fiscal update should be stimulatory,” says Imre Speizer, an Auckland-based FX strategist at Westpac. “NZD/USD retains upward momentum, chartists targeting 0.6700 multi-week.”

Speizer and the Westpac team are eyeing the prospect of further gain for the Kiwi into year-end, with the NZ government budget update next week seen as likely to provide additional support to the antipodean currency. Financial markets are hopeful that government’s around the globe will step up their fiscal expenditures in the months ahead, which would be positive for currencies because more government spending could potentially mean less interest rate cuts from the central banks.

Above: NZD/USD rate shown daily intervals.

The Kiwi’s upside against Sterling, which is rising amid mounting hopes that Prime Minister Boris Johnson will secure a majority in the December 12 general election, could be quite limited. A Johnson victory might see the UK move forward on Brexit and would certainly bar an increasingly radical opposition Labour Party from 10 Downing Street for up to five more years.

“GBP/USD’s push above 1.3000 reflects the potential of a Conservative majority and suggests a 1.30-1.34 range into the election if polls remain at current levels,” says Tim Riddell, a London-based strategist at Westpac.

A GBP/USD rate of 1.34 and an NZD/USD rate of 0.6700 would produce a Pound-to-New-Zealand-Dollar rate of 2.0, which is around 92 points below Thursday’s level. Sterling has risen sharply in recent weeks in accordance with polls that have often in the past turned out to be, at best, unreliable.

The Pound-to-New-Zealand-Dollar is a 'cross rate' that can be calculated at a basic level by dividing GBP/USD over NZD/USD, which means both the latter rates can impact on the trajectory of Sterling relative to the Kiwi unit.

December's election is front and centre for the British currency, which is tipped to react positively upon a Conservative majority next Thursday, negatively upon a Labour Party win and also negatively in response to another hung parliament.

"GBP/USD is approaching its 5 year downtrend at 1.3156. Also found in this vicinity is the 50% retracement of the move down from 2018 at 1.3167 and the 1.3187 May high and this is tough resistance and we look for the market to fail here," says Karen Jones, head of technical analysis at Commerzbank.

Above: Pound-to-Kiwi rate shown weekly intervals.

Time to move your money? The Global Reach Best Exchange Rate Guarantee offers you competitive rates and maximises your currency transfer. Global Reach can offer great rates, tailored transfers, and market insight to help you choose the best times for you to trade. Speaking to a currency specialist helps you to capitalise on positive market shifts and make the most of your money. Find out more here.

* Advertisement