- Rise in wholesale prices supports Rupee against the Pound at start of week

- INR steadies after losses from trade data on Friday

- Pound at risk of volatility from Brexit politics and three major data releases

Image © Ash T Productions, Adobe Stock

The Pound-to-Rupee's short-term uptrend lost its momentum on Monday morning after higher-than-expected wholesale inflation data supported the Rupee side of the pair.

The data broke a rise which started last Friday after poor Indian trade data weighed on the Rupee.

The Rupee has been supported by relatively strong inflation data which prompted the Reserve Bank of India (RBI) to raise interest rates in June and could lead to further rate hikes in the future.

Higher interest rates tend to appreciate a currency by attracting greater inflows of foreign capital, drawn by the promise of higher returns.

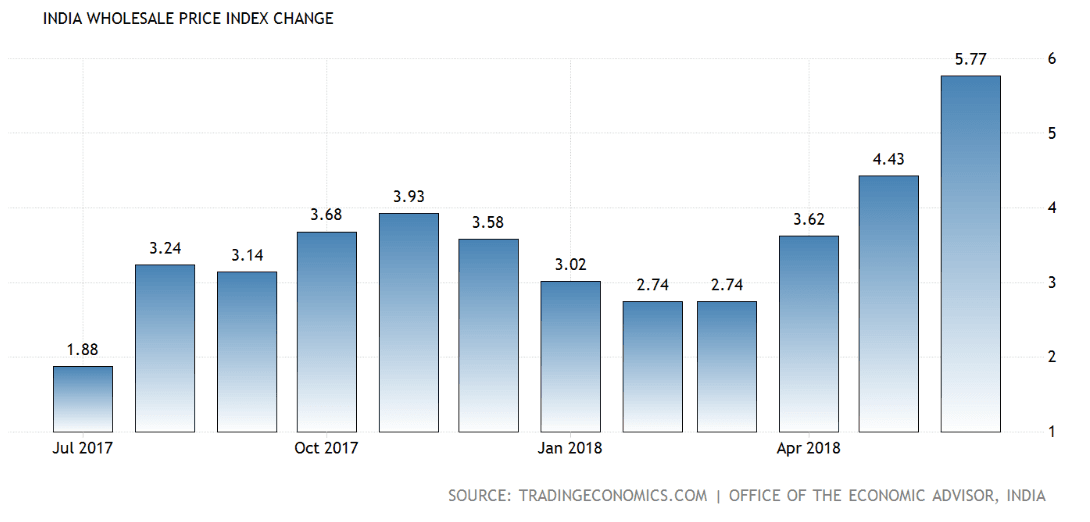

Wholesale prices showed a 5.77% rise in June according to data out on Monday morning and this is likely to pass through into higher consumer prices in the future.

(Image courtesy of Tradingeconomics.com)

India's June trade deficit widened to -$16.6bn from -$14.62bn in May, a 5 year high, mostly on the back of the effects of higher oil prices.

Oil accounts for roughly a quarter of all of India's imports so fluctuations in the price of the commodity heavily impact on supply and demand for the Rupee.

Although the price of oil has fallen of late which should help ease the deficit in the future the impact will take time to filter through as much forward-buying of oil means actual changes in price take time to filter through.

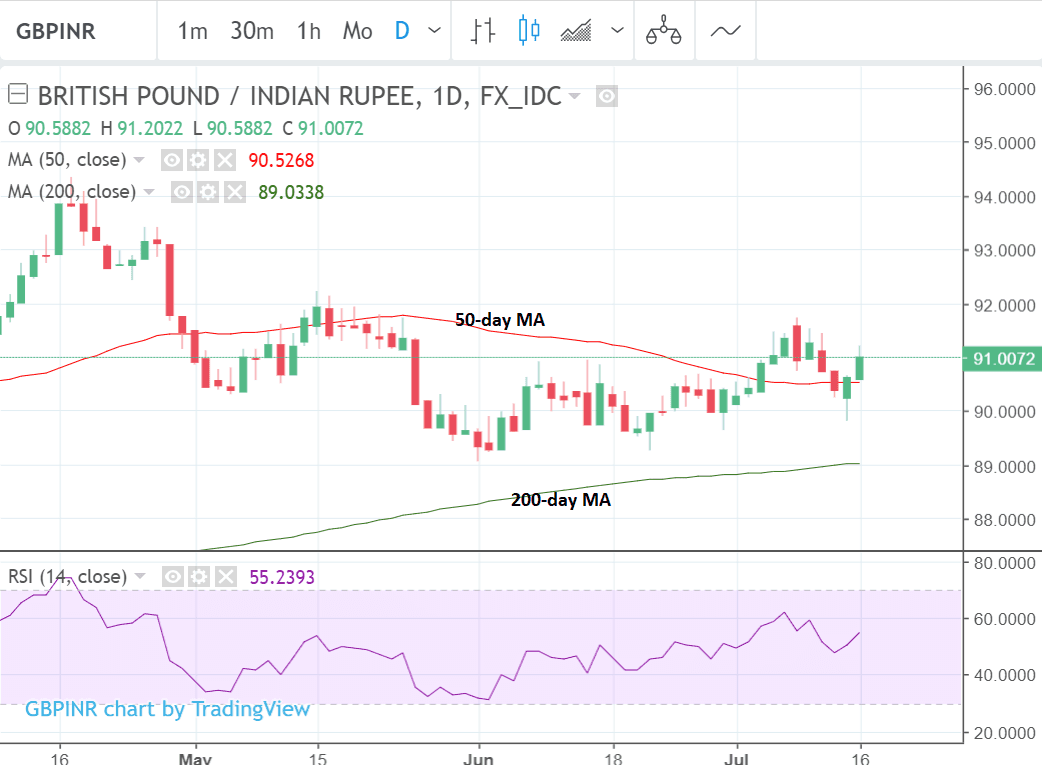

From a technical perspective the mixed data reflects the sideways, rangebound, nature of the charts.

The daily chart, for example, shows the pair in a fairly well-established sideways trend between 89 and 92 Rupees to the Pound.

It could be argued that bulls have a slight advantage on the daily chart because of the position of the major moving averages, especially the 200-day MA at 89.

The location of the large MA should act as an obstacle preventing lower prices.

Momentum is also fairly strong which suggests more upside. RSI is at a higher level currently than it was back in May when the exchange rate was up in the 92s.

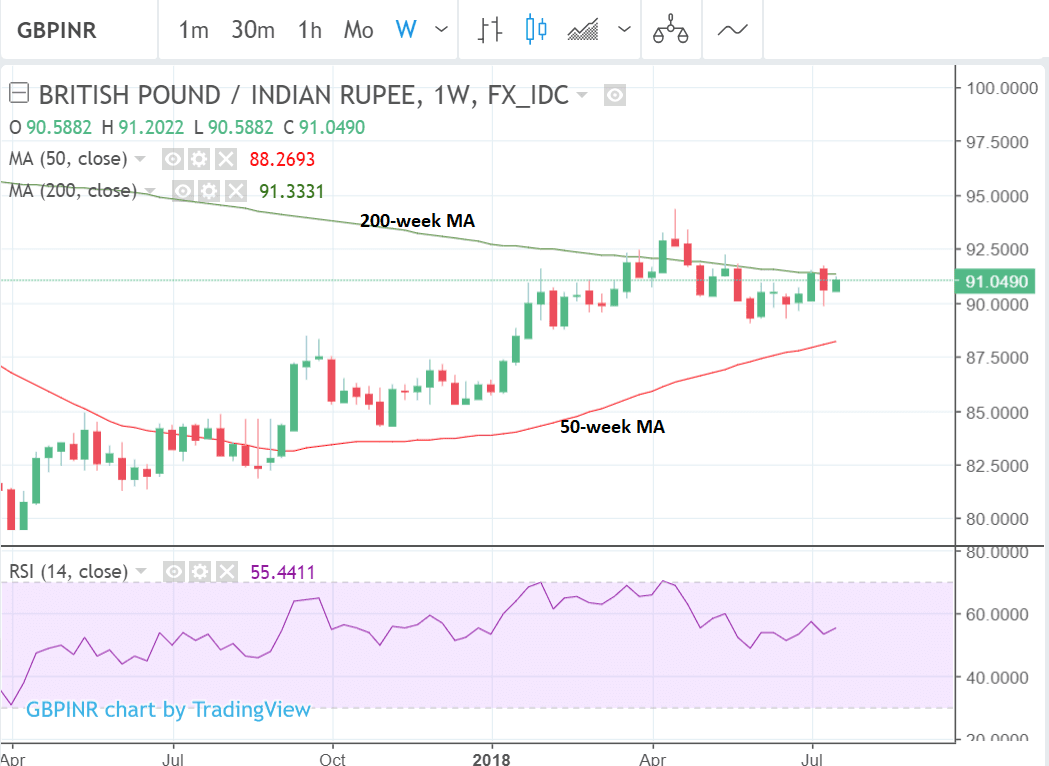

Yet the slight bullish tenor of the daily chart does not extend to the weekly chart, where the 200-week MA is just above prices at 91.33 and therefore capping further upside.

Given both up and downside are thus neatly bordered by the MAs we forecast a probable continuation of the current range-bound market, at least from a technical POV.

From a fundamental viewpoint much depends on the price of oil which although it has lost a lot of ground of late and may be reversing trend lower, remains relatively elevated.

Inflation in India continues to rise strongly which is a bullish factor for INR. Not just inflation from fuel and food but rather Core inflation appears to be one of the main drivers, which is positive for the currency as it suggests it is linked to economic growth and the RBI will continue to hike rates.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

Sterling to Provide Volatility for GBP/INR this Week

In the UK the week ahead promises to be marked by a considerable amount of event risk.

A considerable bundle of data and key political events pepper the calendar.

On the political front there will be votes on amendments to the Trade and Customs Bill, which help form the basis of the government's new 'softer' Brexit proposal. These are expected to take place on Monday 16 and Tuesday 17.

They could be critical in gauging whether the plan has a likelihood of success and implementation.

"Another legislative showdown takes place in the UK House of Commons as the Trade and Customs Bills are voted on. Amendments to the bill have come from 'hard' Brexiteers (trying to undo the white paper) and Remainers (trying to bind the UK to a customs union). Some of these votes could come down to the wire, and have significant implications for Brexit negotiations," say Actionforex in their week ahead analysis.

Sterling may catch a bid if Brexit supporters in the Conservative party fail in their upcoming attempt to harden the UK government's plan on leaving the EU, as failure should increase the GBP-positive probability of a relatively soft Brexit.

We note a string of opinion polls out over recent days that shows support for the Conservatives has fallen below that of Labour with a good proportion of voters flocking back to UKIP having judged that May will not deliver the Brexit they desire.

This will remind Conservative lawmakers that bringing down the government will likely throw their party onto the opposition benches. It does also however offer the potential to sharpen the determination of Brexiteers who believe their electoral success will lie with delivering a clean 'hard' Brexit.

From a 'hard' data perspective the week has three major, potentially market moving, releases too: labour market data on Tuesday, CPI on Wednesday and retail sales on Thursday - all are at 9.30 UK time (8.30 GMT).

Their significance is further heightened by the fact that they may impact on the decision-making of the Bank of England (BOE) when it has its pivotal meeting in August. Because the probabilities of a hike or not, are so evenly balanced, next week's data could prove critical in swinging the vote one way or another.

Labour market data for May, is expected to show continued improvement with a 150K rise in employment on a three-month-on-three-month basis.

The more important wage data component of the release, which is more of an influence on inflation and therefore Bank of England decision-making, is expected to show only modest rises of 2.6% for headline and 2.8% (including bonuses).

Stronger wage rises are necessary to increase the chances of a rate hike and a disappointment could weigh heavily on Sterling.

CPI inflation data in June, out on Wednesday, is likely to show a rise due to the temporary influence of higher oil prices, however, if the main driver is in fact only fuel prices, it is unlikely to have much impact on the Bank of England who are more likely to look through inflation from temporary factors.

Therefore we believe the core CPI reading will be of more interest to the Bank of England as it shows the underlying inflationary pressures present in the economy.

Core CPI is forecast to read at 2.1% (month-on-month) while headline CPI is forecast to read at 0.2% month-on-month and 2.6% year-on-year.

"We suspect that CPI inflation edged up to 2.6% in June, owing to a rise in energy prices. But this should not mark the start of a sustained rise," says Andrew Wishart, UK economist at Capital Economics.

Retail sales for June are set for release on Thursday but the "evidence on strength," says Capital Economic's Wishart, "has been decidedly mixed."

On the one hand, the strong data in April and May will be a hard act to follow in June, yet on the other hand factors such as the good weather and the World Cup could support a rise.

"More sunshine, warm weather, and World Cup should be supportive. Our base case 0.4% forecast leaves a very strong trend for Q2 sales, and a solid hand-off to Q3," says TD securities in their note on data in the week ahead.

Markets are forecasting a reading of 0.4% on a month-on-month basis and 3.9% annualised.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here