Image © Adobe Images

Pound Sterling was higher on the day it was reported headline UK CPI inflation was lower in August than in July, suggesting the peak in price rises might have now passed.

This would be a positive development for the UK economic outlook, and by extension, the Pound.

But the Bank of England's September 22 decision looms large and whether they opt for a sizeable 75bp hike or a smaller 50bp hike could ultimately decide where Sterling ends September.

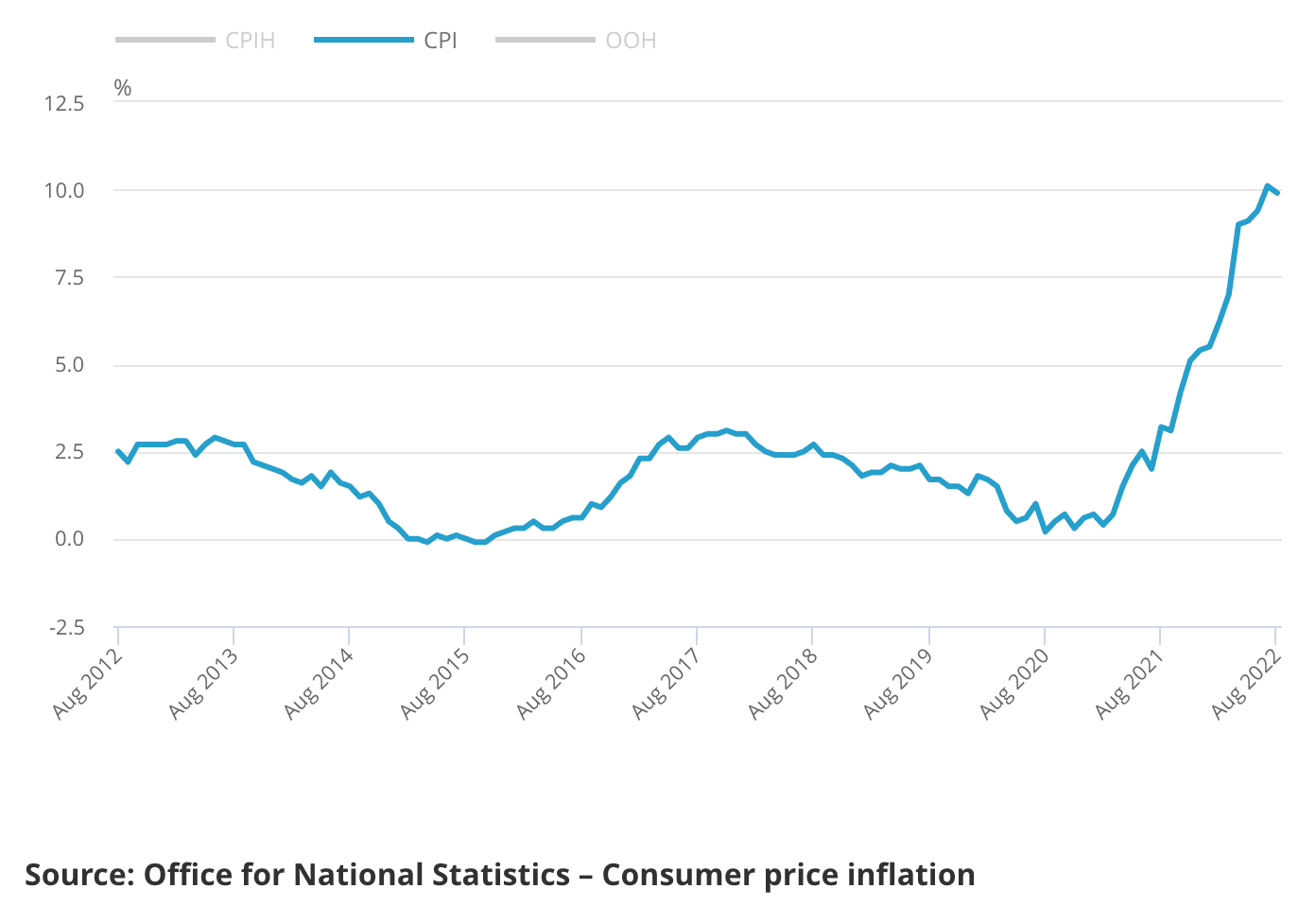

UK CPI read at 9.9% year-on-year in August said the ONS, down from July's 10.1% peak and below the analyst expectation for 10.2%. Inflation rose 0.5% month-on-month in August, coming in below the 0.6% market's expected and July's 0.6% rise.

Core CPI inflation - which strips out externally influenced measures of prices such as fuel - was however higher than in July (6.2%) at 6.3% year-on-year which will remind the Bank of England it faces a hard slog with regards to getting inflation back down to the 2.0% target.

The market is looking for a 75 basis point hike from the Bank, which it must deliver in order to keep Pound exchange rates steady, at least according to analysts at some major investment banks.

If the Bank of England disappoints with a smarll hike the Pound would fall.

While the Pound's initial reaction to the inflation data was to go lower it has since turned and gone higher: the Pound to Euro exchange rate dipped to 1.1521 but is now back to 1.1546, the Pound to Dollar exchange rate fell to 1.1495 but is now back to 1.1546.

Is falling inflation therefore good for the Pound?

It could well be in so far as it raises real yields: i.e. the yield paid by UK monetary assets such as sovereign gilts looks a little more attractive when inflation is not diminishing its value.

From a fundamental perspective, peak inflation implies the cost of living crisis will start improving which is good for consumers and businesses and the economic outlook.

A strong economy commands a strong currency and therefore falling inflation is supportive in a cost of living crisis.

But the complication for the Pound near-term will be the Bank of England's response to the data: the Bank has consistently shown itself to be a reluctant hiker and therefore today's softer-than-expected inflation reading could result in the Monetary Policy Committee reverting to their 'dovish' tendencies and opting to surprise the market with a smaller 50bp rise.

This could weigh on the Pound, as was the case at previous 'dovish' Bank of England decisions.

"With most sell-side economists sympathetic to the 50bp argument, today’s data has done little to impact the pound prior to money markets reopening. While a potential dovish repricing in the September OIS contract may weigh on the pound this morning, we think GBP price action will be determined more by the fallout from yesterday’s US CPI report once US markets open this afternoon," says Simon Harvey, Head of FX Analysis at Monex Europe.

The Pound dropped sharply against the Dollar on Tuesday after U.S. inflation data beat expectations and lead money markets to start betting the Federal Reserve would hike by a massive 100bp next week.

This lead a significant stock market selloff that typically benefits the Dollar and Euro against the Pound.

The repercussions of the U.S. data on broader markets could therefore be more important to Sterling trade over coming days. Mid-week sees markets finding their feet again following Tuesday's sell-off and this could also be providing support for Sterling. Those looking to protect their foreign exchange purchasing power could consider locking in current levels for a future payment, if they fear another slump. Find out more here.

The Bank of England nevertheless looms large from an idiosynchratic perspective and members of the MPC will be poring over Wednesday's data release.

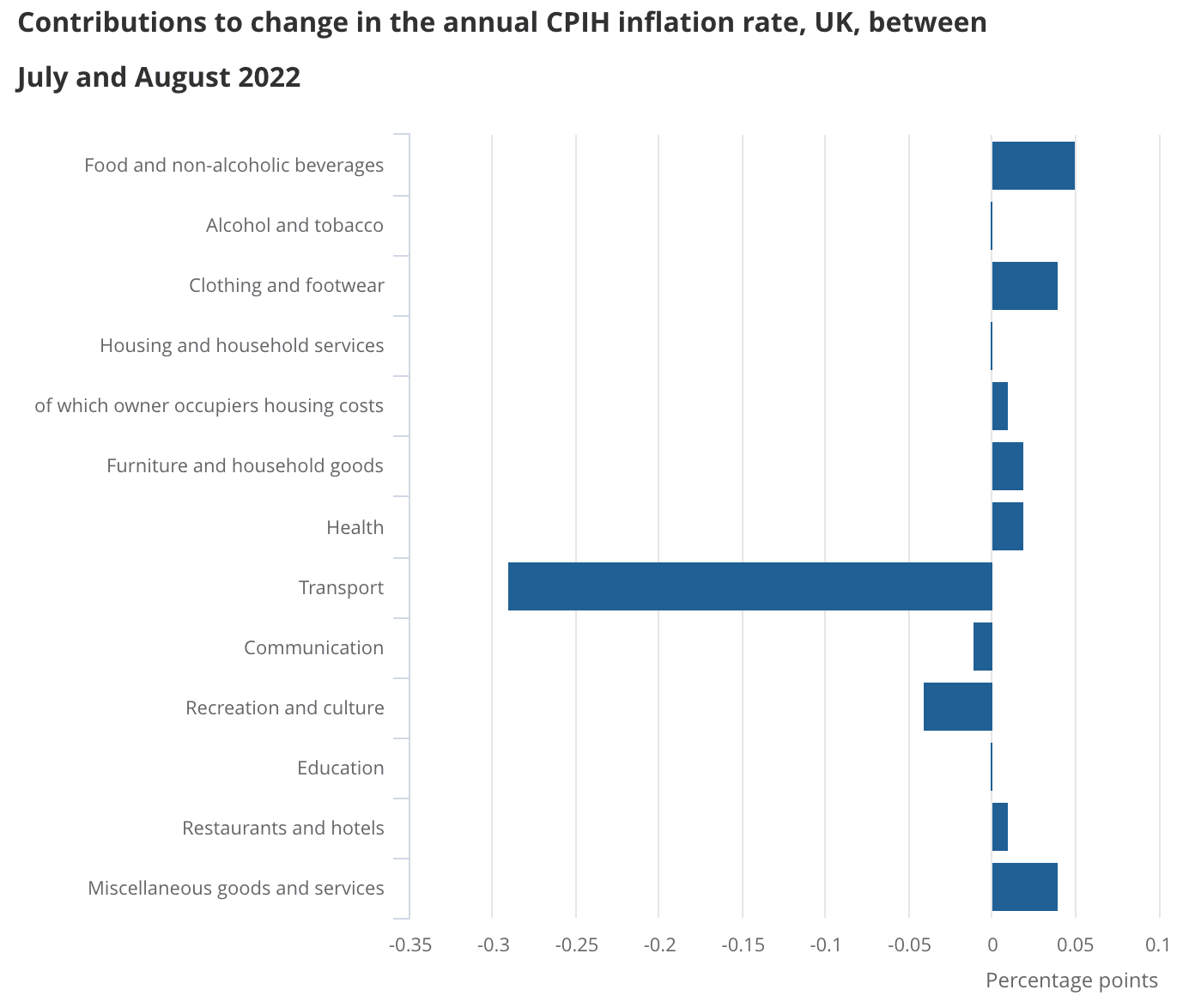

According to the ONS the largest downside drag to inflation was fuel, understandably so given the fall in global oil prices over recent months has pulled down prices at the UK's forecourts.

Above: Inflation was dragged lower by falling fuel prices but prices were up in most categories.

However, as the above shows the breadth of price rises remains large which suggests inflationary pressures are growing right across the price basket.

This will help those members of the Bank's MPC to argue for a 75bp rise, which would arguably support the Pound.

Looking ahead, the peak in inflation might have passed in July thanks to the government's recent decision to cap household energy bills.

But of concern to the Bank of England will be how 'embedded' inflation expectations have become, i.e. are firms going to pursue higher prices and will workers pursue higher wage settlements?

Therefore although the peak might be in, inflation could prove itself stubborn.

Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics, says he anticipates the peak in UK inflation to come in October.

"Looking ahead, we think that the headline rate of CPI inflation will rise to almost 11% in October, driven by a 1.0pp increase in the contribution from electricity and natural gas prices. The latter will rise by only 27% month-to-month in October, far less than the 80% increase announced by Ofgem last month, following the new PM’s intervention last week," says Tombs.

Pantheon Economics are meanwhile "increasingly confident that October’s rate of CPI inflation will prove to be the peak and that it will ease rapidly in 2023, perhaps even all the way back to the 2% target by the end of the year".

"This relatively benign medium-term outlook for CPI inflation should convince the MPC that they do not need to strangle the economy by raising Bank Rate all the way to 4%, as markets currently anticipate," says Tombs.