"The consequences for GBP would be disastrous in this darker scenario, with levels like parity for GBPUSD up for discussion" - Credit Suisse.

Image © Adobe Images

The Bank of England is not doing enough to defend the Pound and risks turning it into an "Emerging Market basket case" according to new research.

Shahab Jalinoos, Head of Global FX Strategy at Credit Suisse, says the UK needs a higher interest rate environment if it is to attract enough foreign investor capital to support the Pound.

He finds the Bank's apparent unwillingness to aggressively pursue higher interest rates is proving a key headwind to the UK currency.

"In theory, a country like the UK with a large current account deficit looking to 'dissave' further through a much larger fiscal deficit will need a lot of foreign capital to plug resulting holes in the balance of payments. The easiest source of this should be 'hot money' flows attracted simply by high UK rates," says Jalinoos.

"But that probably needs the BoE to play its part by actually hiking rates materially as the market is pricing in," he adds.

But hopes for 'material' action at September 15's Monetary Policy Committee (MPC) meeting were dealt a blow Wednesday when members of the MPC suggested they were in no mood to act aggressively.

"I judged that the more gradual pace of tightening will allow us to reduce those risks, because we will see the effects of the data and we can always stop," said MPC member Silvana Tenreyro. "So it's about going slowly when there is a lot of uncertainty. And that was my judgement."

Tenreyro was addressing Parliament's Treasury Select Committee in a midweek appearance made alongside Governor Andrew Bailey and the Bank's Chief Economist Huw Pill.

Following the testimony money market pricing showed the odds of a 75 basis point hike next week have fallen to 55%, from 71% earlier in the day.

The Pound tracked these expectations and was sharply lower.

"We have seen another botched effort from the Bank of England today. They had one job which was to talk up the Pound and instead their waffling sees it at US $1.1425," says Shaun Richards, an independent economist who advises UK pension and investment funds.

The Pound to Euro exchange rate (GBP/EUR) fell two-thirds of a percent on day to 1.1560, the Pound to Dollar exchange rate (GBP/USD) was down by a similar amount to 1.1440.

The lack of a 'whatever it takes' narrative on dealing with inflation has been adopted by the Federal Reserve and is contributing to the Dollar's ongoing rise.

To be sure, some members of the MPC such as Catherine Mann, are arguing for the kind of hike required to defend Sterling, but she remains in the minority.

Indeed, the Bank of England continues to prove a 'reluctant' hiker, perhaps a hangover from a past era when their role was to boost the economy by cutting interest rates, print money and sound 'dovish'.

Bailey told the Treasury Select Committee that the crux of the UK's current inflation crisis was external in nature and that the Bank would consider the new Government's fiscal plans when shaping the September 15 decision.

Pill said he believes the incoming government's plans would, on net, push inflation down.

These two influential members of the MPC are not sending the signals consistent with a 75bp hike.

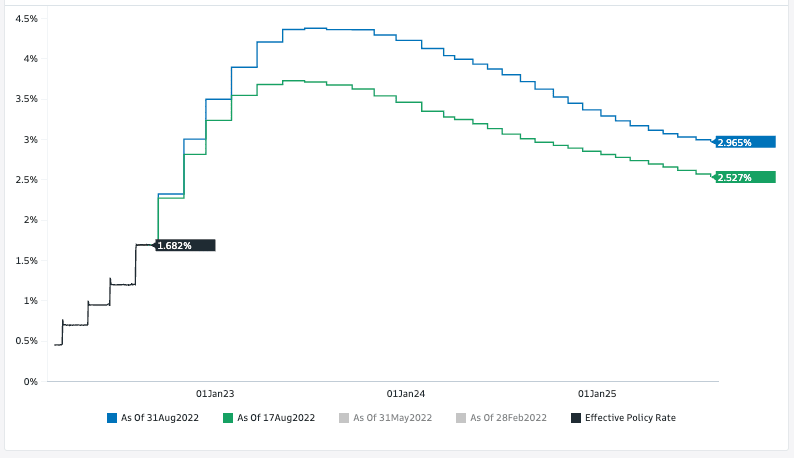

Above: This is what the market is expecting the Bank of England to deliver. Expect the curve to move lower following Wednesday's BoE communications.

The implications for the Pound's outlook from a flat-footed Bank of England are significant, according to Credit Suisse.

"If the BoE shows weakness for any reason (a dovish bias or concern about political attacks), the situation could rapidly shift into a classic EM basket case story where inflation stays high due to both fiscal policy designed to subsidise consumption and monetary policy that is too accommodative," says Jalinoos.

"This not only would fail to attract foreign money, it could even lead to an exodus of UK money too. The consequences for GBP would be disastrous in this darker scenario, with levels like parity for GBPUSD up for discussion," he says.

Research from HSBC meanwhile finds Bank of England policy expectations have become more important for Pound exchange rates than has been the case in the recent past.

"GBP has been heavily influenced by broader risk appetite this year... the relationships between cable and a range of other variables, with equity movements generally the dominant driver of GBP. But the impact of rate differentials has actually jumped above that of risk appetite. This should make the Bank of England’s hike path from here more important," says strategist Dominic Bunning at HSBC.

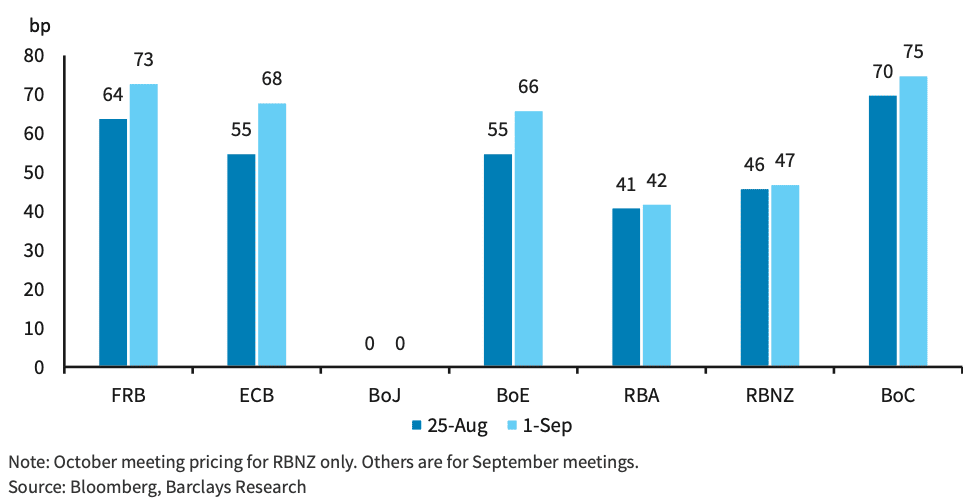

Above: Money market expectations for the size of various central bank hikes in September. Once again it appears the BoE will be the only one to disappoint. Image courtesy of Barclays.

With this in mind, HSBC finds Bank of England policy and communication has become an outright drag on the currency.

HSBC says the Bank of England has been too slow in its quest to challenge inflation by raising interest rates (specifically, market expectations show investors have consistently expected more than the Bank has actually delivered in terms of rate hikes).

"The FX market is getting tired of waiting for the BoE to actually deliver something more hawkish," says Bunning. "The BoE has, at best, met market expectations for hikes, and has actually under-delivered more than over-delivered, pushing GBP lower."

Looking forward, Credit Suisse's Jalinoos says it is time for the Bank of England to step forward and defend the Pound.

"If the BoE plays its part and hikes as the market demands, a stronger GBP should arise, creating a “virtuous circle” in terms of fighting inflation too," he says.

Credit Suisse now forecast a fall to 1.1250 in GBP/USD going forward.

They forecast a rise in EUR/GBP to 0.8700 on account of "ECB hawkishness and UK economic malaise."

This translates into a GBP/EUR forecast for 1.15.