- BoE has a desire to support Sterling

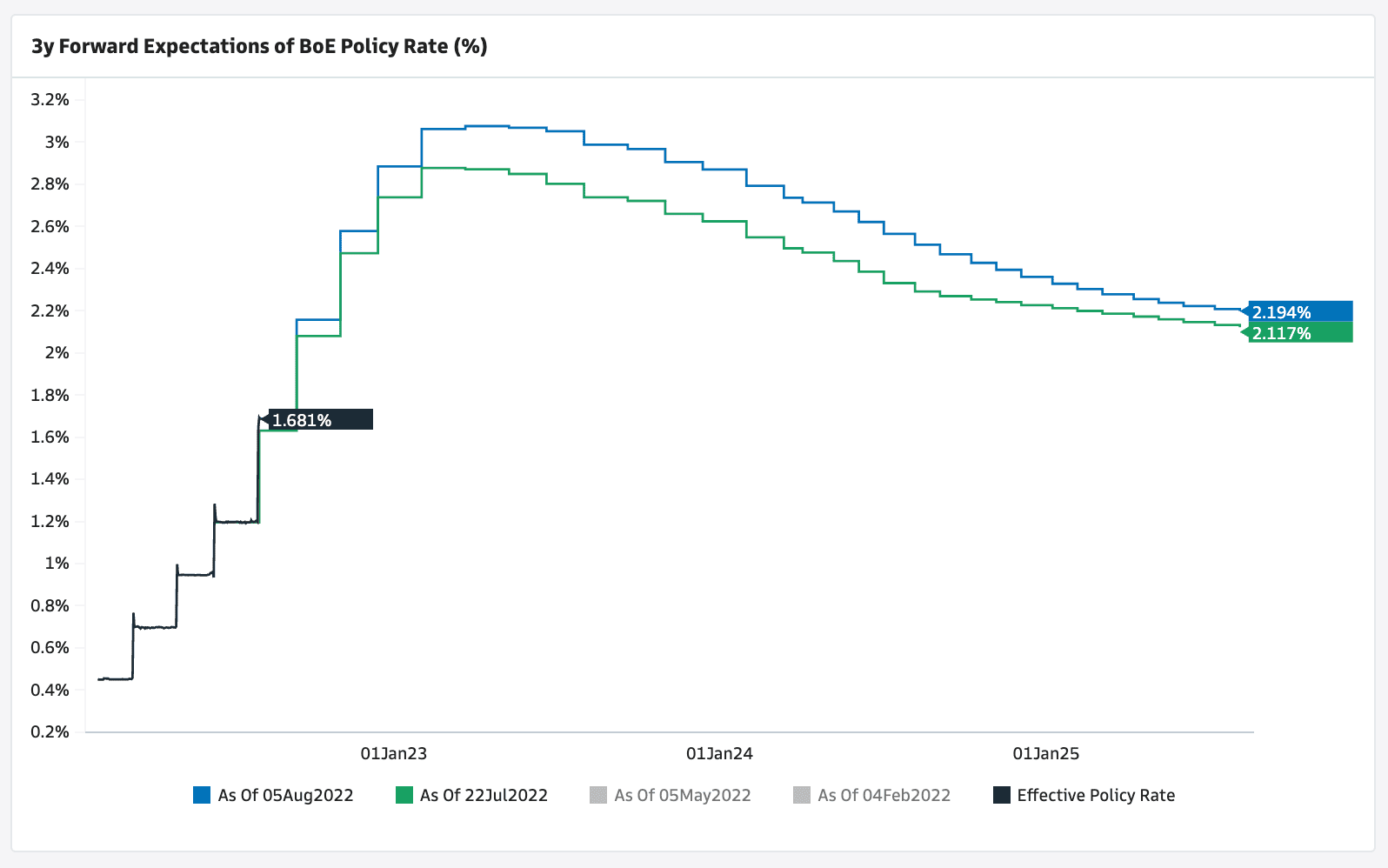

- Oxford Economics raise their Bank Rate forecasts

- Sees GBP/USD supported

- But GBP/EUR can trend down

- With 2023 rate cuts in prospect

Image © Adobe Images

The British Pound will remain supported against the Dollar show new forecasts but the prospect of Bank of England interest rate cuts in 2023 could create downside pressure, particularly against the Euro says an independent economics research provider.

But Oxford Economics says the Bank will now likely raise interest rates faster and higher in 2022 than they had initially though, due to surging inflation and a desire to support the Pound near-term.

"We now expect Bank Rate to peak at 2.5% in November, up from our previous forecast of 2%," says Andrew Goodwin, Chief UK Economist at Oxford Economics.

The Bank of England hiked interest rates by 50 basis points on August 04 as it raised the tempo in its fight against inflation.

"Having stepped up the pace of rate hikes, it would look odd to throttle back straight away. The Fed and ECB are likely to continue to hike at a rapid pace, and a desire to support sterling will likely drag the BoE along with them," says Goodwin.

The Pound initially fell in the reaction to the rate hike, which appeared to be a classic "sell the fact" by a currency market that had bid it higher against both the Euro and Dollar in the two weeks leading to the decision.

On the surface, a 50bp hike is broadly supportive of the Pound, as are the indications the Bank is not yet ready to stop.

But, dire economic forecasts that showed a prolonged recession would start towards year-end ultimately stole the headlines.

The Bank however said it was only concerned with inflation fighting and would not place a heavy emphasis on these forecasts, therefore prompting markets to bet further hikes are coming.

Oxford Economics says their revised expectations for raising Bank Rate to 2.5% would put the policy rate some way above most estimates of the neutral rate.

The neutral rate is the point where interest rates are neither stimulatory nor contractionary.

Going above neutral would mean the Bank increasingly becomes a headwind to UK economic activity, raising the prospect of rate cuts when inflation starts to fall.

Oxford Economics thinks the Bank will pause after November's meeting, as a continued lack of evidence of second round effects from higher wages tilts the risk profile away from concerns about high inflation becoming embedded.

Above: Money market pricing shows the market raised expectations for Bank Rate's path in the wake of the Aug 04. policy update. But, they also show rate cuts are likely in 2023 as the economy slows. Image courtesy of Goldman Sachs.

"Given the fragile backdrop, this makes rate cuts in 2023 more likely," says Goodwin.

They then expect 75bps of rate cuts in 2023, "as it becomes clear that the BoE has overreacted".

This expectation is reflected in forecasts for a lower Pound relative to the Euro: the Pound to Euro exchange rate is forecast by Oxford Economics to be at 1.16 from the end of the third quarter 2022 right through to the end of the first quarter of 2023.

But a broader retreat by the Dollar is anticipated to ensure the Pound to Dollar exchange rate is kept off its 2022 lows going forward.

The pair is forecast to remain above 1.20 and seen at 1.22 from the end of the third quarter through to year-end, ahead of a rise to 1.23 by the end of the firs quarter 2023. (Set your FX rate alert here).

Bank of England's Forecasts "Economic Nonsense" says Toscafund's Savouri

Elsewhere, the Bank of England's forecasts for a long and enduring UK recession have been branded unrealistic by Savvas Savouri, Chief Economist and Partner at hedge fund Toscafund Asset Management.

In fact, the Bank is so wrong in its predictions the economists who drew up the predictions will be "embarrassed" and will choose to omit their time at the Bank from their CVs, says Savouri.

"I do not accept that a statistical recession looms. Yes, we might, just might see real GDP fall in Q2. Thereafter, I see little or no chance of what the BoE projects will be another decline in Q4, followed by its staggeringly-stupid prediction of SIX further sequential falls," says Savouri in a note following the Bank's August 04 decision to raise interest rates.

"How can an economy not grow when employment levels are rising thanks to unprecedented hiring intentions and so too, wages?" asks Savouri, noting the UK's strong jobs market and hiring intentions at businesses.

"Which sectors does the BoE in its "wisdom" predict will misfire to the extent they create a labour market reversal? The answer is that no reversal is possible for all sorts of reasons which should be clear to all, even if not the BoE," he asks.

Savouri observes the economy has a fundamentally healthy property market – both residential and commercial – and homeowners have never had as much equity in their homes.

This in addition to record high household savings.

"To the Bank of England and its economists, I say this. You have no idea what a real recession looks like and will be proven so wrong. Indeed, you will be so embarrassed by what you have been part of that choose to hide from your CV the fact you worked in Threadneedle Street over a period which will go down in history as its forecasting worst," he adds.