- GBP a middle of road performer in Nov despite new BoE burden.

- Market now the most 'dovish' on BoE out of all G10 central banks.

- After RBA rate cut, RBNZ pivot and as hopes of Brexit deal rise.

- Market eyes 0% Bank Rate but deal could upend this applecart.

Image © Adobe Images

- GBP/USD spot rate at time of writing: 1.3380

- Bank transfer rate (indicative guide): 1.2990-1.3084

- FX specialist providers (indicative guide): 1.3158-1.3238

- More information on FX specialist rates here

The Pound has been burdened anew in November by evolving market expectations for interest rates at the Bank of England (BoE) and elsewhere in the world, although this weight around the ankles of Sterling could turn to a tailwind in the event that a Brexit deal is agreed over the coming days or weeks.

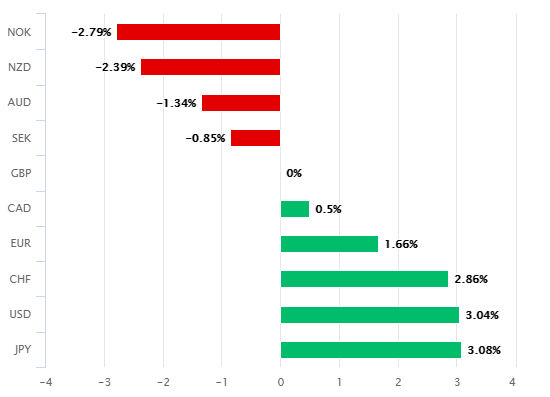

Pound Sterling was a middling performer among major currencies for month of November on Wednesday following a performance that resulted from both international factors as well as tentative hope in the market of progress toward a trade agreement with the EU.

But this performance and market focus on its underlying drivers have obscured a less favourable set of developments in the pecking order of central bank policy rates, where the UK has fallen to the bottom of the major economy class.

Of late the Reserve Bank of Australia (RBA) has cut its cash rate to a new record low of 0.10%, matching it exactly with the BoE's Bank Rate, while an about-turn at the Reserve Bank of New Zealand saw investors abandon earlier wagers that it would cut Kiwi borrowing costs below zero early in 2021.

Both took place early in November and left expectations for the BoE the most 'dovish' among major central banks, a potentially bearish turn for Sterling.

"A critical period is now (again) at hand for post-Brexit trade talks," says Tim Riddell, a London-based strategist at Westpac. "Hopes for a deal held GBP/USD above 1.30 recently, so an actual deal may only lift GBP towards 1.35 while a faltering of talks could see GBP slip back towards 1.27."

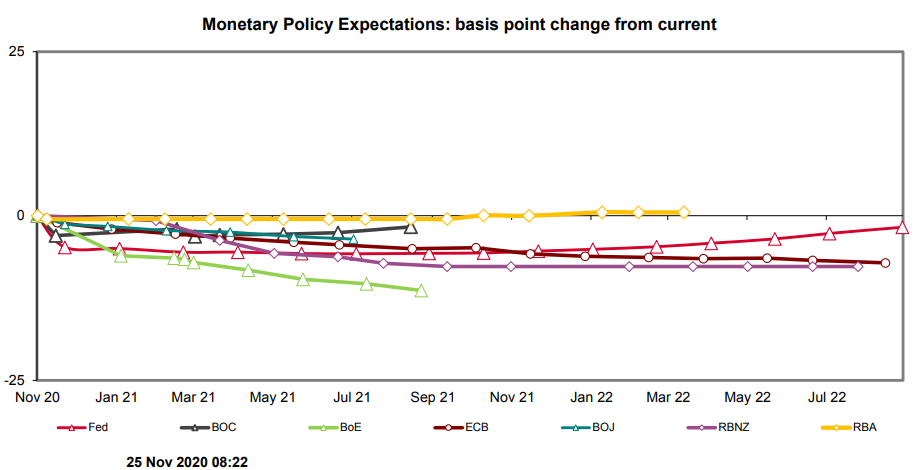

Source: Westpac. Overnight Index Swap (OIS) market expectations for G10 cash rates on Nov 25. BoE shown in green.

Pricing in the overnight-index-swap market implied on Wednesday an expectation among investor that the BoE will cut Bank Rate from 0.10% to 0% by the June 2021 at the latest, with a hefty probability of that coming much sooner rather than later.

BoE Governor Andrew Bailey appeared before the House of Commons of Treasury Select Committee this week where his words provided more fodder for internet trolls of the anti-Brexit variety than they did new information on the policy outlook. However, the governor has warned repeatedly this year that just like the RBNZ previously, the BoE also considers negative interest rates to be a useful if-not policy tool for use by the bank, which partly explains why investors continue to bet on further cuts to Bank Rate.

Watch our full session with the Bank of England from yesterday here👇

— Treasury Committee (@CommonsTreasury) November 24, 2020

📺https://t.co/GSQnmtwBZq

No-deal Brexit to cost more than Covid, Bank of England governor says https://t.co/dilQQblM9f

Bailey was reported this week to have suggested that failure to secure a Brexit trade agreement would "cost more than covid," or in other words, the coronavirus that sunk UK GDP by nearly -20% in the second quarter. Such reports omitted the "long-term" context of his remarks.

The "long-term effect of COVID" could be as little as zero given the related economic damage was done by temporary, but related government restrictions rather than the virus itself. Meanwhile, Brexit has since the referendum been billed by the BoE as a threat to the long-term prospects of the economy instead of growth in the here and now.

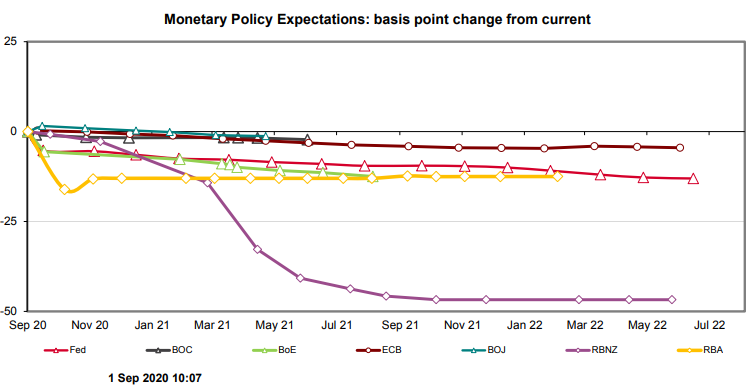

Source: Westpac. Market expectations for G10 cash rates back on September 01, 2020. BoE shown in green.

Nonetheless, the outcome of the Brexit trade talks will be key to the evolution of the green lines on the above graphs as well as the trajectory of Pound Sterling.

"The reality is that negotiators can only take the discussions so far without intervention from national leaders. We've refrained from making decisive calls on EURGBP on a 2-week/1-month horizon because we don't think the probabilities of an agreement (by year-end) have moved much in the last few weeks," says Stephen Gallo, European head of FX strategy at BMO Capital Markets. "That said, we are aware of the fact that the FX market has taken a more optimistic view."

Failure to reach a trade agreement could mean more punishing losses for the Pound as well as a push by the BoE toward zero and below with Bank Rate, although on the flip side there's some chance of investors revising away their anticipated rate cut in the event that negotiators announce they've reached an agreement. The resulting reappraisal of the interest rate outlook could provide an additional tailwind to the Pound if Novembers' performance of the New Zealand Dollar is anything to go by.

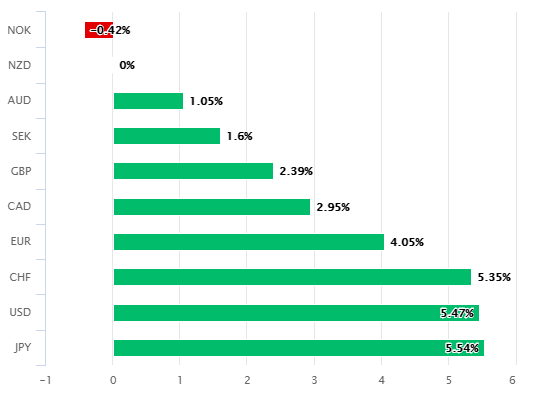

Pound Sterling has fallen more than 2% against the Kiwi this month in response to the RBNZ's policy pivot, while the New Zealand currency has risen close to the top of the majors' league table for the period, leaving it behind only the oil and equity-linked Norwegian Krone.

Above: Sterling (left) and Kiwi (right) performances against major currencies in 20 trading days to Wednesday.

On Brexit itself, European Commission chief Ursula von der Leyen said Wednesday that "genuine progress" had been achieved in the negotiations but that the risk of failure remained. When the EU has asked for, or simply spoken of "progress" over recent years, it's almost always been in reference to compromises on the part of the UK.

Meanwhile, Prime Minister Boris Johnson told parliament that "our position on fish hasn't changed. We'll only be able to make progress on if the EU accepts the reality that we must be able to control access to our waters," while saying nothing in relation to other contentious European demands including the for so-called level playing field terms around state aid, environmental regulation and taxes as well as other non-environmental taxes.

Von der Leyen implied when addressing the EU parliament that there's been progress in relation to these issues too, saying "In the discussions about state aid, we still have serious issues, for instance when it comes to enforcement."

The EU has demanded from the get-go that Britain remain bound by all of its rules in the above areas while the political declaration accompanying the EU withdrawal agreement, when combined with new powers afforded to Brussels by the EU27 in July, implies scope for the EU to pursue new powers over the UK including in relation to tax matters where it never had competence during the country's period of official membership.

PM Johnson has so-far resisted all of those demands, while British negotiator David Frost said in his last official remarks; "We are working to get a deal, but the only one that's possible is one that is compatible with our sovereignty and takes back control of our laws, our trade, and our waters. That has been our consistent position from the start and I will not be changing it," without ruling out a possibly pending change of position by PM Johnson.

Above: Pound-to-Dollar rate shown at weekly intervals alongside Pound-to-Euro rate (black line, left axis).