We consider the potential impact on the Euro exchange rate complex of the weekend's referendum in Italy.

On Sunday, Italian voters will be asked whether they approve the proposed reform of Italy’s constitution, which aims to reform the Senate, overcome perfect bicameralism and review the division of power between the central government and regions.

Italian Prime Minister, Matteo Renzi will face one of the biggest challenges to his political leadership and if he loses he may have to resign leaving a political vacuum which markets fear could lead to a snap election which could open the path for a victory for the anti-European Five Star Movement.

If the vote passes, some see calm as being restored – whilst the more pessimistic see danger simply being delayed.

Therefore, the No vote succeeding represents risk owing to the uncertainty it poses.

If turnout is high on Sunday it is believed there is less of a chance of a Yes victory as all the opposition parties are urging their followers to reject the referendum.

How would such an outcome challenge the leadership of Europe, the supremacy of Brussels and the longevity of the single currency?

Analysts appear split as to how much of an impact the referendum could have on these wider issues.

What Will Happen in the Event of No Vote?

Some see a potential 'butterfly effect' - it may be that the Italian referendum could trigger, via a ripple effect, with serious consequences for Europe as a whole.

Other's see the potential threat as 'overhyped' and the probability of a domino effect impacting on the Eurozone in a substantial way as very small.

Dr. Loredana Federico, Lead Italy, Economist at UniCredit Bank in Milan says if the No vote prevails, Mr. Renzi would likely resign from his post as prime minister but not as PD leader.

President Sergio Mattarella could decide to ask Mr. Renzi to verify, with a vote of confidence, whether he can still count on a parliamentary majority.

"Alternatively, the president could start a round of consultations with key institutional players and political parties to form a transitional government with limited scope and duration. Early elections right after the referendum are unlikely because the electoral law would need to be changed first," says Federico.

Latest Pound/Euro Exchange Rates

| Live: 1.1701▼ -0.04%12 Month Best:1.1719 |

*Your Bank's Retail Rate

| 1.1303 - 1.135 |

**Independent Specialist | 1.1537 - 1.1584 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Impact on the Euro

Analyst Alvise Marino, of Credit Suisse, is of the of the view that the referendum could heavily impact the single currency.

Marino sees a win for the “No” vote in the referendum as detrimental for the Euro, as it would trigger fears of a rise to power for the anti-EU Five Star Party.

“A victory of the ‘no’ vote would not necessarily cause the Renzi government to fall, but it would likely cause fears of such an outcome to grow rapidly, especially in the light of the strong performance of the anti-euro 5-Star Movement party in local elections in June of this year and with an eye on national elections in Germany and France in 2017 (potential repercussions from the Italian vote on next year’s electoral consultations in the two largest countries in the euro area alone argue against an idiosyncratic interpretation of the referendum results),” said Marino.

Those fears would lead to a sudden rise in the cost of borrowing due to the added risk premium of Italy potentially leaving the EU, which would prompt easing from the ECB, and would thus be negative for the Euro.

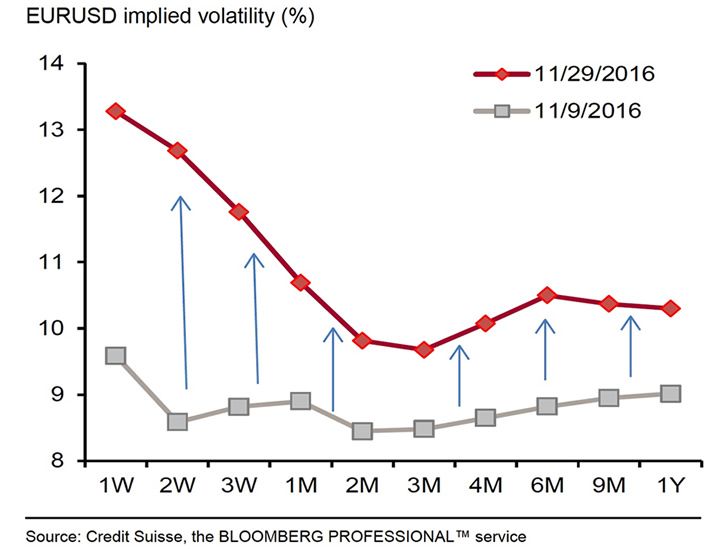

Indeed, Credit Suisse note that the cost of insuring against volatility in the Euro-Dollar exchange rate is now more costly than it was going into the US election.

However, it remains well below Brexit levels. This in itself helps put the potential for volatility following the vote into perspective.

But why does the referendum pose a risk to the Euro?

“Given the focus on the local banking industry’s near-term funding needs, widening credit spreads would amount to a tightening in financial conditions, which could amongst other, trigger expectations of a response by the ECB in the form of a more accommodative monetary stance – a likely EUR negative outcome, in our view,” says Marino.

The analyst is of the view that a win for the “No” vote would lead to a fall in EUR/USD as the single currency would weaken against strengthening Dollar.

Credit Suisse forecast more downside in the pair, which they recommend trading via a put option due to an expected win for “No” who have been; leading by a substantial margin in polls.

Marion says he is “positioned for additional EURUSD downside via a 20 December 2016 expiry EURUSD 1.085 strike put (link) and a 4 Apr ’17 expiry EURUSD 1.00 one touch.”

BNP Paribas: A Win for “Yes” Poses More Risk to the Euro

The opposite opinion to Credit Suisse’s is held by BNP Paribas, who do not see a win for the “No” vote as impacting on the Euro.

“According to our economists, although the impact of a ‘no’ vote would not be neutral, it might be less damaging than many in the market assume.

"We do not expect a protracted period of political instability, and Prime Minister Matteo Renzi would be reasonably likely to hold on to his job after a period of uncertainty,” says Paribas’ Clara Leonard.

Leonard does not think credit will suddenly tighten after a “No” win due to fears of an EU implosion because she sees much more resilient mechanisms in place to provide liquidity, such as the European Stability Mechanism, a massive emergency fund.

In fact, the view of Paribas is that a win for “No” may be the lesser of two evils.

For them, a “Yes” vote would pose the greater risk for several reasons.

First is that it could make Matteo Renzi and his PD party over-confident about their chances of winning a general election, which might make them more complacent about changing a new electoral law, called the Italicum, which awards extra seats to the party with the largest share of the national vote.

The Italicum awards the largest party with a boost for being the largest party – as long as it has over 40% of the share of the vote – giving it over 50% of the seats in parliament.

It was brought in to increase the power of the largest party so as to create stronger government with more powers to make bold reforms.

The Italicum was introduced by Renzi’s government in July 2016 but it has already drawn huge criticism and is being challenged in the constitutional courts.

It is feared the Italicum could help the anti-EU Five Star party gain total power, and lead to an Italexit, since Five Star is currently leading PD in the polls.

Although Renzi has promised critics in his own party he will amend the Italicum to lessen its majority premium, if he wins the referendum he will be more likely to make the amends minor, which could still keep the door open to a Five Star sweep at the next election.

Another major reason why a “No” win would be preferable is that it would keep the Senate as an electable second house with the power to veto the lower house’s laws.

Then, even if Five Star won an all-out majority with the helping hand of the Italicum, they would still be stymied from pushing through their radical anti-EU agenda by the Senate which would have been voted in via the old proportional system. “

Political Risk has had little Impact for Far

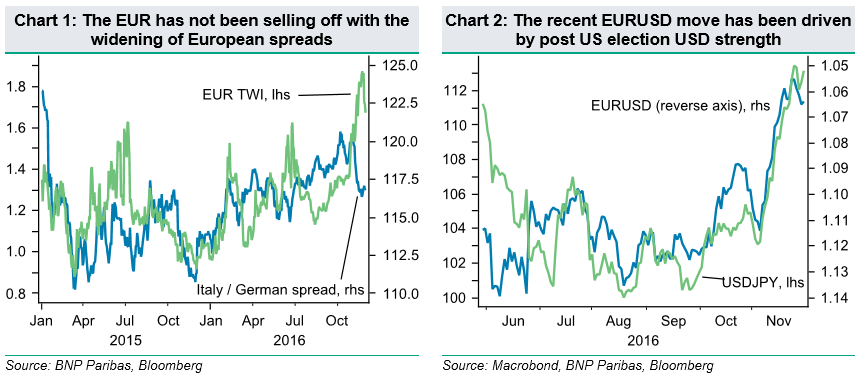

Despite the "No" vote leading in polls for quite some time and by a fairly large margin Paribas' Leonard notes how it has had little impact on EUR/USD.

She compares EUR/USD's recent weakness with the Italian over German bond spread, which has risen substantially due to fears of the "No" vote leading to an Italexit (see below).

Normally the EUR/USD and the spread correlate, however, recently they have diverged, showing the weakening of the pair has not been due to referendum risk, but rather another factor.

Leonard suggests the factor is the hype over Donald Trump's reflationary stimulus policies and references a chart (see below) which shows a high degree of correlation between EUR/USD and USD/JPY - the Dollar versus the Yen providing a purer benchmark of USD strength, since the Yen has been a passive partner recently.

By extrapolating this relationship forward Leonard argues EUR/USD will perform much more as a result of US factors than Italian referendum risk.

Euro’s Positive Reaction to Risk

A further argument in favour of a win for “No” not weakening the Euro comes from its link to risk.

Paribas’ Clara Leonard says that the Euro has had an inverse relationship to risk ever since interest rates in the EU dropped to record lows.

This is because these record low rates made it a popular funding currency for 'Carry traders.'

These traders borrow currency at low interest rates and invest them in riskier currencies with high interest rates.

When global risk appetite wanes, however, the same carry traders see their positions losing profit so the unwind them and repatriate the borrowed Euros – actually leading to a boost in the Euro.

“The EUR has been used as a funding currency for FX carry trades and the risk-off environment has forced the unwind of these trades, leading investors to buy back the EUR.”

It is quite possible, therefore, that a win for “No” would lead to widespread concern and a fall in global risk appetite, which would see an increase in repatriation flows back into the Eurozone, boosting demand for the Euro and thus supporting it.