No trend lasts forever, and this surely holds true for Europe's shared currency which has been under pressure since 2008. We believe there are signs a sustained period of strength is drawing close.

- German economy now fastest growing in G7

- Suite of fundamental, quantitative and technical signals advocate for EUR strength

- No desire at European Central Bank to further lower interest rates, should free up euro strength

For years now it has been difficult to discuss the euro with anything other than a negative tone.

We have seen the Greek debt crisis, the peripheral debt crisis, national bailouts, political discord all rounded off with the dumping of gargantuan quantities of euros onto the markets by the European Central Bank which has been tasked with papering over the cracks.

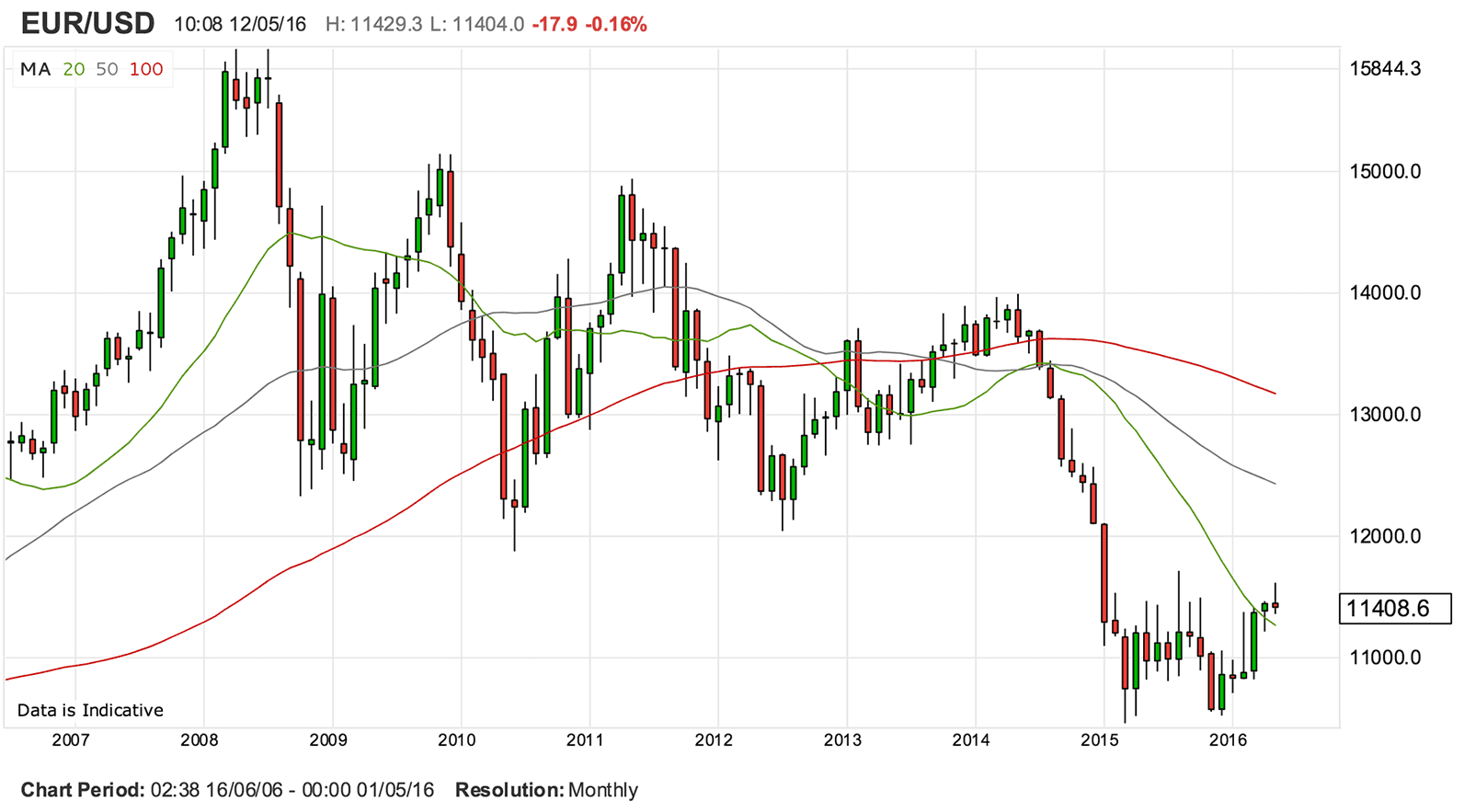

The euro has suffered under the weight of this money dump; it has fallen from levels above 1.50 in 2008 to the 1.10’s we are seeing now.

The loss in value has been fundamentally justified as the European economy which turned weaker after the 2008 crisis and underperformed global peers; the Europeans have been paying their dues for their structural uncompetitiveness and this is reflected in the euro’s decline.

And the negative discourse surrounding all things euro continues in 2016 with a host of big-name researchers continuing to advocate for the euro’s decline to 1:1 against the dollar.

Within this landscape we continue to look the other way, and look for signs of the turnaround which must ultimately happen.

A look at the chart we have stuck into this article offers hints at what is going on. Look at that consolidation around the current lows, it is unprecedented in the post-2008 history of EUR/USD and hints at a solid layer of support above parity.

While the EUR could continue to ease in the short-term, possibly as far as 1.1200 before it finds some stability, this is nothing when we consider the big moves of recent years.

From a technical perspective the euro to dollar exchange rate is already in a technical uptrend, having formed a base in late 2015 and looking intent on testing the upper limits of its consolidation zone in the 1.14’s.

Latest Pound/Euro Exchange Rates

| Live: 1.174▲ + 0.08%12 Month Best:1.1752 |

*Your Bank's Retail Rate

| 1.1341 - 1.1388 |

**Independent Specialist | 1.1576 - 1.1623 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

In fact, looking beyond just the technicals, the bigger picture is also turning pro-EUR.

“A 20%+ EUR long remains a central feature of the portfolio for another week. The region’s huge current account surplus has been an important catalyst for the model’s structural EUR long but interestingly we are now also observing a positive growth signal and a less weak total yield signal too,” says Rob Rennie at Westpac in Sydney.

The portfolio being referred to here is Westpac’s “High Conviction Trades" model which blends the long/short/neutral recommendations from their three research streams: G10 FX model (quantitative analysis), ForeX focus (macro analysis) and technical analysis.

This suggests a whole range of drivers that we obsess over when considering currency valuations are merging into a positive signal for the euro.

The Euro Has Bottomed

Picking up the ‘euro turnaround’ theme this week are long-time euro bulls UniCredit SpA.

Back in 2015 researchers at the Milanese lender joined a small cabal of analysts who saw the end of the dollar’s post-crisis cyclical ascension and warned it was time to drop expectations for parity in EUR/USD to be achieved.

Now, we hear UniCredit are upgrading their euro-dollar forecasts for 2016.

In a note to clients released on the 11th May, Dr. Vasileios Gkionakis, Global Head of FX Strategy at UniCredit Bank in London says a “mix of high past (and current) overvaluation with strong downside momentum should lead to the dollar selling off further as value investors increase short exposure and momentum traders jump on the trend.”

UniCredit point out a second cornerstone to their pro-EUR/USD forecasts is the removal of a formidable hurdle to further appreciation - the ECB.

The central bank’s recent communications hint at a shift from its previous obsession with the exchange rate.

“We believe that the ECB has – rightly – stepped back from talking the euro down and in terms of monetary policy action we think that it is pretty much done,” says Gkionakis.

Rather, the ECB will likely concentrate on credit easing as it would be a more effective channel to boost the Eurozone economy suggests Shahab Jalinoos, Head of Global FX strategy at Credit Suisse:

“In our view the key catalyst for the reversal was ECB chief Draghi's suggestion that the ECB is close to the end of the road in terms of pushing further on negative rates as a policy tool.

“We have argued a shift in the policy mix for further easing away from negative rates (previously seen as targeting a weaker currency as a key objective) towards credit easing can be viewed as a potential positive for the EUR.”

This week the ECB's Vice President Constancio used a speech in London to remind the market to give the central bank time to allow their measures to take effect.

Markets read this as further confirmation that the Bank was stepping away from EUR-negative policy stances.

The head of Germany’s Bundesbank, Jens Weidmann, has meanwhile followed Constancio’s comments warning on the risks associated with keeping the ECB's ultra-low rates and money-printing programme going for too long and defended Germany's conservative fiscal policy against accusations that it was slowing down the European economy.

"An expansionary monetary policy stance is justified for now," Weidmann said at an event in Frankfurt. "But we must not over-extend the period of ultra-loose monetary policy, because various risks and side effects are part and parcel of the current policy stance.”

Thus, as central bank noise abates the currency should continue to move freely, closer to fair valuation which UniCredit see as being towards the 1.20’s against the dollar.

UniCredit have therefore raised higher their euro forecasts and now see EUR-USD at 1.18 by end-2016 (1.12 previously) and at 1.22 by end-2017 (1.18 previously).

The Data is Heading in the Right Direction, Lead by Germany

Perhaps the ECB’s policy of dumping vast quantities of cash are starting to pay off, as per the improving tenor of European data releases.

Eurozone Q1 GDP was surprisingly strong at 0.6%q/q, boosted by domestic demand, ensuring it outperformed both the US and UK over the period.

German factory orders smashed median expectations in March with orders increasing 1.9% in the month.

On the 13th of May German GDP was reported to have risen 0.7% in the first quarter confirming the Eurozone's economic powerhouse is the fastest growing economy in the G7 with annual growth now set at 2.75%.

“The aggressive acceleration in factory output favours a continued uptrend in the Eurozone economic surprise index (ESI). Although the series currently remains in negative territory it has moved aggressively higher since registering a near three year low at the end of February,” says analyst Jeremy Stretch at CIBC Markets in London.

The uptrend in the ESI is contingent with the continued reduction in EUR speculative shorts - a sign that markets are turning more positive on the euro’s prospects going forward.

Investors have meanwhile pared negative EUR positions for seven straight weeks, reducing positions to the lowest level in almost two years as a sign of shifting sentiment in the market.

This is a pertinent shift as analysts tend to lead the markets.

The markets are always right of course, but there is always someone who can see where markets are going before they embark on the journey.

The trick is to find these analysts and scrutinise their thinking and decide whether their vision is plausible before the crowd has the chance to do so.