When looking at the euro / dollar exchange rate at current levels we sense a lack of conviction on the pair’s prospects of advancing much higher.

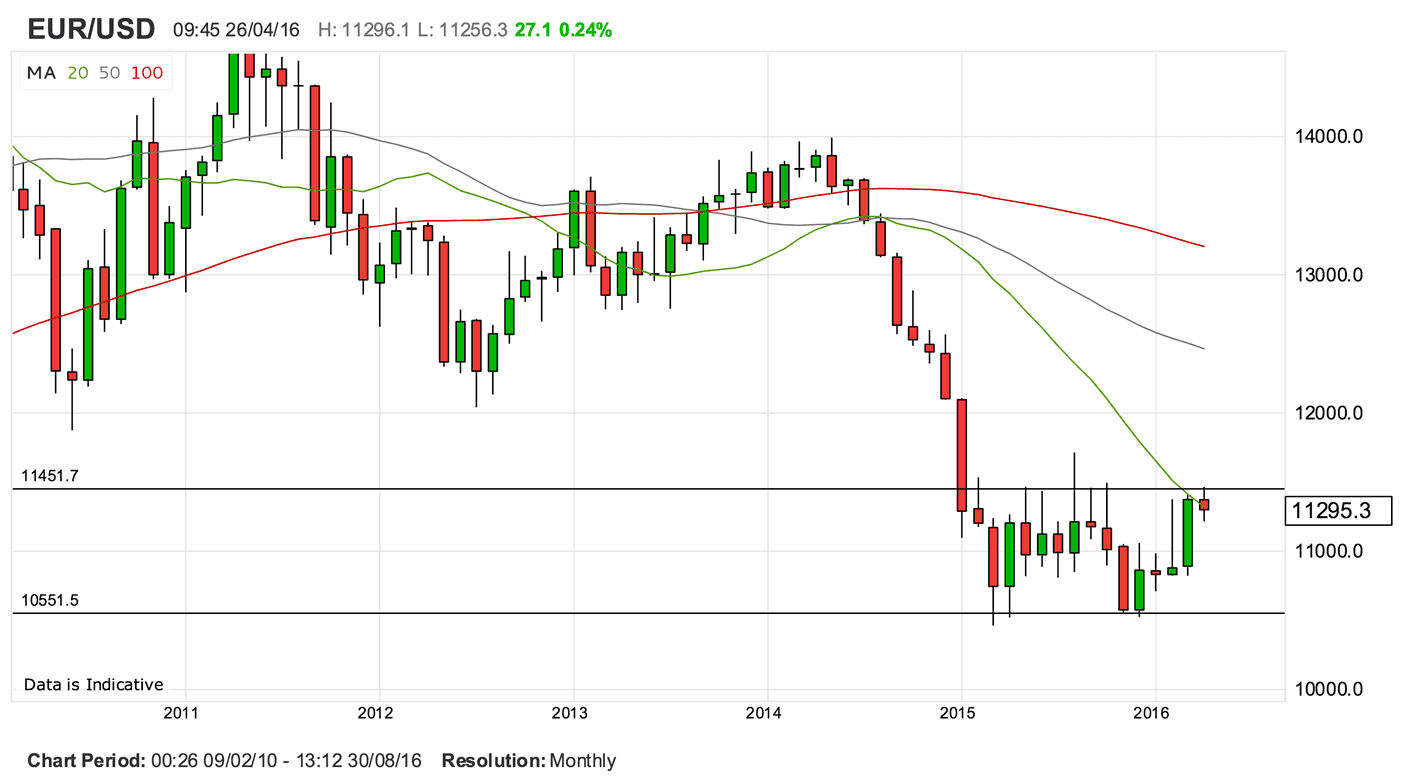

A look at the monthly charts tells the story of a currency pair that is struggling to find any amount of traction beyond the 1.1450 marker:

Not once, since 2015, has the exchange rate managed to close above these levels on a monthly basis.

However it can’t be said that the euro bulls haven’t been trying over the past four months as we have seen upside momentum increasing with each month offering a close higher than that of the previous month.

So fledging momentum is there; the question is can we crack beyond the ceiling at 1.1450 and if so how far can the rally extend?

Forecasting EUR to USD Conversion @ 1.16

Ultimately, we feel a break higher in the euro will only happen when markets move away from their current interest rate settings.

Briefly put, markets see little prospect for any change to US and EZ interest rates to be delivered over coming months.

However, this vacuum of policy change could work in favour of the euro argue analysts at BNP Paribas who believe that the euro does have the legs to extend beyond the ceiling at 1.1450.

In their latest briefing to clients BNP argue that any upside moves in EUR/USD are likely to stem from the USD side of the equation, i.e dollar weakness.

“Financial conditions in the US have tightened significantly and we no longer expect the Fed to hike rates in 2016 or 2017. This implies a much smaller USD appreciation versus the EUR, JPY, and CHF than we previously forecast, implying the USD bull market is entering a long pause,” say BNP Paribas in a briefing to clients.

The prospect of higher interest rates in the United States are central to the USD appreciation story - higher interest rate yields would see a greater demand for US assets, thus driving up the value of the currency.

Back in December 2015 the US Federal Reserve was hinting at the prospect of up to four interest rate rises in 2016.

On the first of December the EUR/USD exchange rate was quoted at 1.0569.

Fast forward, and now markets are expecting, at best, one interest rate rise in 2016. The EUR/USD is now quoted at 1.1287 at the time of writing, confirming just how important interest rate expectations are.

The call by BNP Paribas for no interest rate rises could well be on the money thus strengthening their argument for a subdued dollar going forward. It is also an out-of-consensus call, therefore justifying an out-of-consensus upside target for EUR/USD.

Limiting the euro’s inability to break much higher are the declining interest rates in the Eurozone where the European Central Bank (ECB) has cut into negative territory. The Eurozone is therefore likely to continue supplying euros into higher-yielding areas, ensuring the exchange rate remains hampered.

Nevertheless, there remains the potential for advances argue BNP Paribas who also believe subdued global investor sentiment could well play in favour of the single currency:

“We think EURUSD could rally to 1.16 by mid-year, despite the ECB delivering a significant set of easing measures. A fragile risk environment is likely to deter eurozone outflows, leaving the EUR supported by its current account surplus.”

However, analysts expect EURUSD to fall back to 1.14 by the year end, ultimately betraying a business-as-usual forecast for the exchange rate pair over coming months.

The Other Side of the Coin: Expect the Euro to Fall

It is important to note however that this view is at odds with those forecasters who see a notably lower euro to dollar exchange rate.

We recently presented the views held by analysts at Scotiabank and the Bank of Nova Scotia where declines towards parity are expected in 2016.

The strength in the EUR is unsustainable. Support for the USD from the asymmetric growth and diverging monetary policy dynamics between the US and Europe has yet to materialise but we find it hard to get too negative on the dollar,” says Pablo F.G. Bréard at Scotiabank.

At the same time, Bréard fails to find enthusiasm on the EUR.

“We cannot exclude the potential for EURUSD to gain towards 1.15 in the short run, but sluggish Eurozone growth and extremely low inflation (and inflation expectations) will weigh on the EUR later on in the year,” says Bréard.

Analyst George Saravelos at Deutsche Bank has reiterated his call for the EUR/USD to reach an exchange rate of 1:1.

(This is a notable upgrade from previous forecasts for a decline to 0.85.)

Saravelos outlines 3 reasons behind maintaining its medium term bearish EUR/USD view:

- Despite recent Fed dovishness, the real rate differential between Europe and the US is not signalling a large divergence in FX versus monetary policy expectations. To change our medium-term euro view, we would need to agree with current market pricing, that the Fed is on hold this year. We don’t: one or two hikes seems more reasonable.

- The underlying flow picture is not changing either. Updated portfolio flow data released this week show that the relentless fixed income outflows from Europe continue at full speed, currently running at an annualised half a trillion euros. There is little to suggest that hedging behaviour on these flows should be changing either: 1-yr euro cross-currency basis is reasonably stable, in contrast to Japan where the cost has more than doubled in recent months.

- We don’t think that the medium-term dollar bull trend is over. The recent dollar correction is not unusual for medium-term cycles."

And medium-term tops only happen when the dollar turns into a low-yielding currency argues Saravelos.

The Greenback is currently a mid-yielder – and is still on track for higher, not lower, yield rankings by the end of the year.