Image © Adobe Stock

The Euro is considered among the most vulnerable to a persistently strong Dollar.

The prospect of persistent U.S. economic strength opens the door to a period of extended Dollar outperformance, according to Standard Chartered, the global investment bank.

Responding to the blow-out U.S. job data for January, analysts at Standard Chartered say previously-held expectations for a gradual or more rapid softening of demand are now being questioned, and there is a risk that incoming data also beats to the upside.

"A cyclical or structural upswing in U.S. activity would make a case for pronounced and extended USD strength. This scenario has risen in probability," says Steve Englander, Head of Global G10 FX Research at Standard Chartered.

"Given the size of the NFP shock, we think it will take either a surprise of equal magnitude in the opposite direction or an accumulation of softer data to reverse the impact," he adds.

He expects Dollar exchange rates to advance if incoming data reinforces the signal sent by the jobs report.

But which currencies are particularly prone to an extended period of Dollar strength?

"The currencies we see as most vulnerable are those whose central banks may face pressure to ease because of soft inflation or activity, regardless of the Fed stance," says Englander.

Standard Chartered considers the Euro, Canadian Dollar, and Franc as most vulnerable if their economic data surprises to the downside.

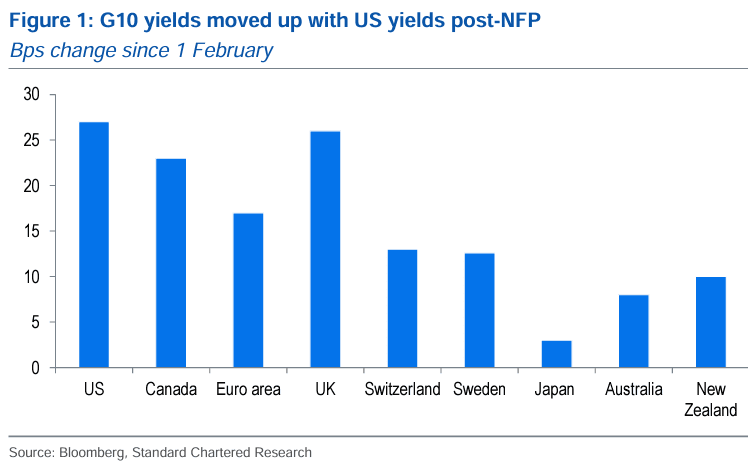

The above chart shows that bond yields rose across the G10 strip following the non-farm payroll data as investors bet central bank rate cuts would be delayed elsewhere.

After all, most central bankers would be more comfortable taking a cue from the Fed to avoid first-mover attention. But some G10 central banks might have little choice but to cut before the Fed does if domestic data disappoints and U.S. data remains strong.

"The potential for currency weakness is if domestic data in these economies do not justify the added hawkishness priced in. If domestic economic and inflation data point to easing by these central banks, we think this anticipated policy divergence will be reflected in FX pricing," says Englander.