- EUR/USD sets new 20-yr low in volatile open

- Tentatively regains 0.96 but outlook uncertain

- With busy schedule of data, event risk ahead

- Europe CPI & U.S. PCE figures the highlights

- But multiple ECB & Fed speakers also ahead

Image © European Central Bank

The Euro to Dollar rate opened the new week with a fall to fresh two-decade lows amid heightened volatility in international markets but faces a busy schedule of domestic data and event risk in the days ahead that will be instrumental in determining whether the single currency can recover its poise.

Europe's single currency fell briefly below 0.9550 against the Dollar in Europe on Monday in losses that coincided closely with steep declines in Sterling exchange rates, some of which reached new all-time lows in an apparent response to the burgeoning supply of UK government debt coming to market.

Monday's losses for Sterling were quickly reversed but had previously echoed price action seen on Friday and in another trading session that had also been marred by risk aversion in international markets, which appeared to weigh on many other currencies at the time.

The Euro was also quick to rebound back above 0.96 on Monday having shrugged off a downbeat Ifo survey of corporate sentiment and following a discernable boost that came against a backdrop of hawkish remarks from Croatian National Bank Governor Boris Vujcic and others on the European Central Bank Governing Council.

"We expect Germany will fall into a recession starting in Q3 and lasting throughout the winter. The September ifo survey results published today fit our bleak outlook," says Salomon Fiedler, an economist at Berenberg.

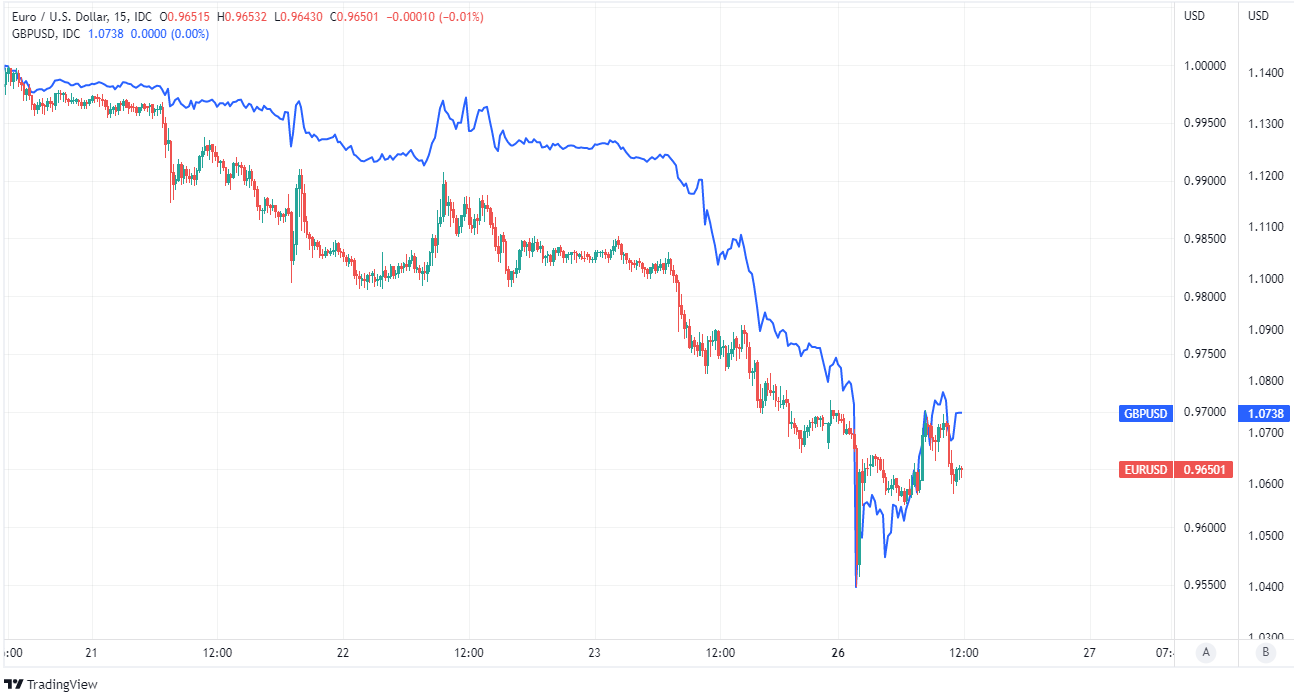

Above: Euro to Dollar rate shown at 15-minute intervals alongside GBP/USD. Click image for closer inspection.

Above: Euro to Dollar rate shown at 15-minute intervals alongside GBP/USD. Click image for closer inspection.

"The expectations component in particular plunged to 75.2 in September from 80.3 in August (Reuters consensus: 79.0), lower than any previous reading except at the height of the Covid crisis in April 2020 (72.0) – during the global financial crisis it had bottomed out at 79.2," Fiedler said on Monday.

While the Euro was quick to find its feet on Monday, much about the outlook for the single currency likely depends on how the market responds to a full sleight of economic data and event risks that litter the European and U.S. calendars for the week ahead.

These include a Monday appearance by ECB President Christine Lagarde before the European parliament Committee on Economic and Monetary Affairs as well as Friday's release of September inflation figures from Eurostat.

"The CPIs for Germany and Spain are released in the lead up to the Eurozone measure. The risk lies with another strong CPI that convinces the European Central Bank to keep up the pace of large increases in its policy interest rates," says Joseph Capurso, head of international economics at Commonwealth Bank of Australia.

"But we expect EUR to receive little support from higher interest rate expectations given the slump in the Eurozone’s current account. AUD/EUR can track lower this week," Capurso and colleagues said on Monday.

Above: Euro to Dollar rate shown at daily intervals alongside GBP/USD. Click image for closer inspection.

There is also a further appearance from the ECB's Lagarde at the Frankfurt Forum on US-European GeoEconomics on Wednesday while all of the European appointments are interspersed with a busy schedule of Federal Reserve (Fed) policymakers who appear publicly for the first time since last week's policy decision.

"The move lower over the past week has been mainly driven by the stronger USD leg following the hawkish policy update from the Fed on Wednesday at which is sent a strong signal that further large hikes will be required through the rest of this year," says Lee Hardman, a currency analyst at MUFG.

"The euro-zone CPI reports are expected to reveal that inflation has not yet peaked in the region, while the US PCE deflator should provide more encouragement that the peak for inflation has already past," Hardman also said in a Friday research briefing.

It's not clear if anything in the European calendar will be enough to stop the uptrend in the U.S. Dollar, which rose aggressively against many currencies after last week's interest rate decision, although this Friday's release of the latest Core PCE price index will be watched closely by the market.

This is the Fed's preferred measure of inflation and is set to be followed by appearances from no less than three Federal Open Market Committee members including Vice Chair Lael Brainard, while the Dollar could be sensitive to any optimistic takes on their part about the outlook for U.S. inflation.

Above: U.S. Dollar Index shown at monthly intervals with Fibonacci retracements of 2002 downtrend indicating medium and long-term areas of technical resistance. Click image for more detailed inspection.

Above: U.S. Dollar Index shown at monthly intervals with Fibonacci retracements of 2002 downtrend indicating medium and long-term areas of technical resistance. Click image for more detailed inspection.

The Fed lifted the top end of the Fed Funds rate range to 3.25% last week and warned that significant further increases are still likely, with the benchmark projected to rise above 4.5% at some time next year as part of the bank's effort to ensure that inflation returns to the 2% target.

This would see the Dollar offering what will potentially be, by then, a higher yield than all other G10 currencies that could further burnish its appeal to the market.

That prospect and poor investor sentiment toward the global economy have weighed heavily on the Euro in recent trading while ensuring that many commentators remain pessimistic about the outlook for the single currency.

"A hawkish Fed has prepared markets for a prolonged hiking cycle while Europe’s recessionary outlook due to ballooning energy prices should increasingly favor a lower EURUSD," says Thomas Flury, head of FX strategies at UBS Global Wealth Management.

"We think it’s too early to bottom-fish in EURUSD. We would hedge near-term EURUSD downside risks into next year until the Fed signals an end to the hiking cycle," Flury wrote in a Friday review of the outlook for the Euro.

Above: EUR/USD at monthly intervals with Fibonacci retracements of 2002 uptrend indicating long-term areas of technical support and Fibonacci trend extension of 2014 downtrend highlighting possible targets or otherwise pivot points for the Euro.