- EUR holds 1.18 on USD weakness, as ECB concerns fall on deaf ears.

- USD downturn, stimulus expectations put ECB policymakers in a bind.

- Control, policy credibility set to be tested as USD falls and EUR rises.

- Early, shock and awe stimulus increase may be only way to dent EUR.

© European Union, reproduced under CC licensing

- EUR/USD spot rate at time of writing: 1.1828

- Bank transfer rate (indicative guide): 1.1419-1.1500

- FX specialist providers (indicative guide): 1.1680-1.1727

- More information on FX specialist rates here

The Euro-Dollar rate remained within arms reach of September highs Tuesday despite a looming European Central Bank event that’s expected to it take aim at the Euro for its recent appreciation, but without a shock and awe stimulus there might be little policymakers can do to put a lid on the currency.

Europe’s unified unit was back above 1.18 on as the Dollar weakened against all major currencies even after U.S. core durable goods orders, a proxy for business investment, surpassed expectations for September.

Tuesday’s gains came after the Euro was caught by its 55-day moving-average just below 1.18 in Monday’s sell-off among risk assets, which has left the single currency’s strong upside bias intact with just two days to go before the October European Central Bank policy decision.

“We see this as the markets becoming more convinced of the deteriorating outlook for the US dollar going forward,” says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG. “Whoever wins the election next week, large fiscal stimulus is coming and coupled with that we believe the Fed will persist with an aggressive easing stance for longer than is usual for the Fed.”

The Dollar has been sold widely as investors price-in what many anticipate will be a victory in next Wednesday's presidential election for opposition candidate Joe Biden, who’s viewed as likely to spend more than the incumbent President Donald Trump would in any second term.

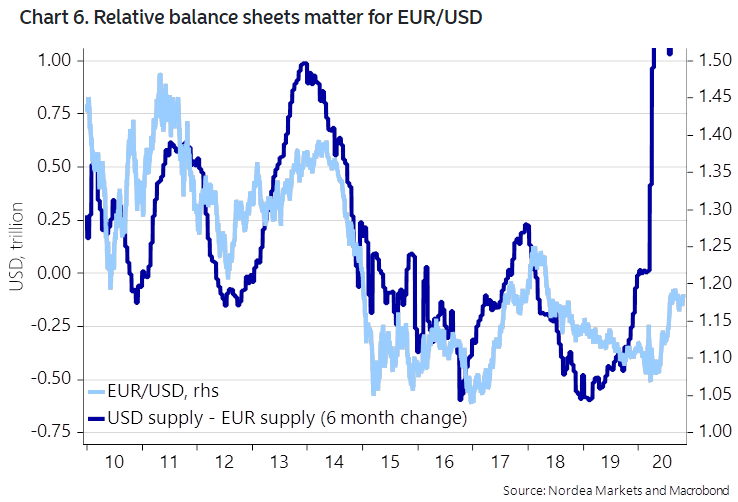

This could necessitate even further Federal Reserve (Fed) bond buying and balance sheet expansion which, according to an ECB research paper released last week, has likely been a factor in driving the Euro higher in recent months. The Fed has created new Dollars at a rapid clip this year to facilitate extraordinary levels of U.S. government spending, and much more so than the ECB or any other central bank, scaring investors away from the greenback and driving them toward alternatives like the Euro instead.

Above: Euro-Dollar shown at daily intervals alongside Dollar Index (black line, left axis) with selected moving-averages.

The Euro remained 9.6% above its mid-May level of 1.08 and 11.2% above its March and 2020 low of 1.0650 on Tuesday, reflecting gains that have lifted trade-weighted measures of the Euro by high single digit percentages and undermined the ECB’s efforts to jump start the Eurozone economy.

The EU’s coronavirus recovery fund had afforded policymakers the luxury in September of attributing some of the Euro's gains to an improved economic outlook, but an ongoing second wave of coronavirus and difficulties among EU members in taking the recovery fund forward mean the ECB will have no such privilege at 12:45 on Thursday.

“Is there anything the ECB can do in October (or December) that will really 'shock' FX and rates investors? We're not sure there is. Said differently, it is now widely accepted (by investors) that the ECB’s implicit role is becoming more of a fiscal one that has less to do with boosting inflation and all to do with supporting weaker sovereign credits,” says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

Europe’s single currency is now being kept at elevated, economically challenging levels not so much due to investors’ bullishness on Europe but more as a result of the market’s Dollar aversion. The resulting gains in the trade-weighted exchange rate are stifling export competitiveness and long-inadequate inflation pressures while in the process necessitating an ECB response to pull the all-important Euro-Dollar rate lower.

But with the ECB’s interest rates already at or below zero, the bank is limited in what it can do to bring down the Euro and to assist Eurozone economies, with its only meaningful option being to increase the size of its government bond buying programme. So far the bank has committed to buying €1.35 trillion of European government bonds in total, which has driven government financing costs lower and ensured that even the most fragile of ‘periphery’ economies were funded throughout the pandemic.

Source: Nordea Markets.

“The case for even more ECB easing has strengthened further lately, but we still expect the central bank to wait until December. Surprise easing already next week would boost bonds and hurt the EUR,” says Jan von Gerich, an economist at Nordea Markets. “More than half of the ECB’s EUR 1350bn Pandemic Emergency Purchase Programme (PEPP) envelope remains unused, while the ECB has said this programme will continue at least until the end of June 2021, so there is no rush to increase the size of the programme.”

The rub for the ECB is that it's being outgunned by the Fed and its pledge to buy an unlimited amount of U.S. government bonds, which Washington has taken full advantage of by spending trillions of Dollars on support programmes for households and businesses, leaving the ECB in a position where it either has to compete or resign itself to a rising exchange rate for as long as the market remains reluctant to hold the greenback.

"Relative balance sheet developments between Fed and ECB matters for EUR/USD," says Martin Enlund, chief FX strategist at Nordea.

In these circumstances and without a change of course in the U.S. which revives investor interest in greenback, the only way for the ECB to successfully address stifling currency strength might be through a shock and awe stimulus package that includes sooner-than-expected and larger-than-expected increases to the size of the its bond buying facility.

But with European constrained in their recoveries by a combination of excessive debt burdens and onerous EU rules about deficits, it’s not clear that there’ll be enough new European debt for the bank to buy. And in any event, policymakers would have a long way to go before they catch up with the Federal Reserve.

“By our calculations, monthly net asset purchases (PEPP and other programs) averaged about €120 billion (April through September), which was considerably more than central government net issuance of conventional debt excluding bills (around €80 billion per month by our calculations),” BMO's Gallo says. “For the immediate future, we would probably look to get involved in EURUSD on dips below 1.17 or on a close above 1.19. But the balance of risks and moving parts mean that EURUSD fluctuations will be more heavily dependent on what the USD does at this stage, as opposed to what the EUR does.”

Above: Euro-to-Dollar rate shown at weekly intervals alongside Dollar Index (black line, left axis) with selected moving-averages.