-EUR/USD a buy on dips candidate ahead of 2021 assault on 1.20.

-A surprise Trump victory sees EUR fall as far as 1.15 in November.

-But EUR/USD's election losses to be limited whatever the outcome.

Image © European Union - European Parliament, Reproduced Under CC Licensing.

- EUR/USD spot rate at time of writing: 1.1717

- Bank transfer rate (indicative guide): 1.1234-1.1315

- FX specialist providers (indicative guide): 1.1466-1.1536

- More information on FX specialist rates here

Europe’s single currency remains susceptible to short-term losses, especially in the event of a surprise victory by President Donald Trump in November’s election, but Credit Agricole CIB has told clients these declines should be used to implement a “buy on the dip” strategy.

The Euro-to-Dollar rate has lost its lustre steadily in September following a correction in stock markets and a somewhat succesful intervention by the European Central Bank (ECB), which questioned the merits of more-than two-year highs around 1.20 at the turn of the month.

Since then the all-important S&P 500 has fallen more than -3% while the Euro has shed some -1.5% after ECB staff including President Christine Lagarde and Chief Economist Philip Lane sought to further persuade the market to restrain its enthusiasm for the single currency.

“We maintain our constructive view on EUR/USD for 2021 when we expect the pair to revisit 1.2000 and head higher still,” says Valentin Marinov, head of FX strategy at Credit Agricole CIB. “That said, a surprise Donald Trump victory could usher in a period of EUR/USD underperformance in Q420 towards 1.1500, on the back of fears about potential trade tariffs.”

Above: Euro-to-Dollar rate shown at daily intervals alongside S&P 500 index futures (green line, left axis).

The Euro-to-Dollar rate slipped back below the 1.17 handle amid a correction in stock markets last week and although it has since reclaimed that level, gravity has weighed heavily upon the single currency, preventing it from making it past the 1.1750 level on two occasions this week.

Gravity may have been aided by Christine Lagarde, who said in a Monday speech that the bank will be watching the Euro closely and that it could respond in the coming months to any upward moves that further imperil policymakers’ ability to deliver the long-last inflation target of “close to, but below 2%”.

The ECB still has the option of increasing the quantity of government bonds it buys as part of its pandemic-related quantitative easing programme, which would add weight to the burdens carried by the Euro although many doubt that injecting the balance sheet with an extra dose of government debt would do much to restrain the currency not least of all because the market already expects exactly this outcome to materialise before year-end. This is all very relevant to the investment case made by Credit Agricole.

“We do not think that the Eurozone authorities would resort to disruptive full national-level lockdowns in response to the latest rise in infections. We further doubt that any additional ECB easing would be as aggressive as to be a game changer for the EUR, especially if, as we would think, it continues to exclude negative rates,” Marinov says. “The key risk to our constructive view on EUR/USD remains a potential re-election of President Trump.”

Above: Credit Agricole table showing median and mean average G10 currency returns in three months after U.S. elections.

A surprise re-election of President Donald Trump could push the Euro lower in November but Credit Agricole doubts this would disrupt the single currency’s uptrend. It cites a two-decade-long tendency of EUR/USD to emerge as one of the best performers in the aftermath of U.S. elections.

The Republican Party has held the top office three times in that period while the Democratic Party has captured the White House twice.

Europe’s economy might be at risk from renewed tensions if Trump wins but Credit Agricole says to “buy any Trump dip” because a then-lame-duck administration would be more likely to focus on the longer-lived trade dispute with China. That too could be bearish for the Dollar this time.

The safe-haven Dollar was boosted in 2018 and 2019 as the trade war between the world’s two largest economies got going, but that took place under the cover of an economy-boosting programme of tax cuts that disguised its effect on the U.S. but which might not be repeated.

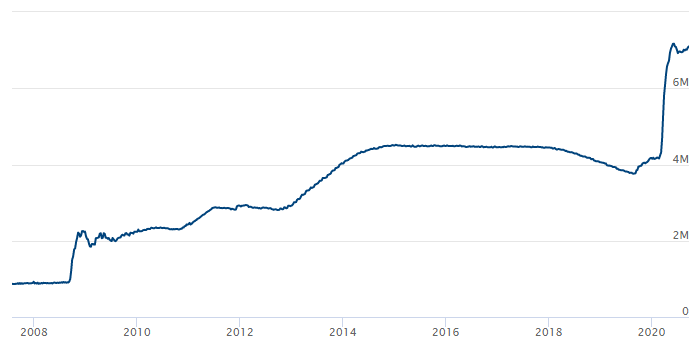

This would leave the ball in the court of the Federal Reserve, which has already undermined the greenback’s appeal by flushing an extraordinary amount of newly created Dollars into financial markets in response to the pandemic, which led to a Dollar shortage and vicious March swings in exchange rates.

The Fed has expanded its balance sheet by more than $2 trillion in the space of two quarters whereas before the pandemic and following the last crisis it took the bank two years to expand its asset holdings by an equivalent amount.

Above: Total value of assets recorded on Federal Reserve system balance sheet. Source: Federal Reserve.

“It remains the case that huge amounts of USD liquidity have stunted the ability of the USD to move back to pre-crisis levels. That said, in our view there are sufficient negative headlines for the market to cover short USD positions going into Q4 and question their EUR longs. We see scope for a dip towards EUR/USD1.16 on a 3 month view,” says Jane Foley, a senior FX strategist at Rabobank, which also forecasts Euro declines in 2021. “Further sharp dips in risk appetite are still likely to at least trigger bouts of USD short covering.”

Foley, like Marinov, also sees scope for a Euro-to-Dollar decline in the final quarter although unlike Credit Agricole the Rabobank team is looking for this to play out no matter who wins the November election and not least of all because an opposition victory could be contested by the incumbent.

Wednesday’s election debate did little to shift the polls, Foley says, leaving the race as a narrow one with the Democratic Party candidte’s lead in key swing states being a precarious one that’s within the margin of error.

This has bolstered concerns in some parts that such a narrow win by the opposition would likely be contested, which means uncertainty that could stoke demand for the safe-haven greenback and weigh on the Euro-to-Dollar rate.

“Given likely delays in counting postal votes and Trump’s predictions of electoral fraud linked to the process, there would appear a tangible risk that both candidates declare themselves as winners of the election. On the heels of recent protests surrounding the BLM movement and elevated unemployment levels, fears of civil unrest have become mainstream,” Foley says. “We see scope for investors to take profits on long EUR positions in Q4 which would pave the way for a moderately softer tone in EUR/USD.”

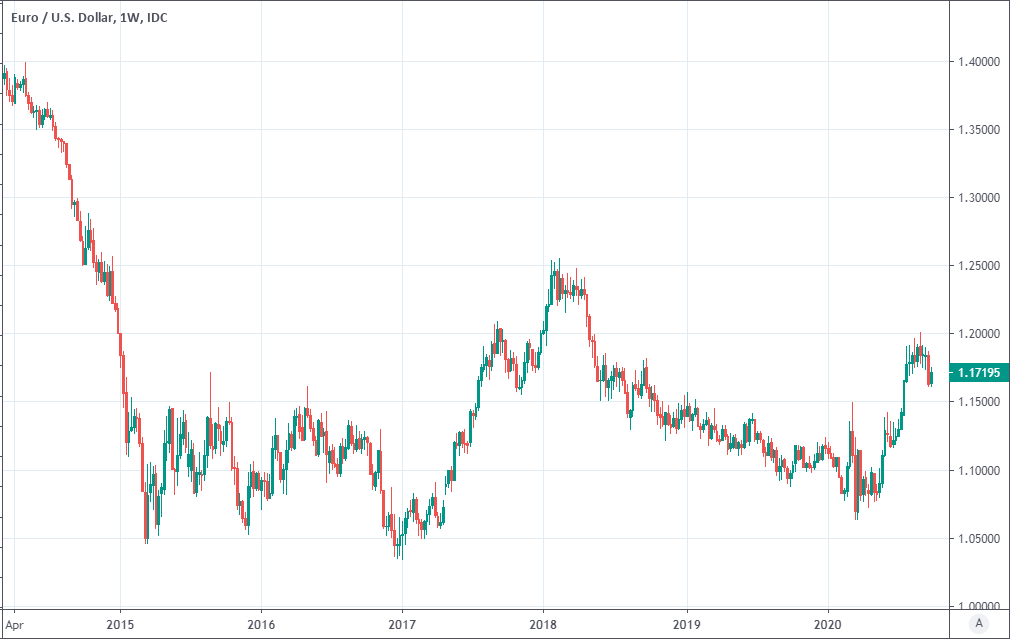

Above: Euro-to-Dollar rate shown at weekly intervals.