© kasto, Adobe Stock

For several years now the Euro has acted like a safe-haven currency: strengthening when investors get fearful and weakening when they get greedy, yet for some reason that relationship has broken down.

On first impressions, the Euro seems to have changed its relationship to risk.

Whereas before it would rise when there is a crisis, in an example of what investors call a 'safe-haven' currency, now that doesn't seem to be the case.

The recent sharp retreat in equities on the back of inflationary fears in the US is a classic example of an event which would normally trigger a flight to 'safety' but it has not led to a rise in the Euro, as would be expected, but actually the opposite, weakness.

Indeed, many dealers were expecting the Euro to rise:

"The latest wave of risk liquidation has inspired a flight to safety bid and it will be particularly interesting to see how much of that safe haven flow is funneled over to the Euro on account of US soft Dollar policy concern," says the dealing desk at broker LMAX.

Yet the answer is, "none so far."

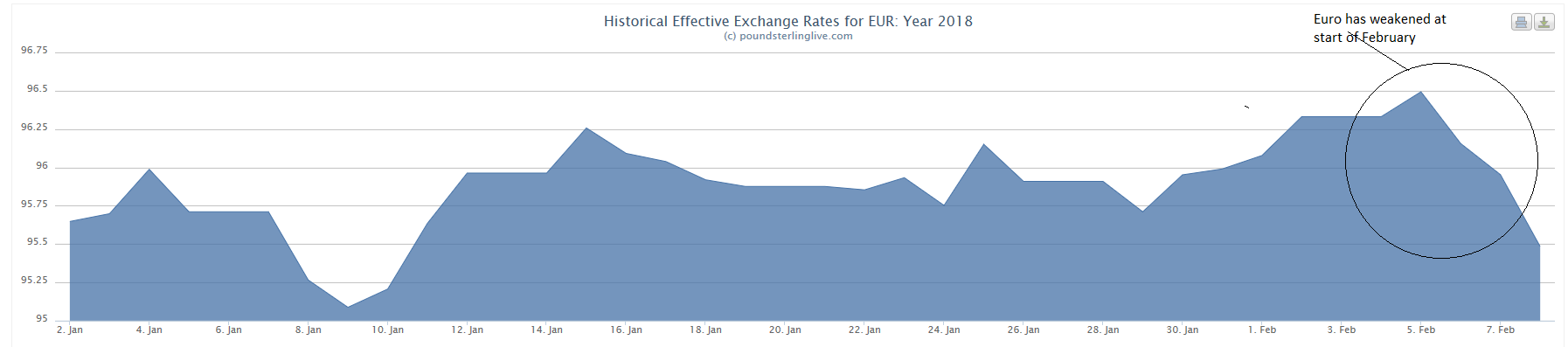

The fall in the Euro since the equity market slump is shown on the Euro index pictured below:

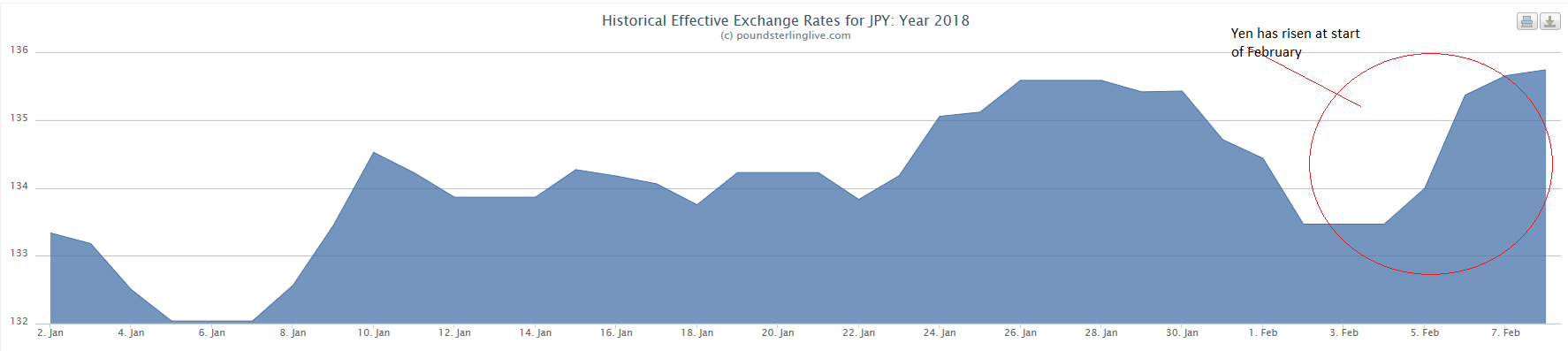

The same cannot be said of the Yen, however, another more traditional safe-haven, which has risen instead as would be expected.

The mystery is why the Euro is not acting like a safe-haven anymore. Is it a change in the Euro or the market which has caused this?

Why Safe?

It may help to explain what a safe-haven currency is first.

'Safe-haven' is a bit of a misnomer, as safe-haven currencies are not 'safer' per se than any other major currencies, rather the reason why they rise during crisis-situations is more complex, and has to do with the cost of borrowing.

Safe-haven currencies like the Yen, the Swiss Franc and previously the Euro all have one thing in common: they all come from countries with low-interest rates.

This makes them cheap to borrow and therefore popular with international investors.

One widely employed investment strategy, for example, is for investors to borrow in a cheap safe-haven currency and use the money to invest in a riskier currency or asset.

The investor then pockets the difference between the returns from the riskier asset or currency and the relatively low repayments of the funding currency.

When markets become volatile and investors start to get worried, however, they often pull out of the risky investments and repatriate the borrowed money to the safe-haven.

This explains why safe-havens increase in value when investors get fearful and risk appetite falls.

Not Overly Scared

Yet interest rates in Europe are still ultra-low so by rights the Euro should still be acting like a safe-haven.

One possible reason why it is not is that the sell-off in equities is not actually really worrying investors, therefore, there is not a real safe-haven bid, and the reason the Yen is rising is because it is being driven by some other factor.

The consensus, after all, has been that global growth is set to catapult higher this year, which seems to indicate an optimistic outlook for the globe at ods with the curren spike in volatility and concerns over risk.

Swiss bank UBS, for example, downplays the importance of the recent sell-off in stocks and bonds.

"The immediate reaction (in the FX market) was rather muted as the equity market volatility was considered a temporary, technical phenomenon with little to no real economic impact," says UBS Strategist Thomas Flurry.

The strategist goes on to restate the UBS house view that global growth is still going to rise in 2018.

"We agree and see also no reason to change our longer-term outlook. A weaker greenback and Swiss franc, a stronger euro, pound and Canadian dollar and a risk that the yen could eventually strengthen remain part of our core views. They are all driven by the main economic theme in 2018, which is for synchronous growth across the globe. We find nothing so far in current macro data or in recent market moves, that would seriously challenge the profound and broad-based upswing in economic sentiment," says Flurry.

Another baffling characteristic of the recent equity and bond market sell-off is the lack of a corresponding rise in gold, which is a safe-haven asset par excellence, so would be expected to rise if investors were really worried.

Another save-haven, the Swiss Franc has also been rather mixed in its response to the recent volatility in stocks, as was actually down against the US Dollar las week.

Perhaps the reason why gold, the Franc, and the Euro have not risen is because the market is not taking the sell-off seriously, as suggested by UBS's Flurry?

Stimulus To End in Japan

If there is no real flight to safety, then how to explain the rise in the Yen which has acted like a typical safe-haven?

One explanation might be that it is due to an idiosyncrasy of the Japanese funding market, another is that the bounce in the Yen was more due to pure speculation, a further that the Yen rose because of other fundamental factors.

The second and third reasons may provide an explanation as to why the Yen has risen more in keeping with its safe-haven status.

Analysts have been saying for quite some time that they expect the Yen to rise in 2018 anyway, but not because it is a safe-haven, but because they expect the central bank to wind down QE and begin raising interest rates - a trajectory which is overall positive for the currency.

The Bank of Japan (BOJ) is already showing signs it may be getting ready to reduce stimulus after it made changes to its last policy meeting statement saying that inflation was now "more or less unchanged" from previously saying prices "have remained on a weakening phase".

The Yen may also have risen due purely to speculation from traders and funds expecting it to go up from safe-haven flows and therefore buying into it en masse; in sufficient volumes, this might have been enough to spur the currency higher.

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.