- GBP/EUR on front foot but upside likely limited

- May struggle to sustain momentum above 1.15

- Win for parliament plotters does little for outlook

- Energy supply & inflation headwinds still persist

- As attention turns to ECB decision & S&P PMIs

Image © Adobe Images

The Pound to Euro exchange rate entered the new week on its front but could struggle to extend Monday's recovery by much beyond the nearby 1.15 level unless this Thursday's European Central Bank (ECB) leads the market to shy further away from the single currency.

Sterling rose broadly from the open on Monday after part of the governing Conservative Party succeeded in deterring former Prime Minister Boris Johnson from participating in the latest selection process for the role of Prime Minister.

That leaves two candidates who both now have partial claims to at two prime ministerial scalps following a multi-month period of infighting that began with the ousting of former Prime Minister Johnson, although each of the remaining candidates is preferable for the markets if stood next to the former PM.

"We see sharp divisions within the Tory party continuing whatever the outcome of next week’s leadership election and remain bearish GBP," says Lee Hardman, a currency analyst at MUFG.

"We are recommending a long EUR/GBP trade idea to reflect both the deteriorating macro outlook for the UK economy and heightened political instability," Hardman said on Friday when advocating that clients look for Sterling to fall back to 1.1111 in the weeks ahead.

Above: Pound to Euro rate shown at 4-hour intervals with Fibonacci retracements of August fall indicating possible areas of technical resistance for Sterling. Click image for closer inspection.

Above: Pound to Euro rate shown at 4-hour intervals with Fibonacci retracements of August fall indicating possible areas of technical resistance for Sterling. Click image for closer inspection.

The identity of the new Prime Minister will be known as soon as Monday afternoon and no later than Friday but with little difference expected between government policies and priorities under either candidate, the further implications for Sterling are potentially limited.

This is partly because changing Prime Minister and government will do little on its own to lessen the headwinds currently darkening the economic outlook such as inflation and the energy supply deficit, both of which have been weaponised by the Kremlin in response to sanctions over its invasion of Ukraine.

"People cannot be fed with printed dollars and euros. You can't feed them with those pieces of paper, and the virtual, inflated capitalisation of western social media companies can't heat their homes," Russian President Vladimir Putin said with apparent satisfaction in a September 30 speech.

"You can't feed anyone with paper – you need food; and you can't heat anyone’s home with these inflated capitalisations – you need energy. That is why politicians in Europe have to convince their fellow citizens to eat less, take a shower less often and dress warmer at home," he added swiftly after.

The identity of the new Prime Minister will become known just as financial markets digest the latest S&P Global PMI surveys of the manufacturing and services sectors for the UK and Europe, which are normally some of the more pessimistic indicators for the UK economy.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of August fall and selected moving-averages indicating possible areas of technical resistance for Sterling. Click image for closer inspection.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of August fall and selected moving-averages indicating possible areas of technical resistance for Sterling. Click image for closer inspection. "Financial strains on households no doubt continued to weigh on consumer activity this month, as have cost pressures on private sector firms, although the flash survey may show an easing in the latter, given ongoing turns in commodity and shipping prices," writes Andrew Goodwin, chief UK economist at Oxford Economics, in a Friday research briefing.

"The political and economic turmoil following the mini-Budget in late September will probably depress the PMIs, given the damaging effect of that turmoil on the sentiment of survey respondents. We expect October's flash services PMI to come in at 49.5 and the manufacturing index 48.5," he added.

Monday's PMI surveys would fall to levels consistent with both of the UK's two largest sectors operating in recessionary conditions if Goodwin and the Oxford Economics team are on the money with their forecasts, though this would merely confirm the message sent by other recent UK economic figures.

Office for National Statistics (ONS) figures suggested last week that UK retail sales fell steeply in September as inflation returned to the double-digit percentages while data released over the course of the prior week had shown the economy contracting far more steeply than was anticipated in August.

"Much of the mini-budget has been reversed and more tightening measures are set to be announced. Despite potentially much higher inflation in 2023, we believe this is supportive of a more measured approach from the MPC [BoE]," say Abbas Khan and Fabrice Montagne, both economists at Barclays.

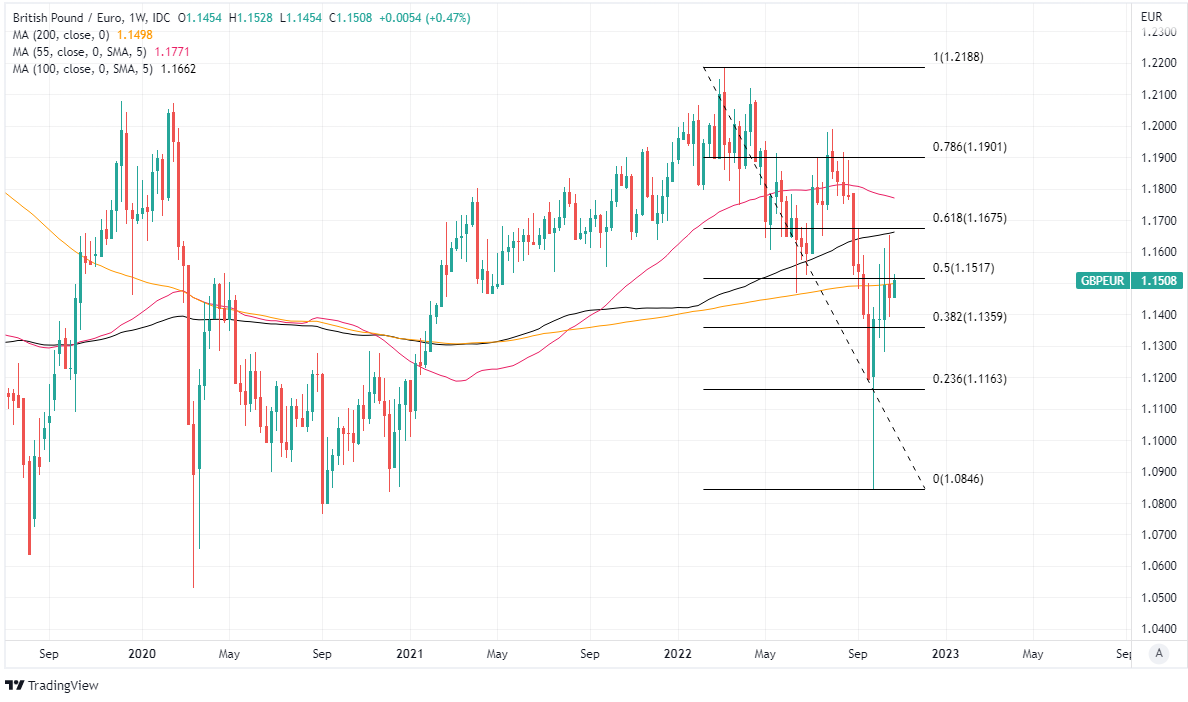

Above: Pound to Euro rate shown at weekly intervals with selected moving-averages and Fibonacci retracements of 2022 downtrend indicating possible areas of technical resistance for Sterling. Click image for closer inspection.

Above: Pound to Euro rate shown at weekly intervals with selected moving-averages and Fibonacci retracements of 2022 downtrend indicating possible areas of technical resistance for Sterling. Click image for closer inspection.

Recent data has cast the economy as slowing faster than expected by the Bank of England and other forecasters while the outlook for it has not been helped by the reversal budget measures announced by the government in late September.

However, for the Pound, much about this week's performance is also likely to depend on the market response to this Thursday's interest rate decision from the European Central Bank, which is widely expected to lift its benchmark interest rate by three quarters of a percentage point for a second time running.

This will further narrow what is already a historically low gap between interest rates in the UK and Eurozone, which might normally be expected to weigh on the Pound, although the ECB's recenrly hawkish turn and various interest rate rises have not done many favours for the single currency so far.

"We expect the ECB to deliver a second consecutive 75bp rate increase in its policy interest rates on Thursday. We also expect its post-meeting commentary to be hawkish because inflation is high and inflation expectations are rising," says Carol Kong, a currency strategist at Commonwealth Bank of Australia.

"Markets have almost fully priced a 75bp hike for both November and December. As a result, we see little potential for a hawkish surprise which would support EUR," Kong and colleagues said in a Monday look at the week ahead.